Could Women Open Bank Accounts Before 1974

Hey there! So, imagine this: you’re a woman, you’ve got your own paycheck, maybe you’ve inherited some dough, and you’re thinking, "Awesome! Time to open my own bank account!" Seems like a no-brainer, right? Like, of course you can. But here’s a fun little history lesson that might just blow your mind a tiny bit. Ever wondered if women always had the key to their own financial kingdoms? Let's spill the tea on whether ladies could, you know, actually open their own bank accounts before the groovy year of 1974.

Now, before we dive in, let’s set the scene. We’re talking about a time that wasn’t that long ago, relatively speaking. We’re not going back to the days of corsets and powdered wigs (though that’s a whole other fascinating can of worms!). We’re talking about the mid-20th century, a period often painted as a time of progress, but with some sneaky, outdated laws still hanging around like that one sock that mysteriously disappears in the dryer. You know the one.

So, The Big Question: Could They or Couldn’t They?

Alright, drumroll please… Yes, women could open bank accounts before 1974. Phew! Okay, breathe easy, your great-aunt Mildred probably wasn't turned away at the bank door with a polite but firm "Sorry, dearie, no ladies allowed unless you've got a man's signature." That would be a bit too dramatic, even for a historical drama!

But here's where it gets… well, interesting. While the door wasn't slammed shut in their faces, the way women accessed their money and the control they had over it was a whole different story. It wasn't as simple as just walking in and saying, "My name is [Your Name], and I'd like to deposit this glorious pile of cash!" Oh no, that would be too straightforward, wouldn't it?

The Nitty-Gritty: What Was Really Going On?

Think about it from a legal perspective. For a really long time, women were considered legally dependent on men. This wasn't just about societal expectations; it was baked into the law. If a woman was married, her husband was often legally in charge of her finances. This concept, known as coverture (fancy word, right?), essentially meant that a married woman's legal identity was subsumed by her husband's. So, if she had her own money, it was often technically his money too. It’s enough to make you want to do a rebellious jig!

This meant that even if a woman wanted to open her own account, she might need her husband's permission or even his signature. Imagine that! Want to save up for that new hat you’ve been eyeing? Gotta get the hubby’s OK. Planning a surprise birthday gift for him? Better not let him see that savings account!

And it wasn't just married women. Unmarried women, especially those who had inherited money or were earning their own keep, could also face hurdles. Banks, being the cautious institutions they are, often had policies that reflected the prevailing societal attitudes. If a woman didn't have a male relative (father, brother, husband) to vouch for her or co-sign, it could be a bit of a struggle to prove her financial independence and trustworthiness.

The "Feme Covert" Clause: A Real Buzzkill

Let’s delve a little deeper into this "coverture" business. Under this legal doctrine, a married woman was often referred to as a "feme covert" (again with the fancy legal terms!). This meant she was "covered" by her husband. Consequently, she generally couldn't own property in her own name, enter into contracts independently, or even sue or be sued without her husband's involvement. And guess what that included? Managing her own money! It’s like having a financial shadow constantly looking over your shoulder.

So, while a bank might have let her open an account, it was often under terms that acknowledged her husband's legal authority. It wasn't exactly a declaration of financial freedom, was it? It was more like a temporary loan of her own money, under the watchful eye of the patriarchy. Not exactly the empowering feeling you’d hope for.

The "Equal Credit Opportunity Act" - Our Hero!

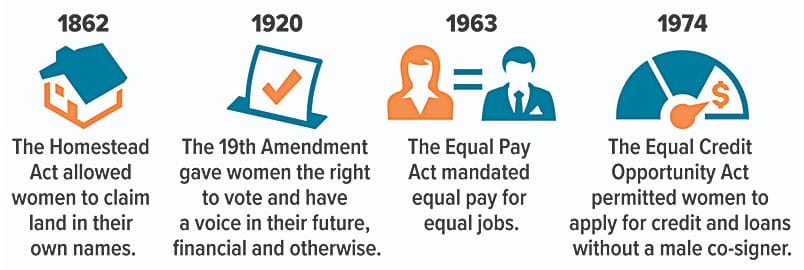

Okay, so we’ve established that it wasn't always a walk in the park. But then came a game-changer. Enter the Equal Credit Opportunity Act of 1974. This was a HUGE deal! Before this act, lenders (banks included) could legally discriminate against applicants based on things like sex, marital status, race, national origin, and age. Yes, you read that right. They could just say, "Nope, no married women today!" or "Sorry, we don't lend to single ladies."

The Equal Credit Opportunity Act (ECOA) basically said, "Hold up! That's not cool." It made it illegal for creditors to discriminate against applicants in any aspect of a credit transaction. This meant that women, regardless of their marital status or gender, had a right to apply for and receive credit, including opening their own bank accounts, on the same terms as men. This was revolutionary!

This act didn't create the ability for women to open bank accounts from scratch. That ability, in a limited and often restricted form, existed before. But the ECOA empowered women to do so without discrimination and with full autonomy. It removed the legal barriers that were often used to limit their financial independence. It was like upgrading from a rickety old bicycle to a sleek, fast sports car. Suddenly, the road was wide open!

Before 1974: A Patchwork of Possibilities

So, to recap the pre-1974 era: it was a bit of a mixed bag. Some women, particularly those who were single, widowed, or had particularly progressive husbands, might have found it relatively easy to open accounts. Others, especially married women whose husbands were less supportive or who lived in more traditional communities, faced significant hurdles. It wasn't a universal "no," but it was certainly not a universal "yes" with all the bells and whistles of equal footing.

Banks often had their own internal policies, which could be influenced by state laws, local customs, and the individual bankers themselves. Some were more forward-thinking than others. It was a bit like playing financial roulette. You might land on a good bank, or you might land on one that made you feel like you were asking for a loan from the mafia!

Consider this: a woman might have been able to open a savings account, but perhaps not a checking account that allowed her to write checks freely. Or she might have been able to open an account, but needed her husband to co-sign for any significant withdrawals. It was all about degrees of control and autonomy. Imagine having to explain every single time you wanted to buy a cup of coffee! Utter madness.

The Real Shift: Autonomy and Dignity

The true power of the ECOA wasn't just about the mechanics of opening an account; it was about the fundamental shift in recognizing women's economic rights and their inherent dignity. It was a legal acknowledgment that a woman’s financial life was her own, not an extension or appendage of a man's. This was crucial for women who were entering the workforce in increasing numbers and earning their own money.

It meant that if a woman was the victim of domestic abuse, she wouldn't be financially tied to her abuser through joint bank accounts. It meant that if a woman wanted to start her own business, she could apply for loans and accounts in her own name. It meant that she could build her own financial future, independently and with pride.

This wasn't just about dollars and cents; it was about a woman’s ability to make her own choices, to be self-sufficient, and to have the same opportunities as her male counterparts. It was about finally being able to say, "This money is mine, I earned it, and I decide what happens with it." Talk about a mic drop moment for women everywhere!

It Wasn’t Just Banks, Though

It’s important to remember that this struggle for financial equality wasn’t confined to just banks. It extended to credit cards, mortgages, car loans, and pretty much any financial transaction where you needed to prove your creditworthiness. Before 1974, all of these were often inaccessible or heavily restricted for women. A woman could have a stellar credit history from her own job, but if she was married, her husband’s financial standing (or lack thereof) could be the deciding factor. It was a frustrating system that held many capable women back.

The fight for financial equality was a multi-faceted battle, and the ECOA was a major victory on one of its most important fronts. It opened up the doors not just to bank accounts, but to a world of financial possibilities that had previously been limited or non-existent for many women.

So, What’s the Takeaway?

The answer to "Could women open bank accounts before 1974?" is a nuanced "Yes, but it was complicated and often discriminatory." The Equal Credit Opportunity Act of 1974 was the real hero of the story, legalizing equal access and empowering women to manage their finances with the autonomy and respect they deserved. It was a massive step forward in a long journey towards true financial independence for women.

It’s easy to take for granted the ability to walk into a bank, open an account, and manage your money freely. But a little bit of history reminds us that this freedom wasn't always a given. It was fought for, legislated for, and ultimately, it’s a testament to the incredible resilience and determination of women who paved the way for us.

So, the next time you’re using your debit card or checking your online banking, take a moment to appreciate the journey. You’re not just managing your money; you’re participating in a legacy of progress and empowerment. And that, my friends, is something to truly smile about. Go forth and conquer your financial goals, ladies!