Can I Do A Balance Transfer From Someone Else's Card

So, you're staring down a mountain of credit card debt. We've all been there, right? That feeling of "uh oh" when you open the mail, or worse, the app. And then you start thinking, "Is there a magic bullet? A secret escape hatch?" And one of the first things that pops into your head, probably while you're scrolling through finance blogs at 2 AM, is a balance transfer. It’s like a financial Cinderella story, swapping a pumpkin of high interest for a carriage of 0% APR for a little while. Sweet relief!

But then, a different kind of "uh oh" question might hit you. You're talking to your buddy, your sister, your significant other, and they've got a decent credit score, maybe even a shiny new card with a killer intro offer. And you, well, your credit might be… let's just say, "working on it." So the big question, the one that might get you a funny look over your latte, is: "Can I do a balance transfer from someone else's card?"

Let's spill the beans, shall we? The short, sweet, and slightly disappointing answer is: No, you generally cannot do a balance transfer from someone else's credit card directly into your name, or onto your card, using their card to pay your debt. Think of it this way, credit card companies are a little protective of their money. They like to know exactly who they're lending to, and they’re not exactly handing out blank checks for you to manage your pal’s finances. It’s like trying to cash a check that isn't yours – a big no-no.

Why, you ask? Well, it’s all about identity and risk. Credit card companies are essentially making a bet on your ability to repay them. They look at your credit history, your income, all that jazz, to figure out the odds. When you apply for a balance transfer, it’s your application, your credit score, your responsibility. They’re not going to let you borrow money using someone else’s financial credentials. That would be like letting your friend borrow your driver’s license to rent a car – highly illegal and a recipe for disaster, my friends!

So, if you're envisioning a scenario where you snag a sweet 0% APR offer on your card and then somehow, magically, transfer your bestie's high-interest debt onto it, that’s not really how the universe (or the credit card companies) works. It’s a bit of a bummer, I know. You were probably picturing a smooth, seamless financial maneuver, a little white lie to the credit card gods. Alas, they have a very keen sense of who's who.

But wait! Don't throw your perfectly good (or maybe not-so-perfect) credit card in the recycling bin just yet! There are ways people sometimes try to navigate this, and while they’re not direct transfers from someone else’s card, they involve teamwork. Let’s explore these, shall we? Think of it as a collaborative effort to conquer debt. Teamwork makes the dream work, as they say. Though in this case, the dream is paying less interest, which is still pretty sweet!

The "Cash Advance" Shenanigans (and why they’re a TERRIBLE idea)

Okay, so this is where things get a little dicey, and I need to be super clear: DO NOT do this. Seriously. Put down the phone. Step away from the keyboard. This is the financial equivalent of a trap door. Someone might suggest that the person with the good credit score could get a cash advance on their card, and then… well, you can guess what comes next. They’d hand you the cash, and you'd use it to pay off your debt. Sounds simple, right? Wrong!

First off, cash advances are notoriously expensive. Like, eye-wateringly expensive. The interest rates are usually much higher than regular purchases, and they start accruing interest immediately. There's no grace period, no friendly 0% intro offer waiting for you. It’s like paying a penalty just for touching the money. And on top of that, there’s often a cash advance fee, which can be a percentage of the amount you take out. So, let’s say you borrow $5,000. That fee could be $150-$200 right off the bat. Ouch!

And then there’s the whole credit score impact. When your friend takes out a cash advance, it shows up on their credit report. It can ding their credit utilization ratio, which is a big factor in credit scores. So, while you might be thinking you’re helping them out, you could actually be hurting their financial future. That’s not exactly the kind of help you want to offer, is it? Imagine the awkward conversation: "Hey, thanks for the cash, but also, sorry your credit score took a nosedive!" Not ideal.

Plus, let’s not forget the legal and ethical implications. This can be seen as financial fraud. You’re essentially using someone else’s credit line in a way that wasn’t intended and could have serious repercussions for both of you. So, while the idea of a friend lending you cash might seem like a life raft, a cash advance is more like a leaky dinghy in a hurricane. Stick to legitimate financial strategies, folks. Your friendships (and your credit reports) will thank you.

The "Authorized User" Loophole? (Spoiler: It's Not Really a Loophole)

Another idea that might float through your brain is the concept of an authorized user. This is where someone adds you to their credit card account. You get a card with your name on it, linked to their account. It’s often used for family members, or to help someone build credit. So, you might think, "Can I get added as an authorized user to my friend’s card with a good balance transfer offer, and then… you know… do the transfer thing?"

Here's the deal: Being an authorized user means you share the account, not the debt in the same way. When a balance transfer is initiated, it’s a transaction on that specific account. So, if your friend has a card with a 0% intro APR balance transfer offer, they could potentially do a balance transfer to that card to pay off their own existing debt from another card. But you, as an authorized user, cannot initiate a balance transfer from your debt onto their card. The application and the decision-making power for new credit or transfers still lie with the primary account holder.

Think of it this way: The primary cardholder is the captain of the ship. They decide where the ship goes and what it carries. You, as an authorized user, are a passenger with a nice view, but you can’t steer the ship or decide to load it up with someone else's cargo (your debt). The credit card company is looking at the primary cardholder's creditworthiness and their history when approving any changes or new transactions on the account.

Now, this can indirectly help someone build credit. If the primary cardholder manages the account responsibly, paying on time and keeping utilization low, that positive activity can reflect on your credit report too, if the issuer reports authorized user activity. This is a legitimate way to build credit, but it's not a direct path to transferring someone else's debt onto your friend's card. It's more about shared financial responsibility and observation, not a debt-swapping mechanism. So, while authorized user status is a real thing, it doesn't grant you the power to perform a balance transfer from your own financial obligations onto someone else's credit line.

So, What Can You Do? Real Solutions for Real Debt!

Alright, let’s ditch the complicated and potentially risky workarounds. If you can’t directly transfer someone else's balance, what can you do to tackle that debt monster? Don’t despair! There are legitimate and effective strategies out there. We’re talking about taking control of your finances, not trying to pull a fast one.

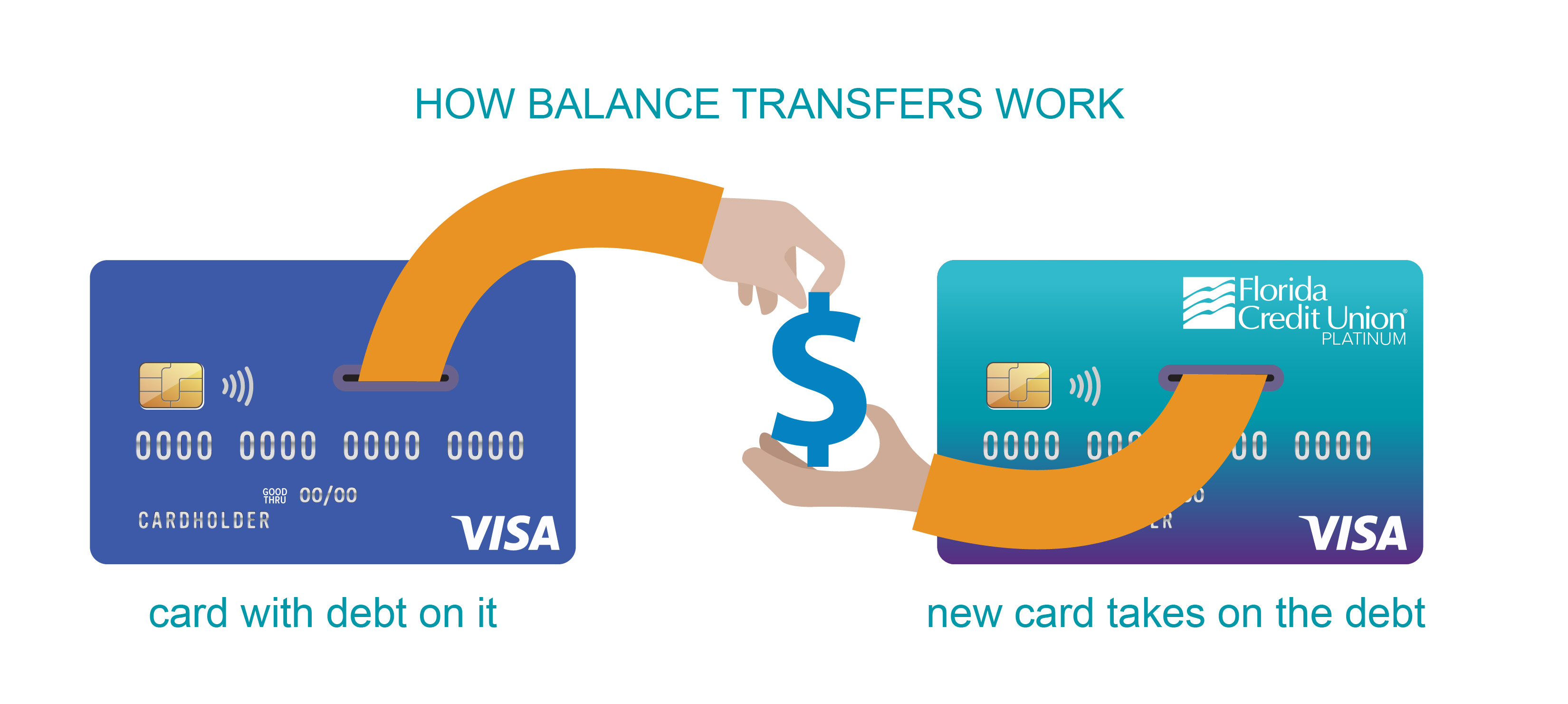

1. Get Your Own Balance Transfer Card: This is the classic, the gold standard. If your credit score is decent, or even if it's just okay, you might qualify for a balance transfer card yourself. You apply for the card, and if approved, you can transfer your own debt from one or more of your high-interest cards onto this new card. The magic here is that introductory 0% APR period! You get a window of time – sometimes 12, 15, or even 18 months – to pay down your debt without accruing interest. This is your chance to attack the principal!

The key is to have a solid plan. Don’t just transfer the debt and forget about it. Make a budget. Figure out how much you can realistically pay each month, and aim to pay off as much as possible before that 0% APR period ends. Remember there’s usually a balance transfer fee, typically around 3-5% of the amount transferred. Factor that in! It’s a small price to pay for potentially saving hundreds or even thousands in interest. This is the most direct and ethical way to leverage a balance transfer.

2. Talk to Your Friend (for a Real Loan, Not a Cash Advance): If your friend with the good credit score is truly willing to help, they can consider offering you a personal loan. This isn’t a cash advance on their credit card; this is them lending you money from their own savings or bank account. You would then use that money to pay off your high-interest credit cards.

This needs to be a very clear, documented agreement. Treat it like a formal loan. Decide on an interest rate (maybe something lower than your credit cards, but fair to them), a repayment schedule, and put it all in writing. This protects both of you and keeps the friendship intact. It’s a much safer and more transparent approach than the cash advance route. Your friend is essentially helping you out by giving you a more manageable repayment plan, without the massive fees and risks of credit card cash advances.

3. Debt Consolidation Loan: Similar to a personal loan from a friend, you can explore getting a debt consolidation loan from a bank or credit union. This is a single loan that you use to pay off all your existing debts (credit cards, etc.). You then make one monthly payment to the lender of the consolidation loan. If you can qualify for a loan with a lower interest rate than what you’re currently paying, this can save you money and simplify your payments.

The effectiveness of this depends heavily on your credit score. A good credit score will get you better rates. If your credit isn't stellar, the rates might not be low enough to make it worthwhile. But it's definitely an option to explore! It’s a structured way to manage your debt with a clear payoff timeline.

4. Negotiate with Your Current Creditors: Don’t underestimate the power of a direct conversation. If you’re struggling to make payments, call your credit card companies. Explain your situation. Sometimes, they are willing to work with you. They might offer a lower interest rate, a payment plan, or even waive some fees. It’s not a guarantee, but it’s always worth a shot. They’d rather work with you than have you default, right? Persistence and politeness can go a long way here.

5. Debt Management Programs: If your debt feels overwhelming, consider a reputable non-profit credit counseling agency. They can help you create a budget, negotiate with creditors on your behalf, and set up a debt management plan. This often involves making one monthly payment to the agency, which then distributes it to your creditors. They can sometimes secure lower interest rates and waived fees for you. It's a structured support system to help you get back on track. They’re the financial therapists of the debt world!

So, while you can't directly transfer someone else's credit card balance to your card, or vice versa in a way that circumvents the rules, there are plenty of legitimate and effective ways to get a handle on your debt. It might require a bit more effort, a bit more planning, and maybe a few more conversations, but it's all about building a stronger, more stable financial future. Remember, honesty and legitimate strategies are always your best bet. Now, go forth and conquer that debt!