Can You Get Mortgage Without Down Payment

Dreaming of your own place? That picture of a cozy living room, a garden to potter in, or even just a quiet space to call your own can feel a million miles away when you hear the words "down payment." It's often seen as the ultimate hurdle, the big, scary number that stands between you and homeownership. But what if we told you that hurdle might not be as high as you think? In fact, it might even be… a hop, skip, and a jump? The idea of snagging a mortgage without a hefty down payment is a topic that sparks a lot of curiosity, a little bit of disbelief, and a whole lot of hope. It’s the ultimate "too good to be true" question that many aspiring homeowners ask, and we’re here to unpack it in a way that’s easy, fun, and genuinely useful.

The whole point of exploring "no down payment mortgages" is to unlock the door to homeownership for folks who might be struggling to save a substantial chunk of cash upfront. Traditional mortgages often require anywhere from 5% to 20% of the home’s price as a down payment. For many, especially first-time buyers or those in high-cost areas, accumulating that kind of money can take years, if not decades. These alternative mortgage options aim to bridge that gap, making the dream of owning a home a more accessible reality. The benefits are pretty straightforward: you get to become a homeowner sooner, start building equity in your property, and avoid paying rent that just goes to someone else's mortgage. Plus, it can be a fantastic way to get into the market before prices climb even higher, potentially locking in a more favorable interest rate in the long run.

So, Can You Really Do It? The "No Down Payment" Magic

The short answer to "Can you get a mortgage without a down payment?" is a resounding yes, but with some important caveats. It's not a free-for-all, and it certainly doesn't mean lenders are handing out money with zero risk involved. Instead, it usually involves government-backed programs or specific lender initiatives designed to help a wider range of people achieve homeownership. Think of it like a helpful nudge rather than a magic wand. These programs often have specific eligibility requirements, and the terms might differ from a standard mortgage. But the core idea remains: you might be able to buy a house without needing to pull out thousands upon thousands of dollars from your savings account.

Unlocking the Doors: Popular Paths to a Zero Down Payment

When people talk about getting a mortgage with no down payment, they're usually referring to a few key avenues. These aren't secret loopholes; they are established programs designed to boost homeownership. Let's break them down:

The USDA Loan: Rural Dreams and Beyond

If you've ever pictured yourself in a charming home in a more rural setting, the United States Department of Agriculture (USDA) Rural Development Guaranteed Housing Loan Program might be your golden ticket. These loans are designed to encourage homeownership in eligible rural and suburban areas. The amazing part? They can offer 100% financing, meaning you can borrow the entire purchase price of the home without a down payment.

Who is it for? Primarily for low-to-moderate income borrowers looking to buy in eligible rural areas. Eligibility is based on income limits, which vary by location. The home itself must also be located in a USDA-designated rural or suburban area.

The Perks: The obvious one is the zero down payment. Beyond that, USDA loans often come with competitive interest rates and can include closing costs in the loan amount if you want to roll them in. They also require mortgage insurance, but it's generally more affordable than private mortgage insurance (PMI) found on conventional loans with smaller down payments.

The Catch: The location is key, and income limits apply. So, while it’s a fantastic option for many, it’s not universally available for every buyer or every property.

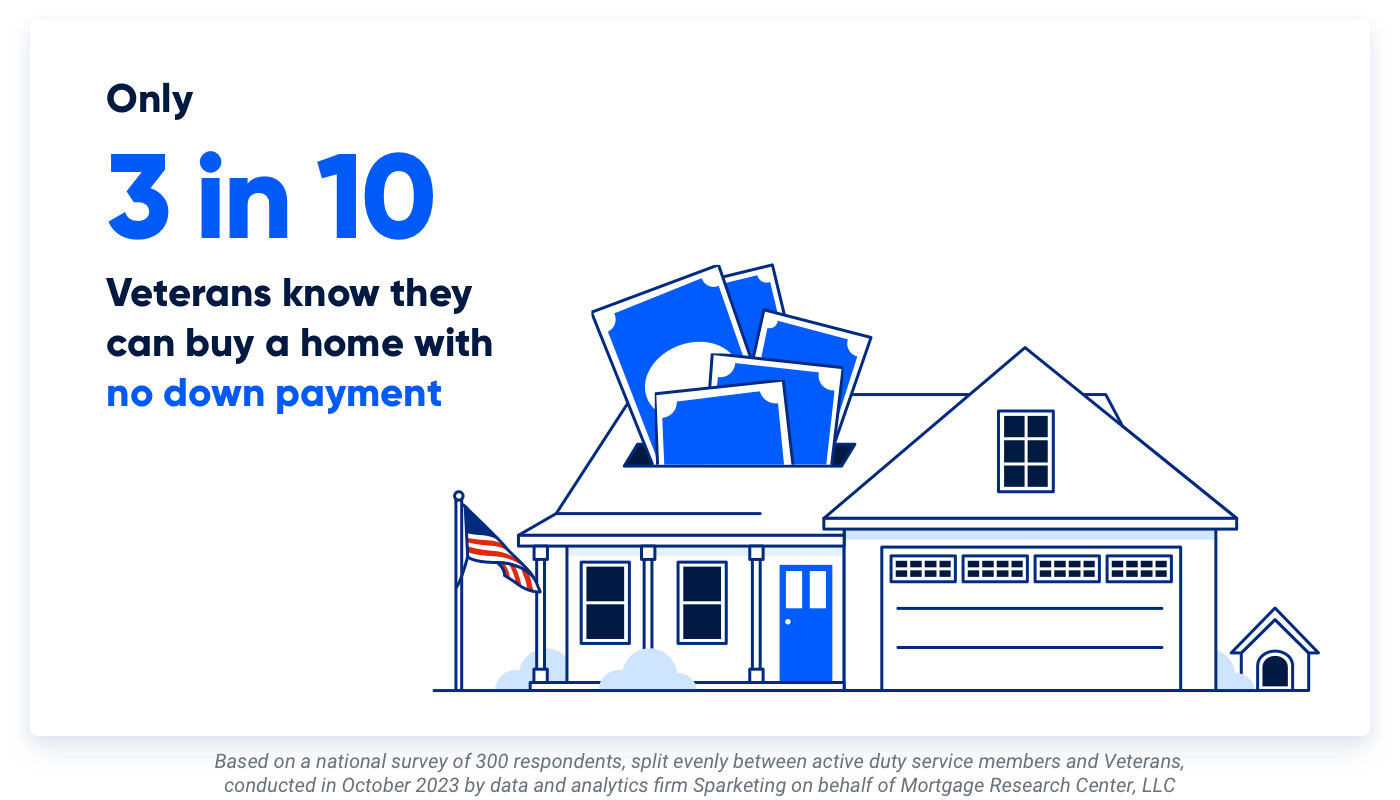

VA Loans: Honoring Our Heroes

For our nation's heroes – the men and women who have served in the United States Armed Forces – the Department of Veterans Affairs (VA) Loan Program is a monumental benefit. These loans are designed to help veterans, active-duty military personnel, and eligible surviving spouses achieve homeownership. The most attractive feature? They offer a zero down payment requirement for most eligible borrowers.

Who is it for? Eligible veterans, active-duty military personnel, and their qualified surviving spouses. You'll need to obtain a Certificate of Eligibility (COE) from the VA to prove your service and eligibility.

The Perks: The no down payment is a massive advantage. VA loans also typically feature competitive interest rates, and they do not require private mortgage insurance (PMI). While there is a VA funding fee, it can often be financed into the loan, and this fee is waived for veterans with service-connected disabilities. Lenders also often have more flexible credit score requirements.

The Catch: The primary hurdle is proving your eligibility through the COE. Once that’s sorted, the benefits are substantial.

FHA Loans: A Helping Hand for First-Timers

The Federal Housing Administration (FHA) loan program is a widely popular option, especially for first-time homebuyers, because it allows for a lower down payment. While not strictly a "no down payment" option, it significantly lowers the barrier to entry. FHA loans can require as little as a 3.5% down payment.

Who is it for? Borrowers who might not have a large down payment saved, those with less-than-perfect credit scores, or first-time homebuyers. FHA loans are insured by the government, making them less risky for lenders, and thus more accessible to borrowers.

The Perks: The low down payment is a huge plus. FHA loans also have more lenient credit score requirements compared to conventional loans, making them attainable for a broader range of individuals. They also often come with competitive interest rates.

The Catch: FHA loans require both an upfront mortgage insurance premium (UFMIP) and annual mortgage insurance premiums (MIP) for the life of the loan in most cases. This can increase your monthly payment and the overall cost of the loan.

State and Local Programs: Tailored to Your Backyard

Beyond the federal programs, many states, counties, and cities offer their own housing assistance programs. These can include down payment assistance (DPA) grants or loans, which can help cover some or all of your required down payment and closing costs. Some programs might even offer low-interest loans or grants to reduce your overall housing expenses.

Who is it for? Varies widely depending on the specific program, but often targets first-time homebuyers, low-to-moderate income individuals, and essential workers.

The Perks: Can significantly reduce or eliminate the upfront cash needed for a down payment. Some grants don't need to be repaid!

The Catch: These programs have their own unique eligibility criteria, application processes, and often a limited funding pool, so it’s essential to research what's available in your area.

Beyond the "No Down Payment": What Else Lenders Consider

Even with these programs, it’s crucial to understand that lenders will still be looking at your overall financial picture. A "no down payment" mortgage doesn't mean "no scrutiny." They'll be evaluating:

- Credit Score: While programs like FHA loans are more forgiving, a decent credit score still signals to lenders that you're a reliable borrower. The better your score, the more likely you are to be approved and get favorable terms.

- Income and Employment Stability: Lenders want to see that you have a steady income to make your monthly mortgage payments. They'll look at your employment history and debt-to-income ratio (DTI).

- Debt-to-Income Ratio (DTI): This is a comparison of your monthly debt payments to your gross monthly income. A lower DTI generally indicates you have more disposable income to handle a mortgage.

- Property Appraisal: The home you want to buy will need to be appraised to ensure its value supports the loan amount.

So, while the dream of a zero down payment mortgage is exciting and achievable for many, remember that it's part of a larger financial puzzle. It’s about making homeownership more accessible, not about avoiding responsibility. If you've been putting off your homeownership dreams because of the daunting down payment, it's time to do a little digging. Explore the options available to you, talk to a trusted mortgage lender or housing counselor, and you might just find that your key to your new home is closer than you think!