Difference Between A Standing Order And Direct Debit

Hey there, digital nomads, cozy homebodies, and everyone in between! Let's talk about something that might sound a little… well, financial. But don't let that send you running for the hills! We're diving into the wonderfully practical, surprisingly simple world of how your money moves around for those recurring bills. Think of it as a mini-masterclass in keeping your cool when it comes to your finances, served with a side of chill vibes.

Ever find yourself staring at your bank statement, wondering how that subscription you vaguely remember signing up for keeps happily draining your account? Or perhaps you're meticulous, setting up payments like a pro, but the terms get a little fuzzy? Today, we're demystifying two of the most common ways your money gets from your account to, say, your streaming service, your gym, or even your friendly neighborhood utility company: Standing Orders and Direct Debits.

Now, I know what you're thinking. "Really? Money stuff? Can't we just talk about the latest Netflix binge or the perfect brunch spot?" Trust me, understanding these little financial wizards can actually free up your brain space for all those important things. Imagine a world where you don't have to stress about missing a payment, incurring a late fee, or that slightly panicked feeling when you think you forgot something. That, my friends, is the promise of these automated payment methods.

The Stand-Up Guy: Understanding Standing Orders

Let's start with the Standing Order. Think of it as your reliable, old-school friend. You tell it exactly what to do, and it does it, no questions asked, no deviations. It's like programming your VCR back in the day – you set the channel, the time, and it’s locked in.

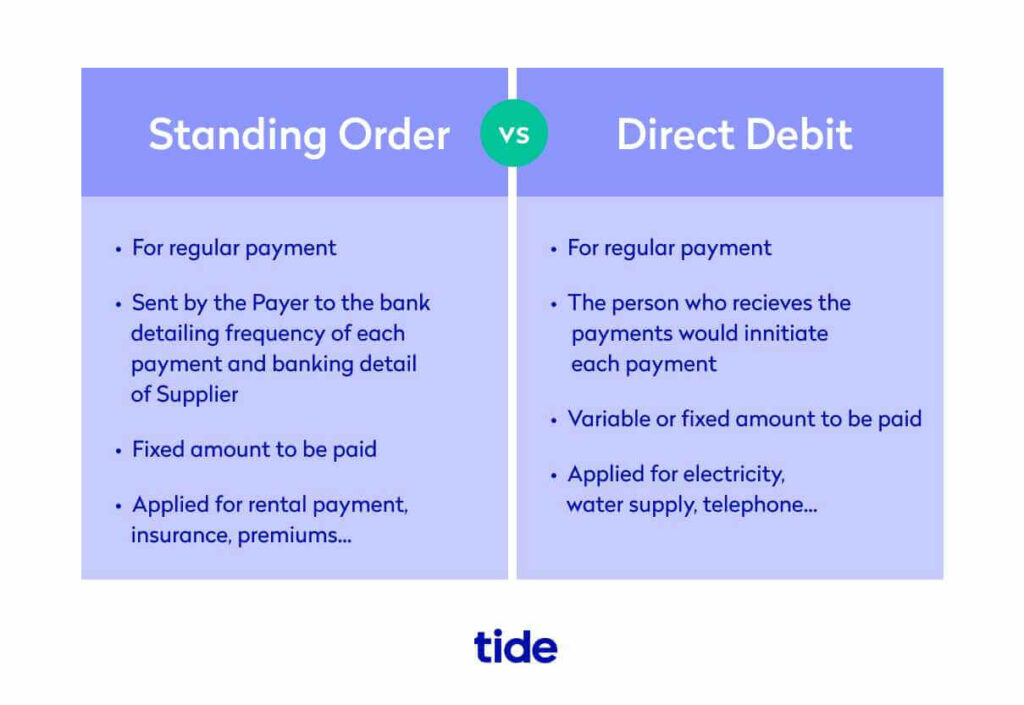

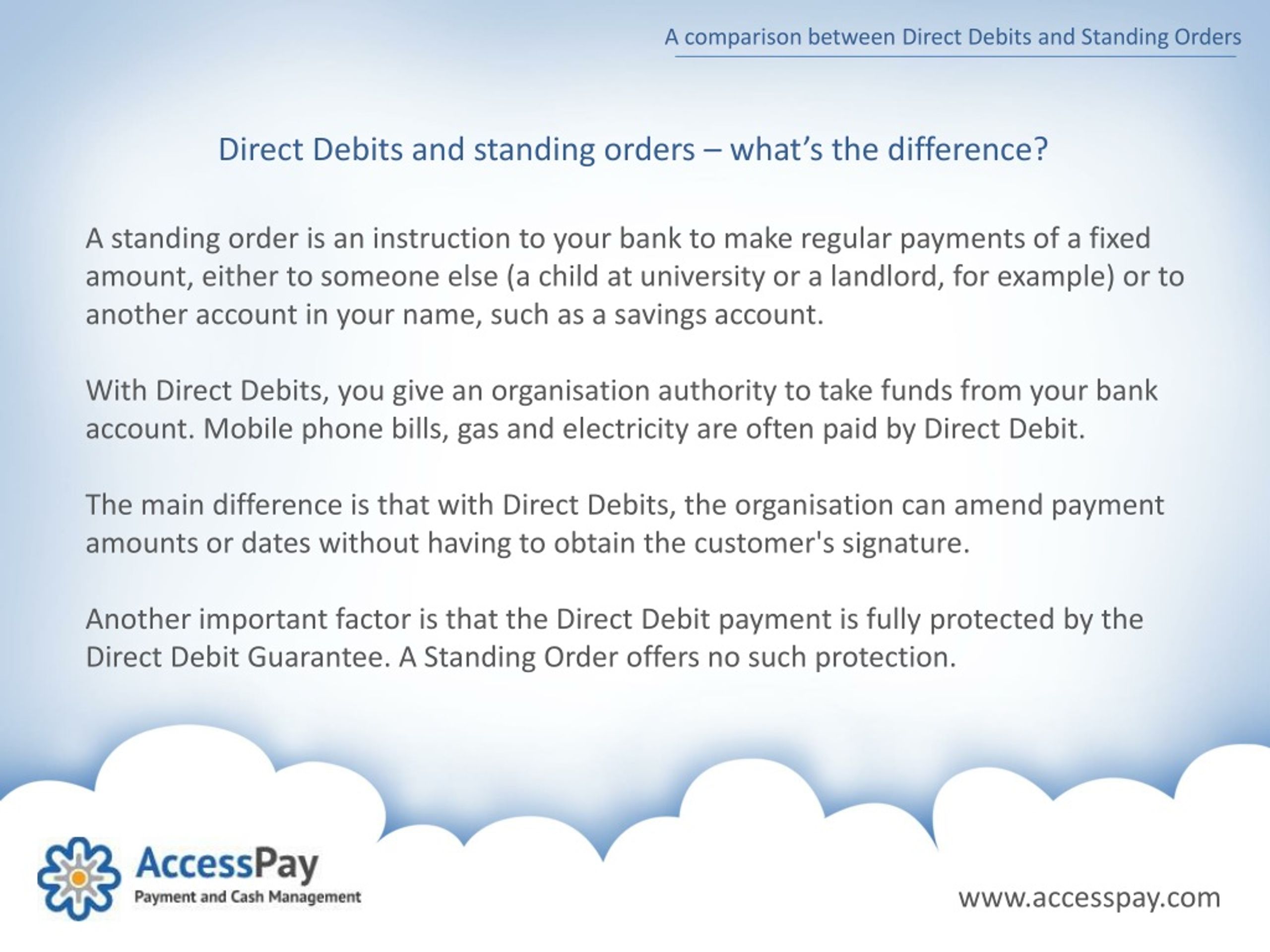

A standing order is an instruction you give to your bank to pay a fixed amount of money to a specific person or company on a regular, predetermined date. The key here is the fixed amount and the fixed date. It’s a set-it-and-forget-it kind of deal.

For instance, if you pay your rent to your landlord on the 1st of every month, and it's always the same amount, a standing order is perfect. You log into your online banking, set up the instruction: "Pay £800 to [Landlord's Name] on the 1st of each month, starting next month." And voilà! Your bank then takes care of it, like a diligent little financial assistant.

The beauty of a standing order is its predictability. You know exactly how much is going out and when. This makes budgeting a breeze. It’s like having a personal finance GPS that always points you in the right direction, telling you precisely when a certain outgoing payment will occur.

Practical Tip Alert! Standing orders are fantastic for things like:

- Rent or Mortgage Payments: Especially if your rent or mortgage is a consistent amount.

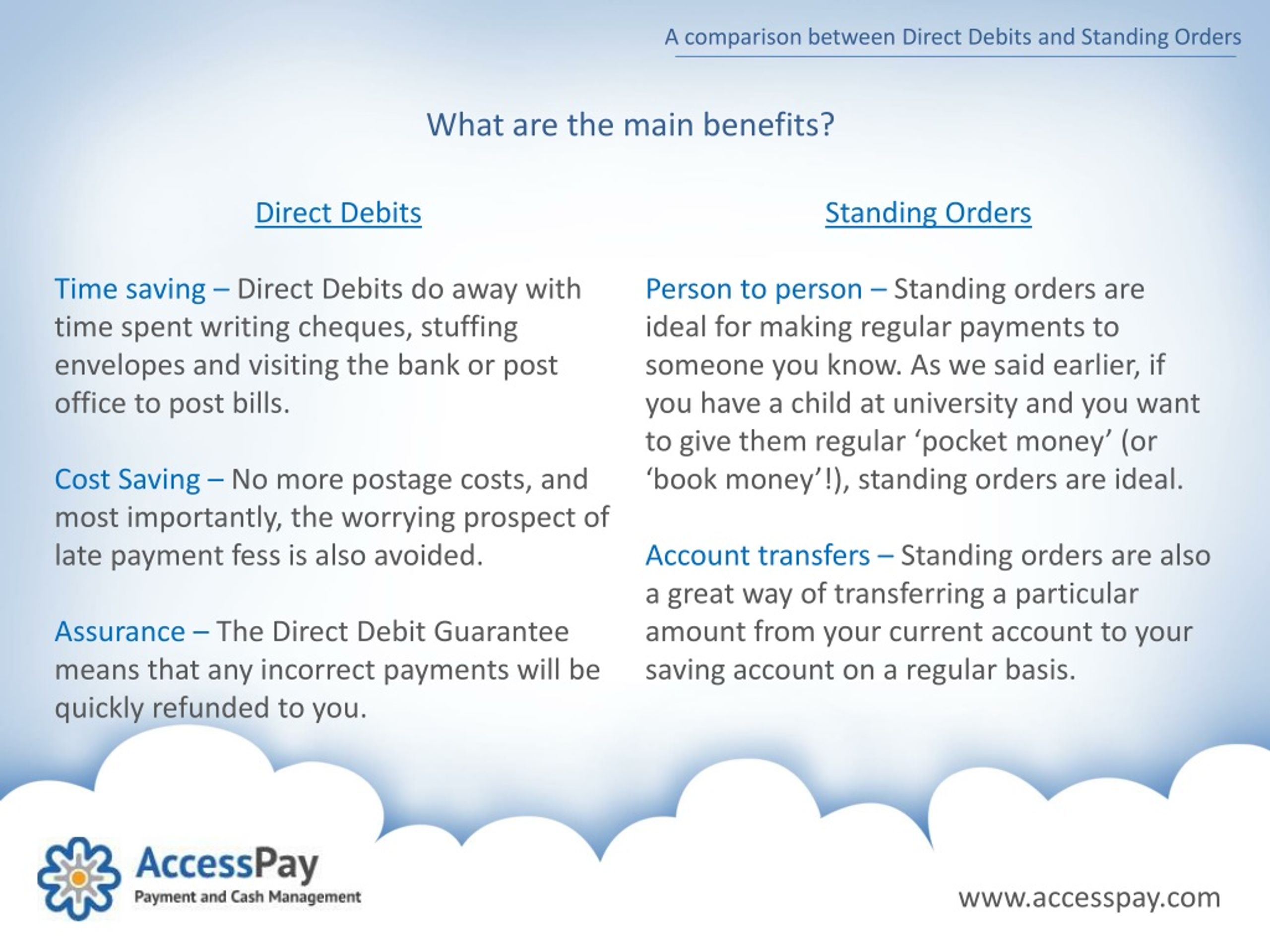

- Regular Savings Transfers: Want to put £100 into your savings account every payday? Set up a standing order! Your future self will thank you. Think of it as a little "treat yo' self" fund for a bigger goal, like that dream vacation to Bali or a new vintage record player.

- Regular Gifts to Family or Friends: Helping out a family member regularly? A standing order makes it effortless.

- Fixed Subscription Services (with fixed prices): If your gym membership is always £40 a month, and never changes, this works.

One of the biggest advantages of a standing order is the control it gives you. Because you set the amount and the date, and it’s all done through your bank, you're always in the driver's seat. You can easily adjust it, cancel it, or pause it directly through your banking app or by speaking to your bank.

Think of it this way: A standing order is like sending a meticulously crafted postcard. You’ve written the message, addressed it perfectly, and dropped it in the mail. It’s going to arrive on time, and the recipient will receive exactly what you sent. Simple, elegant, and you initiated the exact content.

A fun little fact? The concept of standing orders has been around for ages, evolving from simple written instructions to the digital precision we see today. It's a testament to the human need for reliable systems that just… work.

The Smooth Operator: Decoding Direct Debits

Now, let’s pivot to the Direct Debit. If a standing order is your reliable friend, a Direct Debit is more like your super-organized, but sometimes a little mysterious, personal assistant. It's authorized by you, but the company you’re paying has a bit more flexibility in how much and when they can request the payment, within agreed parameters, of course.

With a Direct Debit, you give a company permission to take money directly from your bank account. However, crucially, you must be notified in advance if the amount or date of the payment is going to change. This is a super important protection!

So, what’s the difference in practice? Let’s say you have a utility bill. Your gas or electricity usage can vary month to month. You can’t set up a standing order for a fixed amount because the bill will change. That’s where Direct Debit shines.

You authorize the utility company to take payment via Direct Debit. They’ll then tell your bank how much to pay and when, and your bank will execute it. But – and this is the big but – they have to give you a heads-up if they plan to change the amount. You’ll typically receive a statement or email a few days before the payment is due, informing you of the new amount. This is your chance to check if it looks right.

The key phrase here is "authorized by you". You sign a mandate (usually digitally these days) giving the company the right to collect payments. This mandate specifies what they can collect for and the agreed collection times.

When does a Direct Debit make the most sense?

- Variable Bills: Utility bills (gas, electricity, water), phone contracts, internet services.

- Subscription Services with Price Fluctuations: Think streaming services that might occasionally adjust their prices, or magazine subscriptions that might have special offers.

- Gym Memberships: Often these can change slightly with annual price reviews.

- Charitable Donations (variable amounts): If you pledge a certain amount that might change based on your circumstances or specific campaigns.

The biggest advantage of a Direct Debit is its flexibility for the company, which often translates to convenience for you. You don't need to manually update payment amounts or remember to make the payment each month. It just happens, and you're alerted to any changes.

And here’s a really cool safety net: the Direct Debit Guarantee. This is a promise offered by banks and building societies that participate in the Direct Debit scheme. It’s a pretty powerful piece of consumer protection:

- Immediate refund: If an error is made in the payment, you’ll be refunded immediately by your bank.

- Advance notice: You’ll be notified of any changes in the amount or date of the payment.

- Right to cancel: You can cancel a Direct Debit at any time by simply contacting your bank.

So, while the company initiates the collection, you have a robust safety net in place. It’s like giving your assistant permission to manage your schedule, but with a clear contract and a backup system that ensures you’re always informed and protected.

Think of a Direct Debit as ordering from your favorite online retailer. You give them your payment details once, and they can charge you for future orders (with your explicit consent, of course!). They’ll usually send you an order confirmation and shipping details, keeping you in the loop about what’s coming your way.

A fun cultural reference? The Direct Debit scheme is a cornerstone of modern payment systems in many countries, particularly the UK. It’s one of those unsung heroes that keeps our digital economy humming along smoothly, allowing businesses to manage cash flow and consumers to enjoy convenience.

The Big Showdown: Standing Order vs. Direct Debit – What’s the Vibe?

So, we’ve met our two financial players. Let’s put them side-by-side and see where they truly shine:

Standing Order: The Steady Eddy

- Control: You set the exact amount and date.

- Predictability: Great for fixed, regular payments.

- Simplicity: Easy to set up and manage through your bank.

- Best for: Rent, fixed savings, regular gifts, predictable subscriptions.

- Vibe: Reliable, consistent, like your favorite comfy sweater.

Direct Debit: The Flexible Friend

- Flexibility: Allows for variable amounts and dates (with notice).

- Convenience: Companies manage the collection, saving you manual effort.

- Protection: The Direct Debit Guarantee offers strong consumer rights.

- Best for: Utility bills, phone contracts, variable subscriptions, memberships.

- Vibe: Adaptable, convenient, like a subscription box that surprises you (in a good way!).

It’s not about one being inherently “better” than the other. It’s about choosing the right tool for the job. Think of it like choosing between a hammer and a screwdriver. You wouldn’t try to screw in a nail with a screwdriver, would you? Similarly, you wouldn’t use a Direct Debit for a fixed rent payment if you want complete control over the exact amount each time.

One of the most common mistakes people make is using the wrong one. Forgetting to update a standing order when a bill increases can lead to insufficient funds. Conversely, setting up a standing order for a variable bill can lead to under or overpayments. Paying attention to the nature of the payment is key!

Pro Tip: Regularly review your standing orders and Direct Debits. Are you still using that gym membership? Is that subscription still relevant? A quick check-in every six months can save you money and mental clutter. It’s like decluttering your digital life!

Some companies might offer you a discount for setting up a Direct Debit, as it guarantees them a consistent cash flow. So, it's always worth checking if there's a financial incentive!

And remember, for both, you can usually manage them through your banking app or website. Need to change an amount? Pause a payment? Cancel an instruction? It's typically just a few clicks away. It’s all about embracing that modern, streamlined approach to managing your money.

A Little Reflection for Your Day

Think about it: In a world that often feels chaotic and unpredictable, having these small, reliable systems in place for our finances is a form of quiet rebellion. It’s about creating order where we can, about outsourcing the mundane so we have more energy for the extraordinary. Whether it’s a standing order that ensures your savings grow steadily like a well-tended plant, or a Direct Debit that smoothly handles your ever-changing utility needs, these tools are designed to give you peace of mind.

They’re the financial equivalent of setting your coffee maker the night before or prepping your lunch on a Sunday. Small actions that make your weekdays just a little bit smoother, a little bit less stressful. So, the next time you’re setting up a payment, take a moment to consider: are you sending a perfectly crafted postcard, or are you empowering a trusted assistant? Either way, you’re taking a step towards a more effortless financial life. And who wouldn't want a little more of that?