Difference Between Balance Sheet And Profit And Loss Account

Ever feel like diving into your company's finances is like trying to assemble IKEA furniture blindfolded? You've got all these pieces, and you know they're supposed to fit together, but… where do you even start?

Well, buckle up, buttercup, because we're about to unpack two of the biggest players in the financial game: the Balance Sheet and the Profit & Loss Account. Think of them as your financial fairy godmothers, each with a very different kind of magic.

The Balance Sheet: A Snapshot of What You've Got (and Owe!)

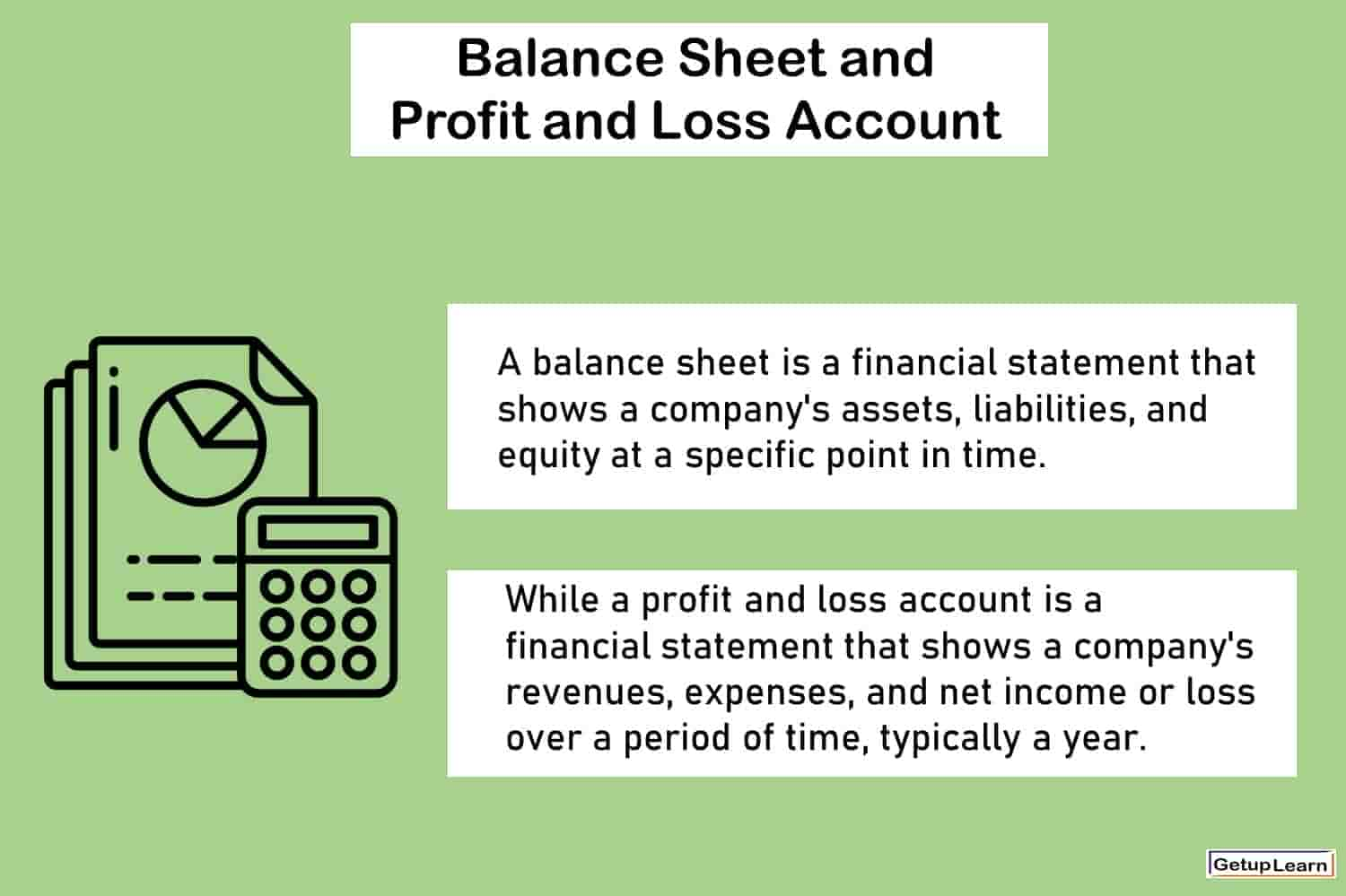

Let's start with the Balance Sheet. Imagine you're having a particularly good hair day and decide to take a selfie of your entire financial life. That's basically your Balance Sheet. It's a picture taken at a specific moment in time. Like, right now. Poof! It’s a snapshot.

So, what's in this financial selfie? Well, it's all about what your business owns, what it owes, and what's left over for you, the glorious owner. We call these Assets, Liabilities, and Equity. Easy peasy, right?

Assets are the shiny things your business has. Think of your cash in the bank (yay!), your fancy equipment (that coffee machine you swear is essential), maybe even that building you own. These are all the good bits that can be turned into cash, or at least help you make more cash. They're the "stuff" of your business.

Then come the Liabilities. These are the less glamorous bits. They’re the IOUs. The money you owe to others. Your credit card bills, loans from the bank, maybe that invoice you haven't paid yet. They’re the "whoops, I gotta pay this" items.

And finally, the grand finale: Equity. This is the owner's share. It's what's left after you've paid off all your debts. It’s your stake in the game. If you sold everything your business owned and paid off everyone it owed, this is what you’d walk away with. It's your reward for all the hustle.

The golden rule of the Balance Sheet, the thing that makes it… well, balance… is this: Assets = Liabilities + Equity. It’s like saying, "All the stuff I have equals what I owe plus what’s mine." It always, always, always has to add up. No fudging allowed!

Think of it like your personal bank account statement at the end of the month. It shows what you have in your account (assets), what you owe (liabilities on your credit card), and your actual net worth (equity).

So, the Balance Sheet tells you the financial health of your business at a single point in time. Is it strong? Is it teetering? Are you drowning in debt or rolling in dough? It’s the ultimate financial check-up.

The Profit & Loss Account: The Story of Your Money Making (or Losing!)

Now, let’s switch gears and meet the Profit & Loss Account, also known as the Income Statement. If the Balance Sheet is a snapshot, the P&L is the blockbuster movie of your business's financial journey. It tells a story over a period of time. We're talking months, quarters, or a whole glorious year.

This is where we see if your business is a rockstar making a fortune or a sad trombone playing out of tune. It’s all about Revenue and Expenses.

Revenue (or Income) is the sweet, sweet money you earn from doing your business thing. This is the cash rolling in from selling your products, providing your services, or whatever magical service you offer. It's the 'money coming in' section.

Expenses are the costs of doing business. This is the money you spend to make that revenue. Think of your rent, your salaries (yes, you have to pay yourself and others!), your marketing costs, your electricity bills, even that very necessary fancy coffee machine we mentioned earlier. These are the 'money going out' items.

The magic here is simple: Revenue - Expenses = Profit (or Loss). If your revenue is bigger than your expenses, congratulations! You’ve made a profit. Cue the confetti cannons!

If your expenses are bigger than your revenue… well, that's a loss. Sad trombone sound intensifies. Don't despair, it happens! The P&L just tells you the story so you can figure out how to turn things around.

Think of it like your monthly electricity bill. It shows how much you used (revenue equivalent for the power company) and how much they charged you (their expenses to generate power). The difference is their profit (or loss, if they're having a bad month!).

The Profit & Loss Account shows you how well your business is performing over a period. Is it generating enough cash? Are your costs under control? It’s your business’s performance review.

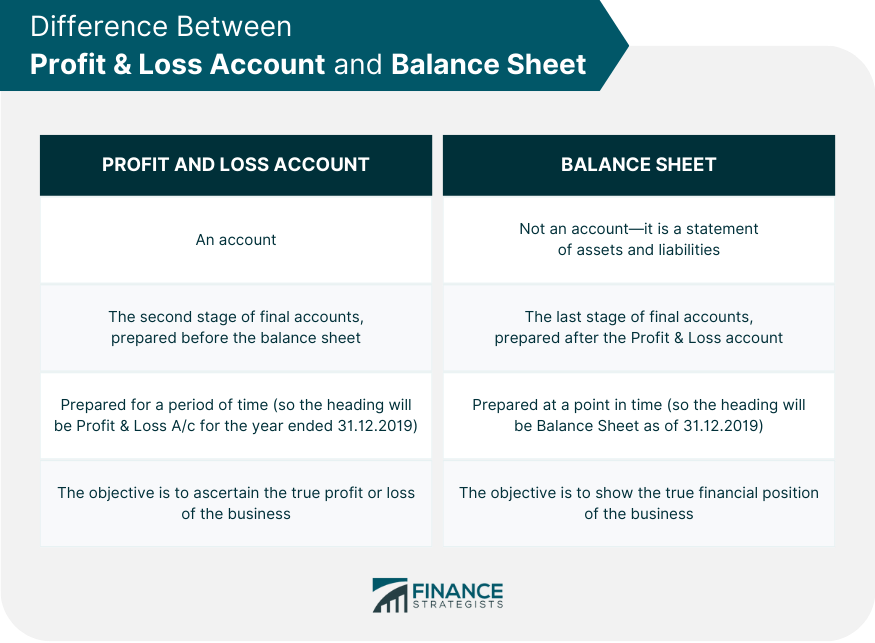

So, What's the Big Difference?

Here's the juicy gossip: The Balance Sheet is a snapshot at a point in time. The P&L is a story over a period of time.

The Balance Sheet shows your financial position – what you have and what you owe. The P&L shows your financial performance – how much money you made or lost.

And here’s a little secret: The Profit (or Loss) from your P&L feeds into your Equity on the Balance Sheet. So, they are connected! They're not competing, they're collaborating. It's like a financial buddy-cop show. One is the 'who you are' detective, the other is the 'what you've done' investigator. They both help you understand your business better.

So, next time you're faced with financial statements, don't panic. Just remember the selfie (Balance Sheet) and the movie (P&L). You've got this!