Closing Cost On 100k House

So, you're thinking about diving into the world of homeownership, huh? Maybe you've spotted a charming little place for around $100,000, and you're picturing yourself sipping coffee on its porch. Sounds dreamy, right? But before you start picking out paint colors, let's chat about something that might seem a little less glamorous, but is super important: closing costs.

Think of closing costs as the "welcome to the club" fees for owning a home. It’s like when you join a new gym – you might have an initiation fee along with your monthly membership. For a $100k house, these costs aren't going to be astronomical, but they're definitely something to be aware of so you don't get any nasty surprises.

So, What Exactly ARE These "Closing Costs" Anyway?

Basically, closing costs are a collection of fees you'll pay at the very end of your home purchase. They cover all sorts of things that make the sale official and legal. It's not just about the sticker price of the house itself; it's about all the behind-the-scenes work and services that go into transferring ownership from one person to another.

Imagine buying a really cool, vintage car. You're not just paying the price tag for the car, right? You also have to factor in the cost of getting it registered, maybe a new insurance policy, and perhaps a tune-up to make sure it's running smoothly. Closing costs are a bit like that, but for your new humble abode.

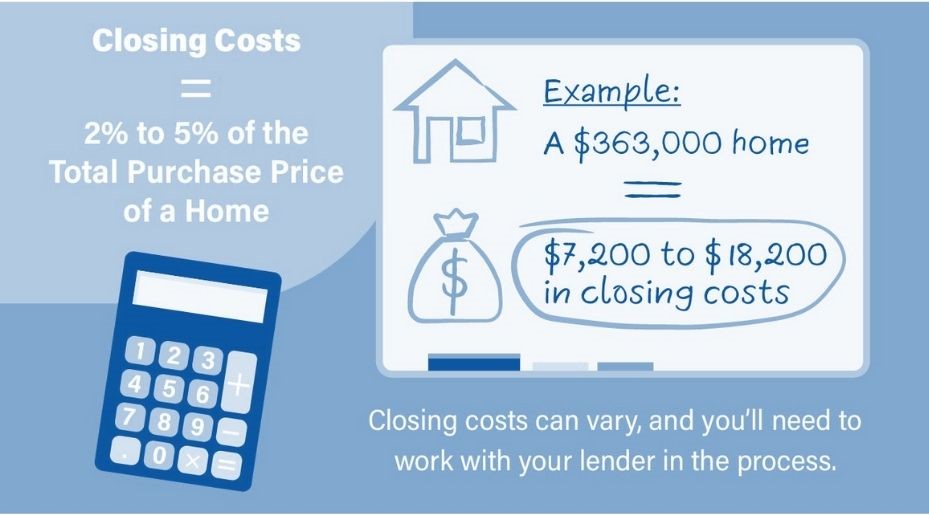

For a $100k house, these costs can range from about 2% to 5% of the loan amount, or sometimes the purchase price. So, for a $100k house, you could be looking at anywhere from $2,000 to $5,000 in closing costs. It’s not pocket change, but it’s also not the down payment itself, so that’s a relief!

Why So Many Different Fees? It's Like a Potluck of Paperwork!

Okay, so why all the fuss? Well, a lot of different folks and services are involved in making a home sale happen. It's like throwing a party – you've got the caterers (lender fees), the decorators (appraisal fees), and the guests (title company, inspectors). Everyone plays a role!

The Big Players and Their Fees

Let's break down some of the common characters you'll meet in the closing cost cast:

1. The Lender's Take: "We Helped You Get This Money!"

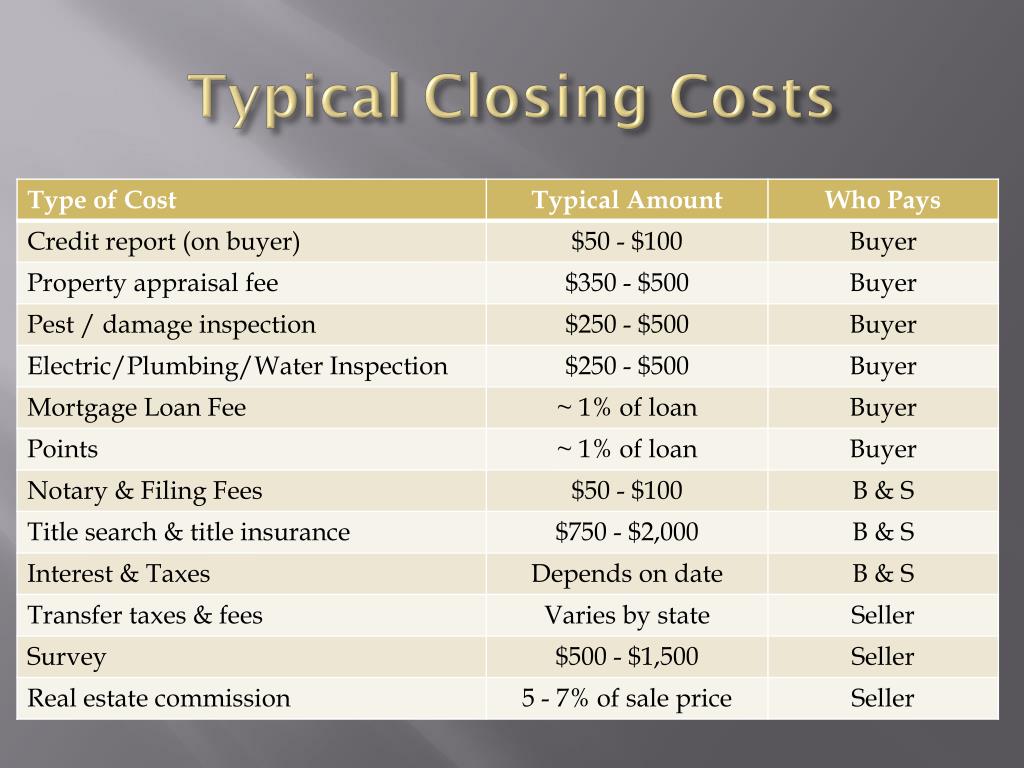

If you're getting a mortgage (and most people do!), the bank or lender will charge you for their services. This can include things like:

- Loan Origination Fee: This is pretty much the lender's fee for processing your loan. Think of it as their "thanks for choosing us" charge. It's often a percentage of the loan amount.

- Underwriting Fee: This is for the people who carefully review your financial situation to decide if you're a good bet for the loan. They're the financial detectives!

- Discount Points (Optional): Sometimes, you can pay extra upfront to "buy down" your interest rate for the life of the loan. It's like buying a membership that gives you a lower monthly subscription fee forever. For a $100k house, this is less common unless you're really planning to stay put for a long time.

2. The Appraiser: "Is This House Really Worth $100k?"

Your lender will want to make sure the house is actually worth what you're paying for it. So, they'll hire an appraiser to come in and give it a thorough once-over. This fee covers their time and expertise. It's like getting a professional opinion on a valuable item.

3. The Inspector: "Is There a Secret Squirrel Nest in the Attic?"

This is a super important step! A home inspector will check out the nitty-gritty details of the house – the roof, the plumbing, the electrical, the foundation. You want to know if there are any hidden problems that could cost you a fortune down the road. This fee is for their keen eyes and knowledge.

4. The Title Company: "Making Sure the Deed is Clean!"

The title company is like the guardian of the house's history. They do a deep dive into public records to make sure the seller actually owns the house and that there are no liens or claims against it. They're ensuring you get a clear title, which is crucial!

- Title Search Fee: For their detective work.

- Title Insurance: This is a one-time fee that protects you (and your lender) in case any past ownership issues pop up later. It's like an insurance policy for the ownership of your home.

5. Government Fees: The Official Stamp of Approval

There are usually some government-related fees to make the transfer official.

- Recording Fees: When you officially become the owner, your county or city needs to record that change in their public records. This fee is for that administrative task.

- Transfer Taxes (if applicable): Some areas have a tax on the transfer of property ownership. This can vary quite a bit by location.

6. Other Little Things: The "Maybes" and "Just in Cases"

You might also encounter:

- Attorney Fees (if required): In some states, you'll need an attorney to review and finalize the paperwork.

- Escrow Fees: This is for the service of holding your funds and documents until closing.

- Prepaid Interest: You might have to pay a bit of interest on your loan from the closing date to the end of that month.

- Homeowner's Insurance Premium: You'll usually have to pay for your first year of homeowner's insurance upfront.

- Property Taxes: You might have to deposit a few months' worth of property taxes into an escrow account.

Can You Negotiate Closing Costs?

This is where things get interesting! While some fees are pretty standard, others might have a little wiggle room. For a $100k house, you might have a bit more leverage than someone buying a multi-million dollar mansion. Don't be afraid to ask your lender and real estate agent about specific fees and if they're negotiable.

Sometimes, you can ask the seller to contribute to your closing costs as part of the negotiation. This is especially true if the house has been on the market for a while or if there are minor issues found during the inspection. It's like saying, "Hey, I'm really keen on this place, but these extra costs are a bit much. Could you help me out a little?"

Another cool trick? You can shop around for lenders! Different lenders can have different fee structures. Getting quotes from a few can save you a pretty penny.

The Final Word: Be Prepared, Not Panicked!

Look, closing costs can seem like a lot at first glance. But for a $100k house, they're a manageable part of the home-buying puzzle. The key is to be informed and prepared. When you get your Loan Estimate from your lender, take the time to read it carefully. Ask questions! Your real estate agent and loan officer are there to help you navigate this.

Think of it this way: these costs are an investment in your future. They're the final steps that get you from dreaming about that $100k house to actually holding the keys to your very own place. So, while they might not be the most thrilling part of buying a home, they're definitely a necessary and interesting part of the journey. Happy house hunting!