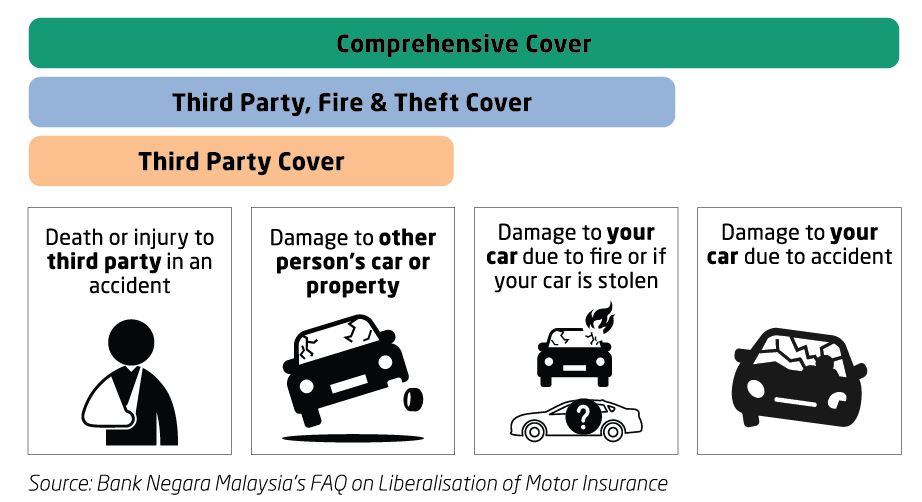

Difference Between Comprehensive And Third Party Fire And Theft

Alright, let's spill the tea on car insurance. Specifically, the difference between those two fancy-sounding options: Comprehensive and Third Party Fire and Theft. Sounds like a mystery novel title, right? "The Case of the Missing Fender: A Comprehensive Investigation." Or maybe, "Burn, Baby, Burn: The Third Party, Fire, and Theft Caper."

But honestly, it's not that dramatic. Think of it like ordering pizza. You've got your basic cheese, and then you've got the works. This is kind of like that, but for your beloved set of wheels.

Let's dive in, shall we? Grab a cuppa, settle in, and let's demystify this whole insurance shindig. It’s actually kind of fascinating when you think about it. Like a little puzzle for your brain.

The Grand Slam: Comprehensive Cover

So, Comprehensive. What's the big deal? Imagine your car is a superhero. This insurance gives your superhero all the powers. It's the full package. The whole nine yards. The cat's pajamas.

What does this mean for your everyday driving? Well, if your car gets dinged, dented, or even totally trashed, Comprehensive is your knight in shining armor.

Did a rogue shopping cart perform a kamikaze mission on your passenger door? Bam! Comprehensive. Did a flock of pigeons decide your car was the perfect target for a synchronized bombing raid? Oh dear! Comprehensive.

But it's not just about your car's woes. It also covers things you might not even think about. Like if your car gets stolen. Poof! Gone. Don't panic. Comprehensive to the rescue. Or if it catches fire. Yikes! Again, comprehensive has your back.

Think of it this way: if something happens to your car that's not caused by another driver hitting you, then Comprehensive is likely your hero. It’s for those unexpected, "what on earth just happened?!" moments.

It even covers things like vandalism. Someone decides to draw a magnificent mustache on your car with permanent marker? Classic. Comprehensive will help you get it fixed. Or if your car slides off the road in a blizzard and ends up looking like a snow sculpture. Yep, comprehensive. It’s the ultimate protection.

The quirky fact? Sometimes, this coverage can be surprisingly affordable. Don't just assume it's way more expensive. Shop around! You might be pleasantly surprised. It's like finding a tenner in an old coat pocket.

The key takeaway here is breadth. It covers a lot. It’s for when you want peace of mind and don't want to be left holding the bag (or the broken headlight) if something bad happens, no matter how it happens.

The "Oops, I Didn't Mean To!" Option: Third Party Fire and Theft

Now, let's talk about Third Party Fire and Theft. This is like a slightly more focused superhero. It’s got some cool powers, but not all of them. It’s a solid choice for many people, and there's a good reason for it.

The "Third Party" part is crucial here. This is all about protecting other people if you’re involved in an accident. If you cause damage to someone else’s car or injure someone, this cover steps in to pay for it. It’s the polite, responsible thing to do. It’s your good neighbor policy.

Think of it as saying, "Oops! My bad!" and then your insurance card happily deals with the other person's damages. No need for you to dig into your savings to pay for their bumper. Phew!

But here's where the "Fire and Theft" comes in. This is the extra bit that makes it more than just basic third-party cover. So, if your car gets stolen? Poof! This cover helps you out. If your car goes up in flames (hopefully not literally!), this cover is there for you too.

So, it protects others if you're at fault, and it protects your car from two specific, rather dramatic, misfortunes: fire and theft. It’s like a two-for-one deal for those particular worries.

What's missing from the comprehensive superhero's cape? Well, it doesn't cover damage to your car if it's involved in an accident that's your fault, or if it’s damaged by things like falling branches, hail, or that mischievous shopping cart we mentioned earlier. It’s not for those random, non-malicious bumps and bruises your car might endure.

It’s a bit like ordering a pizza with pepperoni and mushrooms, but without the extra cheese and olives. You get the good stuff, but not everything. It's a smart choice if you’re looking for decent protection without necessarily needing the absolute maximum coverage.

The funny detail? Sometimes people get confused and think "Third Party" covers everything except their own car. Not quite! It covers other people and then adds the fire and theft protection for your car. See? Nuance is fun!

So, Which One Should You Choose?

This is the million-dollar question, isn't it? Or at least, the several-hundred-dollar question.

Comprehensive is for the cautious soul. The one who wants to sleep soundly at night knowing that no matter what curveball life (or a rogue squirrel) throws at their car, they're covered. It's for newer cars, expensive cars, or if you just have that "better safe than sorry" mentality.

Third Party Fire and Theft is for the pragmatist. The one who understands the importance of covering other people and wants protection against the big, scary "F" and "T" words. It's a popular choice for older cars where the cost of comprehensive might outweigh the car's value, or if you're confident in your driving and happy to accept a bit more risk for your own car's minor mishaps.

Think about the value of your car. If it’s a classic beauty that’s worth a fortune, you probably want the full superhero treatment. If it’s a trusty old steed that gets you from A to B and has a few battle scars already, Third Party Fire and Theft might be your best friend.

It’s also about your personal risk tolerance. Are you someone who worries about every little scratch, or do you embrace the character that comes with a few dings? Your personality plays a role!

The most important thing? Do your research. Get quotes for both. Compare the prices and the exact terms. Don't be afraid to ask questions. Insurers are there to help you navigate this stuff. It's not a secret code. It's just a product!

At the end of the day, both options offer valuable protection. It’s just about finding the right fit for your wallet and your peace of mind. So, go forth, and get insured! Your car (and your future self) will thank you.