Can You Get A Bank Statement From A Closed Account

Ever been there? That moment when you desperately need a bank statement for, let's say, that new apartment application, or perhaps to prove to your slightly skeptical aunt that you did indeed buy her that lovely (and expensive) cashmere sweater? And then you remember… that account is closed. Cue the mild panic. Is it lost to the digital ether forever? Will you have to resort to old-school carrier pigeons to get the information you need? Fear not, dear reader, because in the grand scheme of things, your financial past isn't as locked down as you might think.

Let's dive into the nitty-gritty of whether you can actually snag a bank statement from an account that's officially, irrevocably, closed. Think of this as your friendly neighborhood guide to navigating the sometimes-murky waters of financial record-keeping. No dusty archives or cryptic codes involved, just practical advice with a sprinkle of modern-day savvy.

The "Closed Account" Paradox: What Exactly Does It Mean?

First off, let's get our heads around what "closed" actually signifies. It's not like your bank just hits a delete button and poof, your entire transaction history vanishes into the metaverse. When an account is closed, it typically means it's no longer active for new transactions. The funds might have been transferred, the account balance settled, and the physical plastic card deactivated. But the records? Those usually stick around for a good while.

Think of it like decluttering your digital closet. You might archive old emails, but they're still searchable, right? Your bank operates on a similar principle, albeit with a bit more regulatory muscle behind it. They're legally obligated to keep records for a certain period, so your financial footprint doesn't just disappear overnight.

So, Can You Actually Get It? The Short Answer is… Probably!

Yes, in most cases, you absolutely can get a bank statement from a closed account. The ability to do so, however, often depends on a few factors, primarily:

- How long ago the account was closed: Banks have retention policies. While they're not going to keep your high school checking account statements from 2005 indefinitely, they'll certainly hold onto more recent ones.

- The reason for the closure: Was it a voluntary closure, or did the bank close it due to inactivity or other issues? This might slightly alter the process.

- Your bank's specific policies: Every financial institution has its own set of rules and procedures.

The good news is, most banks are pretty accommodating when it comes to providing historical statements, even from closed accounts. After all, they want to maintain good customer relationships, and being difficult about essential documentation isn't exactly good business practice. It’s like that one friend who always remembers the secret handshake – reliable and reassuring.

Navigating the Channels: How to Request Your Statement

So, how do you go about actually getting the darn thing? It's usually not a Herculean feat, but it does require a little detective work on your part. Here are the most common avenues:

1. Online Banking Portal (The First Line of Defense)

This is your modern-day digital treasure chest. Many banks allow you to access statements for a significant period (often several years) directly through your online banking portal, even for accounts that are no longer active. Log in, navigate to the statements section, and see if your old account pops up. You might need to select a date range. It's like finding a forgotten playlist on Spotify – pure nostalgia, but with actual financial data!

Pro-Tip: If you can't find it immediately, look for a "previously held accounts" or "archived statements" section. Sometimes they’re tucked away, waiting to be discovered.

2. Contacting Customer Service (The Human Touch)

If the digital route yields a blank screen, don't despair. Your next best bet is to pick up the phone or send an email to your bank's customer service. They can guide you through the process of requesting historical statements. Be prepared to verify your identity, as they’ll want to ensure you’re who you say you are – the financial equivalent of showing your ID at a speakeasy.

What to Say: "Hello, I'm trying to access statements for an account that was closed on [approximate date]. I need them for [reason, e.g., personal records, a loan application]." Be polite and clear. Think of it as a friendly chat, not an interrogation. You’d be surprised how much further a "please" and "thank you" can get you.

![How To Obtain Bank Statements On A Closed Account? [Explained]](https://explaincharges.com/wp-content/uploads/2025/07/how-to-obtain-bank-statements-on-a-closed-account.jpg)

3. Visiting a Branch (The Old-School Charm)

In some cases, especially if the account was closed a long time ago or if you're having trouble with other methods, a visit to a physical bank branch might be necessary. A banker can often pull up your records from their system. This might feel a bit retro, like developing film or using a landline, but it can be surprisingly effective.

Fun Fact: Did you know that the first bank in the modern sense was established in Italy in the 14th century? Think of it as the OG fintech!

4. Written Request (The Formal Approach)

For older accounts or specific circumstances, you might need to submit a formal written request by mail. This usually involves downloading a form from the bank's website or writing a letter detailing your request, including your account information and the period for which you need statements. This is the most formal route, akin to sending a well-crafted letter rather than a quick text.

Potential Hurdles and What to Expect

While it's usually straightforward, there can be a few bumps in the road:

- Fees: Some banks might charge a fee for retrieving historical statements, especially if they need to be manually retrieved from archives. This is less common for recent statements but can happen. Think of it as a small "convenience fee" for digging up your past.

- Processing Time: It might not be instant. Depending on the method and how far back you're going, it could take a few days to a couple of weeks to receive your statements. Patience, young grasshopper!

- Statement Format: You might receive them as digital PDFs or physical copies, depending on the bank's capabilities and your preference.

- Limited Information: For very old, closed accounts, the level of detail might be limited. Banks don't keep your high school diary of spending habits forever.

Cultural Context: Why We Need These Statements Anyway

It's interesting to think about why we often need these seemingly mundane documents. In our increasingly digital world, where transactions are often invisible swipes and clicks, bank statements serve as tangible proof. They are the historical record of our financial lives.

From proving residency for immigration purposes to applying for a mortgage, these statements are often the unsung heroes of significant life events. They are the visual narrative of our financial journey, helping us move forward. It's like looking back at old photo albums – it helps you appreciate how far you've come, and it's essential for future planning.

Consider the rise of the "gig economy" and the need to track freelance income. Or the growing popularity of minimalist lifestyles, where people might close old accounts as part of a decluttering spree, only to need a statement later for a specific purpose. The need for these records is a constant, regardless of our lifestyle choices.

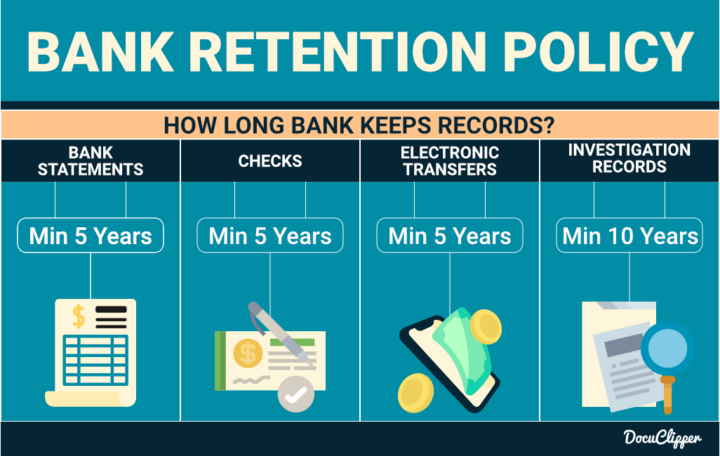

The Timeframe Game: How Long Do Banks Keep Records?

This is the million-dollar question (or rather, the statement retrieval question). Generally, banks are required by regulators to retain customer records for a specific number of years. This timeframe can vary by country and the type of transaction.

In the United States, for example, the Bank Secrecy Act requires financial institutions to keep records of certain transactions for at least five years. However, many banks voluntarily keep records for longer, often 7 to 10 years, or even more for certain types of documentation.

Think of it this way: If you think about it in terms of major life milestones, 5-7 years covers a lot of ground – starting a new job, moving cities, or even the lifespan of a popular Netflix series. Beyond that, it becomes more of a "goodwill" or archival effort by the bank.

When Might You Not Be Able to Get a Statement?

While rare, there are a few scenarios where getting a statement from a closed account might be exceptionally difficult or impossible:

- Extremely Old Accounts: If the account was closed decades ago and the bank has since undergone significant system changes or mergers, it's possible the records are no longer accessible.

- Specific Legal Issues: In cases of fraud or severe legal disputes where records were handled in a particular way, access might be restricted.

- Bank Bankruptcy or Acquisition: If the bank itself ceased to exist without a clear successor retaining all records, this could pose a problem.

These are the extreme edge cases, the financial equivalent of finding a unicorn. For the vast majority of us, the process is much more straightforward.

A Reflection on Our Financial Footprints

In the grand tapestry of our lives, our financial transactions, even from closed accounts, are threads that connect our past to our present and future. The ability to access these statements, even years later, is a quiet testament to the structured nature of our financial systems. It’s a reminder that while we might close a chapter, the evidence of our journey remains.

So, the next time you find yourself needing a statement from an account you thought was long gone, take a deep breath. Channel your inner detective, employ a bit of digital savvy, and don't hesitate to reach out. Your financial history is likely just a few clicks or a polite phone call away. It’s a small comfort, but in a world full of uncertainties, knowing your financial past is accessible can bring a surprising sense of calm. And who doesn't need a little more calm in their day?