Can I Buy A House With Inheritance While On Benefits

Dreaming of your own four walls but find yourself relying on the support of benefits? What if a generous inheritance suddenly landed in your lap? It’s a scenario that sparks a lot of curiosity, and frankly, a bit of excitement! The idea of transforming a windfall into a tangible asset like a home while still receiving essential financial assistance is a hot topic for many. It's a question that blends financial planning, understanding the rules, and a healthy dose of optimism. This isn't about dodging rules; it's about navigating them smartly to achieve a significant life goal.

Unlocking Your Homeownership Dreams

So, can you actually buy a house with an inheritance while you're currently receiving government benefits? The short answer is: yes, it's often possible, but it comes with some important considerations and potential changes to your benefit payments. Think of it like this: your inheritance is a new financial resource, and the government has rules about how these resources affect your eligibility for benefits. It's not a blanket "no"; it's more of a "let's look at the details."

The primary purpose of most benefits is to provide a safety net for individuals and families who meet specific income and asset thresholds. When you receive a significant sum of money, like an inheritance, it can alter your financial standing. The good news is that the rules are designed to allow for life changes, including homeownership, without immediately cutting off all support.

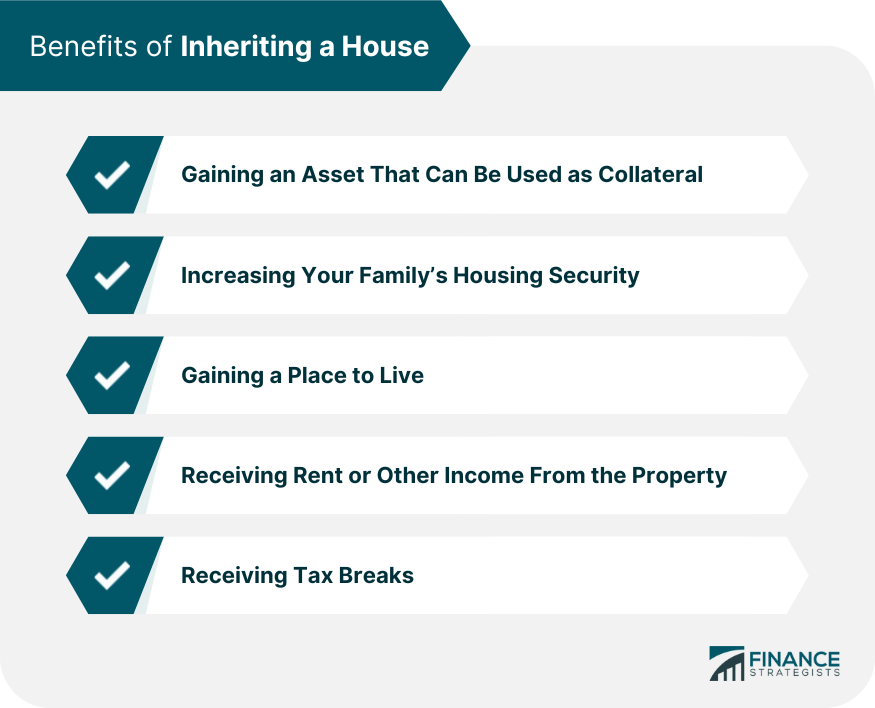

The benefits of being able to buy a house with an inheritance are immense. For starters, you're moving from renting (where your money builds someone else's asset) to owning (where you build your own equity). This provides a stable and secure foundation for your life. Imagine having a place that's truly yours, where you can paint the walls any colour you like, plant a garden, and feel that sense of permanence. It's a massive step towards financial independence and personal freedom.

Furthermore, owning a home can be a significant investment. Over time, the value of your property may increase, providing you with a valuable asset for the future, whether that's for your own retirement or to pass on to your family. It's a tangible way to build wealth and secure your financial future.

Navigating the Nuances: Assets and Income

Here's where things get a little more detailed. Most benefits have limits on the amount of savings and investments you can hold. This is often referred to as the capital limit. When you receive an inheritance, it will likely push you over this limit. For example, benefits like Universal Credit, Jobseeker's Allowance, and some parts of Employment and Support Allowance have capital limits. If your savings (including your inheritance) exceed a certain amount – usually £6,000 for some benefits and £16,000 for others – your entitlement to these benefits may be reduced or stopped altogether.

The key takeaway is that the inheritance itself is treated as capital. However, when you use that capital to buy a primary residence, things can change. The value of your own home is generally not counted as capital for most means-tested benefits. This is a crucial distinction!

So, while the inheritance might initially affect your benefits because it increases your capital, the act of purchasing your main home can then remove that asset from being counted towards your benefit calculations. It's a bit of a juggling act, but the principle is that owning your home is seen differently from simply having a large savings account.

The Role of Your Home

When you use your inheritance to buy a house, that house becomes your primary residence. For most means-tested benefits, the value of your home, and any mortgage you have on it, is not taken into account when calculating your entitlement. This is a fundamental aspect that makes buying a house feasible. Your mortgage payments, however, will become a new outgoing, which is something to factor into your budget.

What about the inheritance money itself before you buy the house? If you receive the inheritance and it pushes your savings above the capital limit, your benefits might be reduced or stopped until you either spend down the money or invest it in a way that doesn't count towards the limit. This is why it's often advisable to act relatively quickly once you receive the inheritance if your goal is to buy a property.

Certain types of benefits are also treated differently. For instance, Disability Living Allowance (DLA) or Personal Independence Payment (PIP) are not means-tested and are not affected by savings or capital. So, if you receive these benefits, an inheritance wouldn't impact them. However, if you receive benefits that are based on your income and savings, like Universal Credit, then the situation is more complex.

Making the Move: Practical Steps

If you find yourself in this exciting position, here’s a simplified approach:

- Seek Professional Advice: This is the most important step! Speak to a financial advisor who specializes in benefits and property, or contact Citizens Advice or a similar organization. They can provide personalised guidance based on your specific circumstances and the benefits you receive.

- Understand the Capital Limits: Familiarise yourself with the capital thresholds for the benefits you claim. This will help you understand how the inheritance might initially impact your payments.

- Budget Wisely: Once you've bought a house, you'll have new expenses like mortgage payments, council tax, insurance, and maintenance. Ensure you have a realistic budget in place.

- Communicate with the DWP: It’s crucial to inform the Department for Work and Pensions (DWP) about any significant changes in your financial circumstances, including receiving an inheritance. They can then advise you on how it will affect your benefits and guide you through the process.

Buying a house is a huge milestone, and receiving an inheritance can be a fantastic catalyst to achieve this dream, even while receiving benefits. By understanding the rules and seeking the right advice, you can successfully navigate this path and unlock a more secure and fulfilling future in your very own home.