Difference Between Current Account And Savings Account

Alright, settle in, grab your latte, and let's talk about something that might sound drier than a week-old scone, but trust me, it's more interesting than you think. We're diving headfirst into the epic saga of the Current Account versus the Savings Account. It's like the superhero showdown of your finances, with one being all about action and the other a chill, wise old mentor.

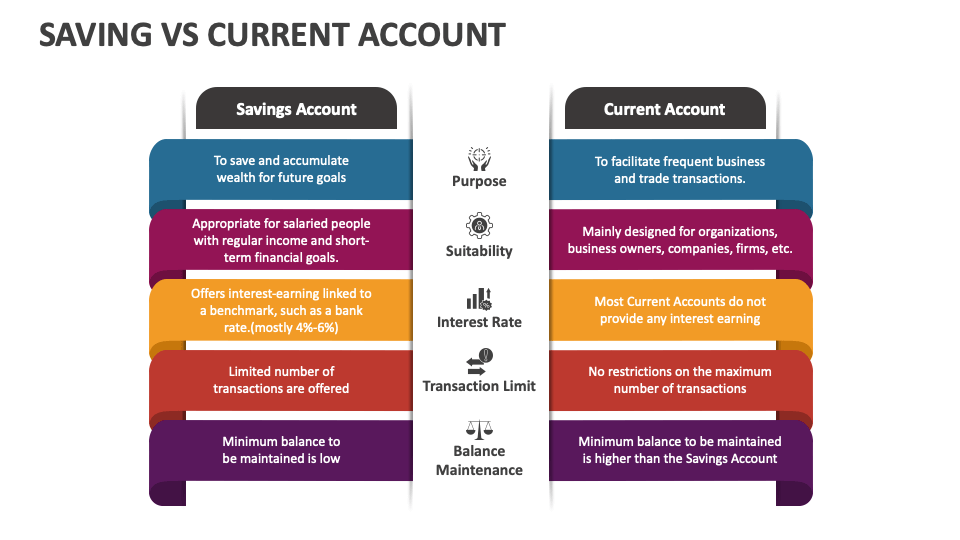

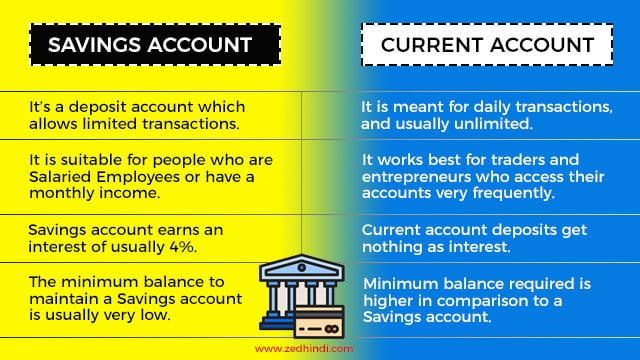

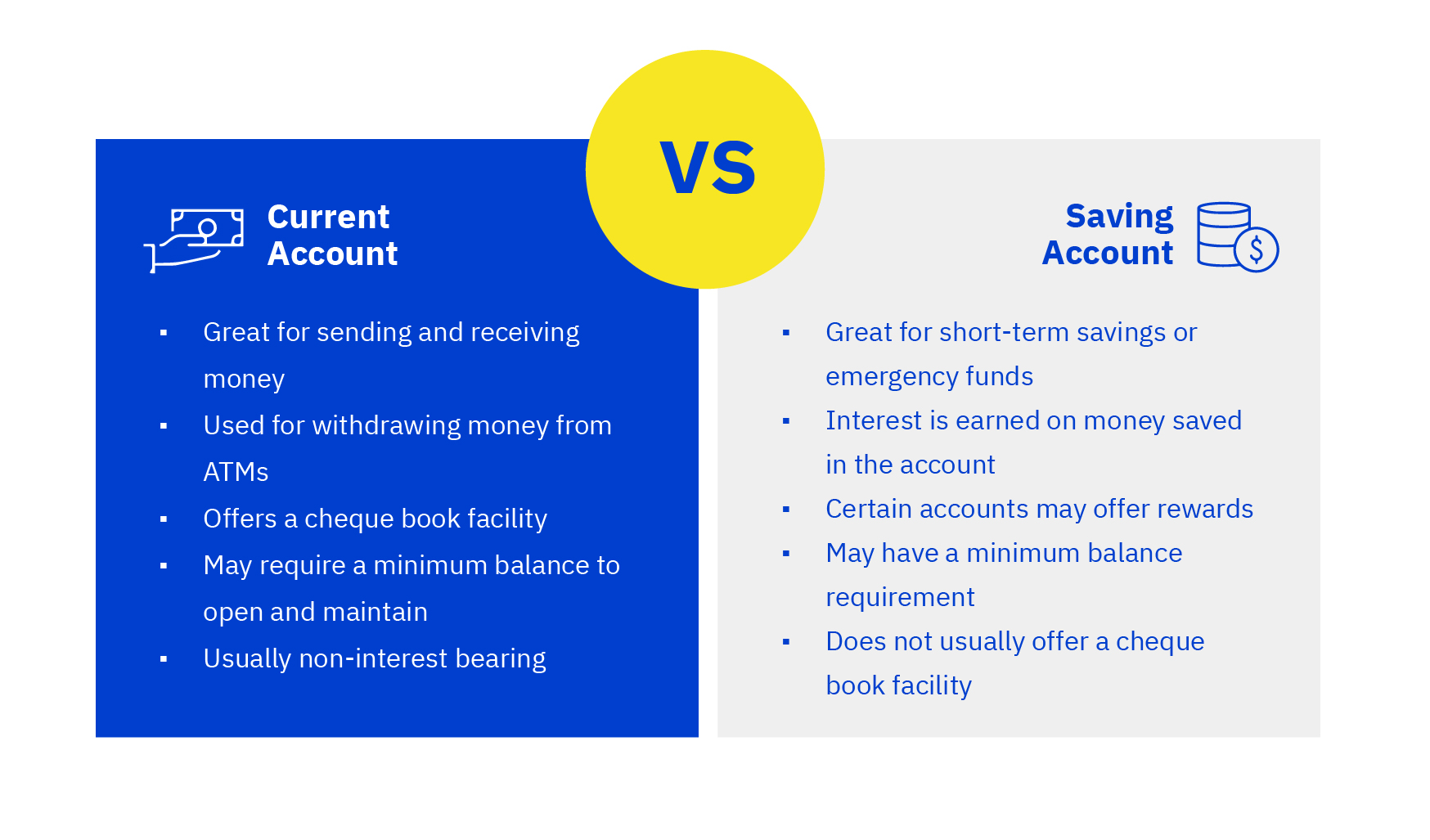

Imagine your money has two homes. One is a bustling city apartment where everyone’s coming and going, paying bills, buying pizza, maybe even launching a rocket to the moon (okay, maybe not the rocket). That’s your Current Account. It’s your daily driver, your workhorse, the place where your paycheck lands and then promptly goes on a wild adventure.

Think of it as your 'get-stuff-done' account. Need to pay your rent? Bam! Current account. Splurge on that ridiculously overpriced avocado toast because, #treatyourself? Current account. Accidentally buy a unicycle online at 2 AM? You guessed it. Current account. It’s built for frequent transactions. You can whip out your debit card like a ninja star, set up direct debits faster than a cheetah chasing a gazelle, and transfer money with the speed of light.

The downside? Well, this action-packed life doesn't exactly earn you a Nobel Prize in finance. You'll probably earn a whopping zero interest, or something so minuscule it’s practically a cosmic joke. It's like giving your money a job and then telling it, "Nope, no bonus for you, sunshine!"

Now, let's switch gears to the other contender. Meet the Savings Account. This one is the polar opposite of the frantic city apartment. It’s more like a serene, sun-drenched villa in the countryside, where your money can kick back, relax, and maybe even do some yoga.

This account is all about long-term goals. Think of it as your money's retirement plan, or its college fund for your future robot butler. You deposit money here with the intention of leaving it be, letting it grow like a prize-winning pumpkin. Because here's the magical part: this sleepy account actually pays you.

Yes, you heard that right. It offers interest. It's like your money is out there working a side hustle while you're busy living your best life, and then it comes back with a little extra cash. It might not be enough to buy a private island overnight, but over time, it can add up. Plus, the interest rates on savings accounts are usually higher than those on current accounts, proving that sometimes, patience does pay off. Who knew?

However, there's a catch, as there usually is in life (and in banking). This peaceful haven isn't designed for your everyday spending spree. If you try to make too many withdrawals or transactions from your savings account, your bank might give you the side-eye, or worse, slap you with some fees. It’s like trying to order a triple-decker cheeseburger at a meditation retreat – it just doesn't fit the vibe.

So, what’s the surprising truth? Most of us need both.

The Dynamic Duo of Doom... for Debt!

It’s not about picking a side; it’s about having a strategic partnership. Your current account is your trusty steed, always ready for action, allowing you to manage your day-to-day life without a hitch. It's where the magic of online shopping and bill payments happens. Without it, you'd be back to bartering with squirrels for nuts, and let me tell you, their exchange rates are brutal.

And your savings account? That’s your financial superpower, your secret weapon for building wealth. It’s where your emergency fund sits, waiting patiently to save you from that dreaded "oh no, my car just ate my rent money" moment. It's also where you stash away cash for that dream vacation or that ridiculously expensive espresso machine you’ve been eyeing.

A Little Fun Fact to Blow Your Mind (or at least mildly surprise you):

Did you know that some banks actually have different types of savings accounts? There are the regular ones, then there are the fixed-deposit accounts where you lock your money away for a set period, usually in exchange for a slightly higher interest rate. It's like putting your money in a time capsule. You can't touch it, but you know it's going to be worth a little more when you finally dig it up!

The Verdict (Spoiler Alert: It's Teamwork!)

Think of your current account as your wallet, always accessible and ready for immediate needs. Your savings account is like your safe deposit box, holding onto your valuable assets and growing them over time.

So, the next time someone asks you about the difference, you can confidently say, "Ah, that's easy! One is for living in the fast lane, the other is for planting roots and watching them grow. And honestly, who wouldn't want both a speedy sports car and a peaceful garden?"

It’s about using each account for its intended purpose. Keep your daily spending in your current account and let your savings account do its thing in the background, earning you a little extra moolah. It’s not rocket science, but it’s certainly a smart way to keep your finances humming along like a well-oiled, surprisingly profitable machine. Now, go forth and manage your money like the financial wizard you are! And maybe treat yourself to that second coffee. You've earned it.