Charles Schwab 401k Transfer

Ah, the 401(k) transfer. For some, it might sound like dry financial jargon, a topic to be discussed only when the taxman looms. But for many of us, especially those navigating the exciting, and sometimes dizzying, world of career changes and financial planning, it's a surprisingly satisfying and empowering act. Think of it as giving your hard-earned retirement nest egg a much-needed spa day, or perhaps a strategic relocation to a more opulent penthouse suite. It’s about taking control, ensuring your future self is living the good life, not just scraping by.

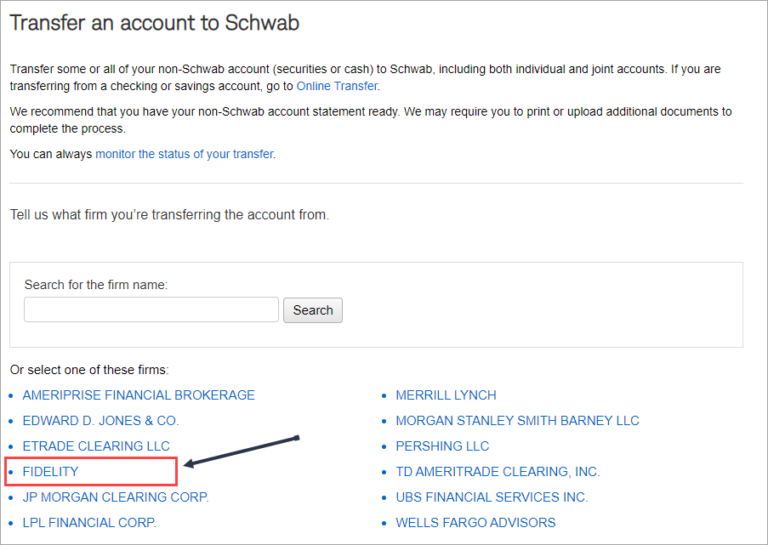

So, what’s the big deal? The Charles Schwab 401(k) transfer, or more broadly, any 401(k) rollover, is essentially moving funds from an old employer’s retirement plan to a new one, or to an Individual Retirement Account (IRA). The primary purpose? Simplicity and potential growth. When you leave a job, that old 401(k) can become a bit of a forgotten relic. It might have higher fees, limited investment options, or simply be a hassle to keep track of alongside your current plan. Consolidating your retirement savings into one accessible account, like a Schwab IRA or a new employer's 401(k), makes managing your investments much easier. No more logging into multiple portals, no more lost statements!

The benefits extend beyond mere convenience. Often, a rollover can lead to lower fees. Different plans have different expense ratios, and by moving your money, you might find a plan with more competitive pricing, letting more of your hard-earned dollars work for you. Furthermore, you gain greater investment flexibility. While your old 401(k) might have had a curated menu of funds, a Schwab IRA, for instance, often opens up a vast universe of investment choices – from stocks and bonds to ETFs and mutual funds. This allows you to tailor your portfolio to your specific risk tolerance and financial goals, especially as you get closer to retirement.

Think about common scenarios. You’ve just landed your dream job, and your previous employer’s 401(k) is sitting there, gathering dust. Or perhaps you’ve been a freelancer for a while and have accumulated several old 401(k)s from past W-2 positions. The most common way to handle this is through a direct rollover. This is where the funds are transferred directly from your old plan administrator to your new account, avoiding any potential tax implications or penalties. Another option is an indirect rollover, where you receive a check, but you have a strict 60-day window to deposit it into a new account. While both are valid, the direct rollover is generally the smoother and safer option.

To make your Charles Schwab 401(k) transfer experience even more enjoyable, here are a few practical tips. First, do your homework. Research Schwab’s IRA offerings and compare them to your new employer’s 401(k). Understand the fees, investment choices, and any advisory services they provide. Second, understand the process. Don't be afraid to call Schwab or your old plan administrator. They are there to guide you. Most importantly, plan your investment strategy for the new account. Don't just dump the money in without a thought. Consider your retirement timeline and risk tolerance. This isn't just a transfer; it's an opportunity to proactively build your future wealth. Enjoy the peace of mind that comes with having your financial future neatly organized and strategically positioned!