Can You Open More Than One Student Bank Account

Hey there, fellow students! Let's chat about something that might seem a bit niche, but trust me, it's got the potential to seriously level up your financial game: student bank accounts. We all know the drill – you’re juggling lectures, late-night study sessions fueled by questionable instant ramen, and trying to maintain some semblance of a social life. Money management can feel like just another item on that never-ending to-do list, right?

But what if I told you there’s a little hack, a secret weapon in your student arsenal, that could make things smoother? We’re talking about the question that’s been buzzing around the digital grapevine: Can you actually open more than one student bank account? The short answer is a resounding YES! And the long answer is… well, we’re about to dive into all the juicy details.

The More, The Merrier? Unpacking the Multi-Account Magic

Think of it like this: you wouldn’t put all your favorite, most treasured possessions in one single box, would you? You’d spread them out, maybe keep your books on a shelf, your art supplies in a craft bin, and your gaming console hooked up to the TV. Your money deserves a similar kind of thoughtful organization. Opening multiple student accounts is all about creating little financial silos, each with its own purpose.

It's like having a personal stylist for your finances! One account for your daily spending (think coffee runs and that essential Netflix subscription), another for saving up for that epic summer trip or that new laptop you’ve been eyeing. And maybe, just maybe, a third for those unexpected emergencies – because let's be real, textbooks aren't cheap, and sometimes your oven decides to take a vacation at the worst possible moment.

Why Bother? The Perks of Proactive Pocket-Padding

So, why would you go through the (minimal!) effort of opening more than one? It boils down to clarity, control, and comfort. When you have everything in one pot, it’s easy for your spending to get blurry. That £5 here, £10 there – it all adds up, and before you know it, your rent money has mysteriously morphed into a mountain of impulse buys.

Having separate accounts forces you to be more intentional. You can see exactly how much you've allocated for groceries, how much is set aside for bills, and how much you can comfortably splurge on that concert ticket. It’s a visual cue, a constant reminder of your financial goals. Plus, many student accounts come with sweet perks – freebies, interest rates that aren’t completely dismal, and often, even overdraft facilities that are more forgiving than your most understanding lecturer.

Imagine this: you're browsing online, see a killer deal on that tech gadget you’ve been coveting. You check your "fun money" account and, surprise! You’ve got enough saved. No guilt, no borrowing from your essentials fund, just pure, unadulterated student joy. That’s the power of segmented savings.

Navigating the Bank-iverse: Your Guide to Opening Doors

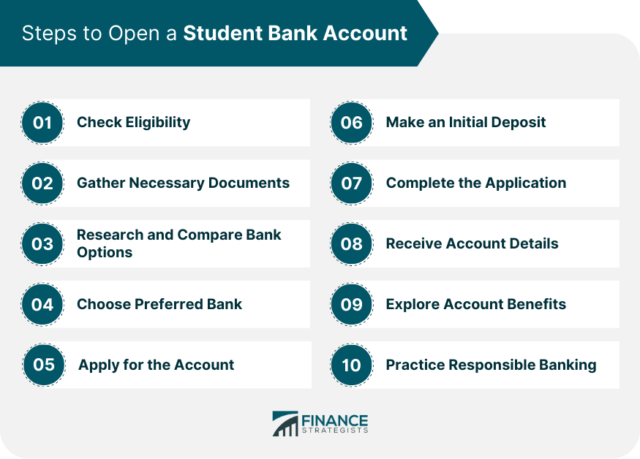

Opening a new bank account might sound like a chore, conjuring up images of endless forms and waiting in line. But honestly, in today’s digital age, it’s often just a few clicks and a quick verification process. Many banks are vying for your student business, so they've made it incredibly easy.

The first step is to do a little research. Not all student accounts are created equal. Some might offer better interest rates, others more generous overdrafts, and some might partner with brands you actually care about (think discounts on student essentials, or perhaps a free coffee from your favorite chain). Think about what matters most to you. Are you a saver? Are you prone to the occasional oops-moment needing that buffer? Or are you all about the perks?

Tip Number 1: Compare, Compare, Compare! Websites like MoneySavingExpert or MoneySuperMarket are your best friends here. They break down all the offers in a super clear way. Don't just go with the first bank your parents used; explore your options!

Once you’ve identified a few contenders, the application process is usually straightforward. You’ll typically need:

- Proof of identity (your passport or driving license).

- Proof of student status (your university acceptance letter or student ID).

- Your National Insurance number.

Many banks allow you to do this entirely online, often within 15-20 minutes. You might even get a welcome bonus for signing up – a little extra cash to kickstart your new financial journey!

The “One Account Per Bank” Rule (and Why It’s Mostly a Myth)

Now, let’s address a common misconception. While it’s generally true that you can only have one type of current account with a single bank, this doesn't stop you from opening different types of accounts (like a savings account) with the same bank, or opening current accounts with different banks. So, you could have your main student current account with Bank A, and then a dedicated savings account with Bank B, and another student current account with Bank C.

It's like having a Netflix subscription and a Disney+ subscription – they both offer streaming, but they're distinct services. You’re not trying to get two Netflix accounts for the price of one; you’re signing up for different offerings.

Fun Fact: In some countries, the concept of a "student account" is more about the perks and lower fees for students, rather than a strictly separate account type. This means you might be able to apply for a standard current account and then inform the bank you’re a student to get those benefits. Always worth asking!

Strategizing Your Student Finances: The Art of Account Allocation

Okay, so you’ve got the green light to open multiple accounts. Now, how do you make it work for you? Let’s brainstorm some super practical strategies:

The “Rent & Bills Buster” Account

This account is your responsible adult. As soon as your student loan or parental contributions land, you immediately transfer your rent, utilities, and other fixed expenses into this account. This way, you know that your essential payments are covered, and you won’t be tempted to dip into them for a spontaneous pizza delivery.

Practical Tip: Set up an automatic transfer from your main account to this one on the day you receive your funds. Out of sight, out of mind!

The “Daily Grind & Grub” Account

This is your everyday spending hub. Keep your weekly budget for food, transport, and those essential coffees in here. It’s the account you’ll use your debit card from most often. By setting a clear limit, you’re essentially giving yourself a weekly allowance. When it’s gone, it’s gone!

Cultural Reference: Think of this like your “walking around money” – the cash you'd historically carry for immediate needs. Except, it's digital and much safer!

The “Future You Will Thank You” Savings Account

This is where the magic happens for your bigger goals. That deposit for your first apartment after uni? That amazing backpacking adventure through Europe? A new laptop that won’t make you want to throw it out the window? Dedicate a savings account for these. Even small, regular transfers can add up significantly over time.

Fun Fact: The concept of saving, while ancient, really took off with the rise of formal banking. Early banks were often seen as safe havens for wealth, and the idea of earning interest on your savings was a revolutionary concept!

The “Emergency Fund – You Got This!” Account

Life happens, right? Your phone might die an untimely death, or you might need an unexpected trip home. Having a small, accessible emergency fund means you can deal with these hiccups without derailing your other financial goals. Aim for a small buffer that you can replenish as quickly as possible.

Think of it like a financial safety net, inspired by the superhero trope of having a hidden escape route or a secret stash of supplies.**

Beyond the Basics: Advanced Student Account Hacks

Once you’ve mastered the multi-account setup, you can get even more sophisticated:

Leveraging Different Account Features

Some banks offer high-interest savings accounts, while others have better mobile banking apps. By using accounts from different banks, you can cherry-pick the best features. One bank might give you a decent interest rate on your savings, while another offers a 0% interest overdraft for your entire degree (a lifesaver!).

Setting Up Standing Orders and Direct Debits Strategically

This is where automation truly shines. Set up standing orders to move money between your accounts on specific dates. Direct debits for bills should come out of your "Rent & Bills Buster" account. This system keeps everything ticking over smoothly without you having to remember every single detail.

The Psychology of Separation

There’s a psychological element to this, too. Seeing a dedicated savings account with a growing balance feels incredibly rewarding. It’s tangible proof of your progress. Likewise, seeing your "Daily Grind" account dwindling reminds you to be mindful of your spending. It’s a visual and emotional reinforcement of good financial habits.

Cultural Reference: This is similar to how Marie Kondo encourages people to declutter and organize their homes. By giving everything a specific place, you create order and clarity. Your money deserves the same treatment!

A Word of Caution: Don't Overcomplicate It!

While opening multiple accounts can be incredibly beneficial, it’s important not to go overboard. Having 10 different accounts with 10 different banks will likely lead to more confusion than clarity. The goal is to simplify your financial life, not to create a tangled web of logins and passwords.

Find the sweet spot for you. For most students, two to three accounts will likely be more than enough to implement a successful financial strategy. Stick to well-known, reputable banks with good student offerings.

Also, always be aware of minimum balance requirements or any potential fees. While student accounts are generally designed to be fee-free for students, it's good practice to read the terms and conditions. Nobody wants unexpected charges!

The Final Word: Your Money, Your Master Plan

So, can you open more than one student bank account? Absolutely! And if you’re looking for a way to gain more control, reduce financial stress, and actually start making progress towards your goals, it’s a strategy worth seriously considering.

It’s about taking a small step to organize your finances, giving yourself the tools to succeed. Think of it as investing in your future self, one smartly managed account at a time. It’s not about being a financial wizard, but about being a little bit more intentional with the money you have. After all, as students, we’re all just trying to navigate this wild ride called life, and having our finances in order can make that journey a whole lot smoother and a lot more fun.

In the grand scheme of things, managing your money is just another skill you're honing, like perfecting that essay structure or mastering that complex equation. It’s about building good habits that will serve you long after you’ve tossed that graduation cap in the air. So go forth, explore your options, and start building your own personal financial success story, one account at a time!