Does Having Multiple Bank Accounts Affect Credit Score

Hey there, ever found yourself wondering about all those little things that might be nudging your credit score up or down? It's like a financial mystery novel sometimes, isn't it? We're all trying to keep our financial ducks in a row, and one question that pops up now and then is: does having a bunch of different bank accounts actually mess with our credit score? Let's dive into this with a cup of coffee (or tea, no judgment!) and figure it out together.

Think of your credit score like your financial report card. The higher the grade, the more lenders see you as a responsible borrower, and that can mean easier approvals for loans, better interest rates on mortgages or car payments, and even sometimes cheaper insurance. So, it's definitely something worth paying attention to!

Now, about those bank accounts. You know, the checking account for your daily latte habit, a savings account for that rainy day fund (or maybe a new gadget fund!), a joint account with your partner for household bills, and maybe even a separate account for your freelance side hustle. It can start to feel like you've got a whole little network of financial hubs.

Here's the really good news, and I'm going to say it loud and clear: Having multiple bank accounts generally does NOT directly affect your credit score.

Let that sink in for a moment. It’s a bit like having a toolbox with different tools for different jobs. You wouldn't use a hammer to screw in a lightbulb, right? Similarly, your checking and savings accounts are for different purposes, and having them separate is smart money management, not a credit score red flag.

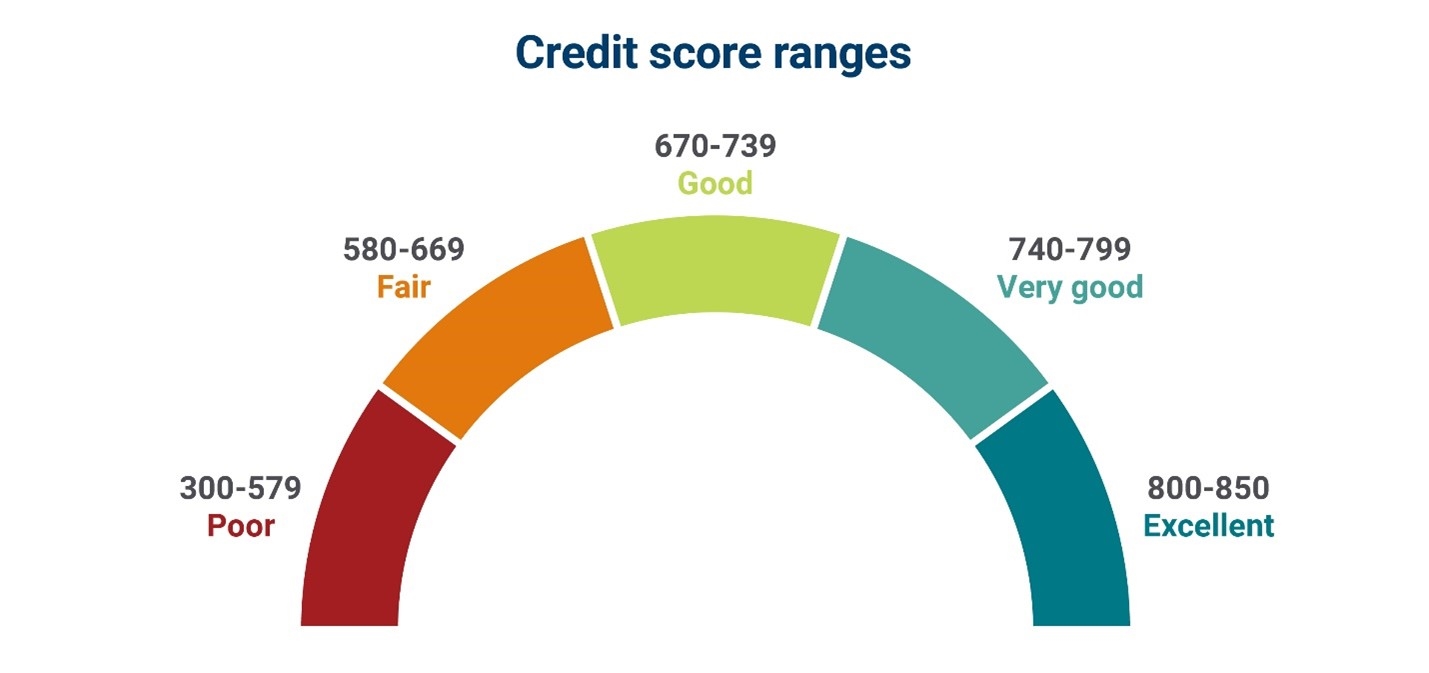

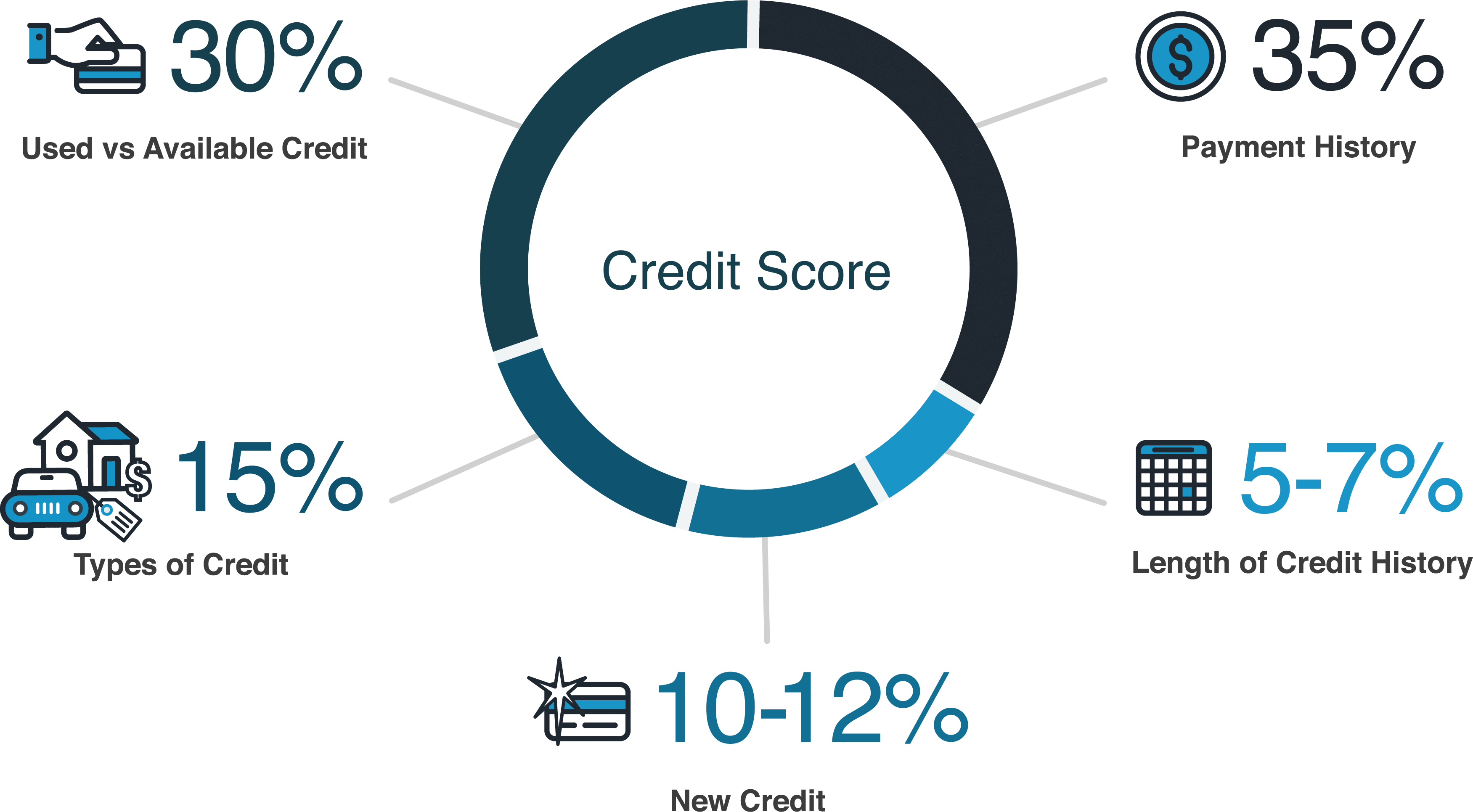

Credit scores are primarily built around how you manage credit. We’re talking about things like:

- Credit cards: How often you use them, how much you owe, and if you pay on time.

- Loans: Like mortgages, car loans, or personal loans. Again, the key is responsible repayment.

- Payment history: This is the biggie! Making payments on time is crucial.

- Credit utilization: How much of your available credit you're actually using.

- Length of credit history: The longer you've been responsibly managing credit, the better.

- Types of credit: Having a mix of different credit types (like credit cards and installment loans) can be a good thing.

Your bank accounts, on the other hand, are more about managing your cash flow and savings. They show how you're handling the money you have, not the money you've borrowed.

Let's paint a picture. Imagine Sarah. Sarah has her main checking account where her salary lands and bills get paid. Then she has a separate savings account where she squirrels away money for her annual vacation to the beach. She also has a joint checking account with her husband, Mark, to manage their mortgage and groceries. And because she's a whiz at knitting and sells her creations online, she even has a small business checking account for her Etsy shop income and expenses. Does this sound like a person who's going to get penalized by the credit bureaus? Nope!

In fact, Sarah is probably doing a fantastic job of managing her finances. Separating funds can actually make it easier to track spending, save effectively, and avoid overdraft fees (which, by the way, can indirectly impact your financial health, but not your credit score directly unless those overdrafts lead to collections or other issues).

Think about it this way: if you had one giant pot of money for everything, it might be tough to see how much you're really spending on fun stuff versus essential bills. Or how much you're actually setting aside for that down payment on a house. Having multiple accounts is like having clearly labeled drawers in a dresser – everything is organized and easy to find.

So, why should you care about this little tidbit of information? Well, for starters, it means you don't have to stress about consolidating your accounts unnecessarily if you like your current setup. If having a dedicated account for travel savings makes it easier for you to reach your goals, go for it! If separating business and personal finances simplifies your bookkeeping, that's a win!

It also helps you understand what actually matters for your credit score. Instead of worrying about the number of bank accounts, you can focus your energy on the things that truly move the needle: paying bills on time, keeping credit card balances low, and reviewing your credit reports for any errors.

However, there's a tiny, almost microscopic, caveat. While having multiple accounts doesn't hurt your credit score, opening a new bank account might sometimes involve a "soft inquiry" on your credit report. This is different from a "hard inquiry" that happens when you apply for credit. Soft inquiries are usually for things like background checks or pre-approved offers and typically don't impact your score. Most banks don't even do a credit check for a basic checking or savings account anymore, but it's always good to be aware.

The main thing to remember is that your bank accounts are your personal financial management tools. They reflect your day-to-day financial habits, not your creditworthiness. Lenders are interested in how you handle borrowed money over time. They want to see a pattern of responsibility, not the number of places your paycheck is deposited.

So, feel free to organize your money in a way that makes sense for you! Whether you have two accounts or ten, as long as you're responsibly managing any credit you have, your credit score will be just fine. It’s all about making smart choices and keeping your financial life as organized and stress-free as possible. Keep up the great work on your financial journey!