Does Transferring Credit Card Balances Affect Credit Score

Hey there, credit card wranglers and money-savvy folks! Ever found yourself staring at a pile of credit card statements, feeling a little like a juggler trying to keep too many balls in the air? You know, the ones with those tempting low introductory APR offers that whisper sweet nothings about saving you money? Well, let's dive into one of the most common questions buzzing around the financial grapevine: does transferring credit card balances actually mess with your credit score?

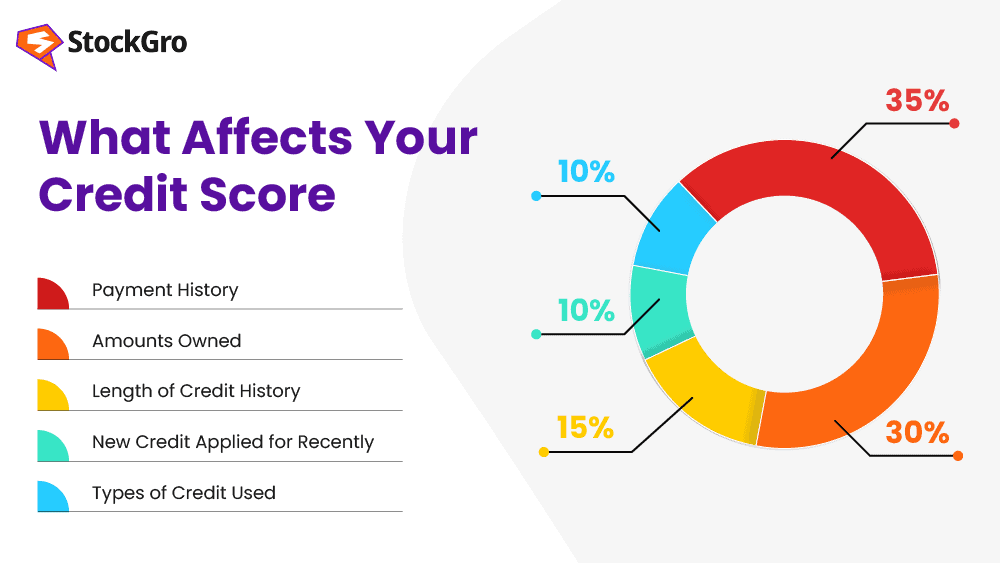

Think of your credit score as your financial report card. It's what lenders, landlords, and sometimes even potential employers look at to get a quick snapshot of how reliably you handle your money. And just like you wouldn't want to see a doodle of a grumpy cat next to your report card grade, you definitely want your credit score to be looking its best.

The Balance Transfer Tango: What's the Deal?

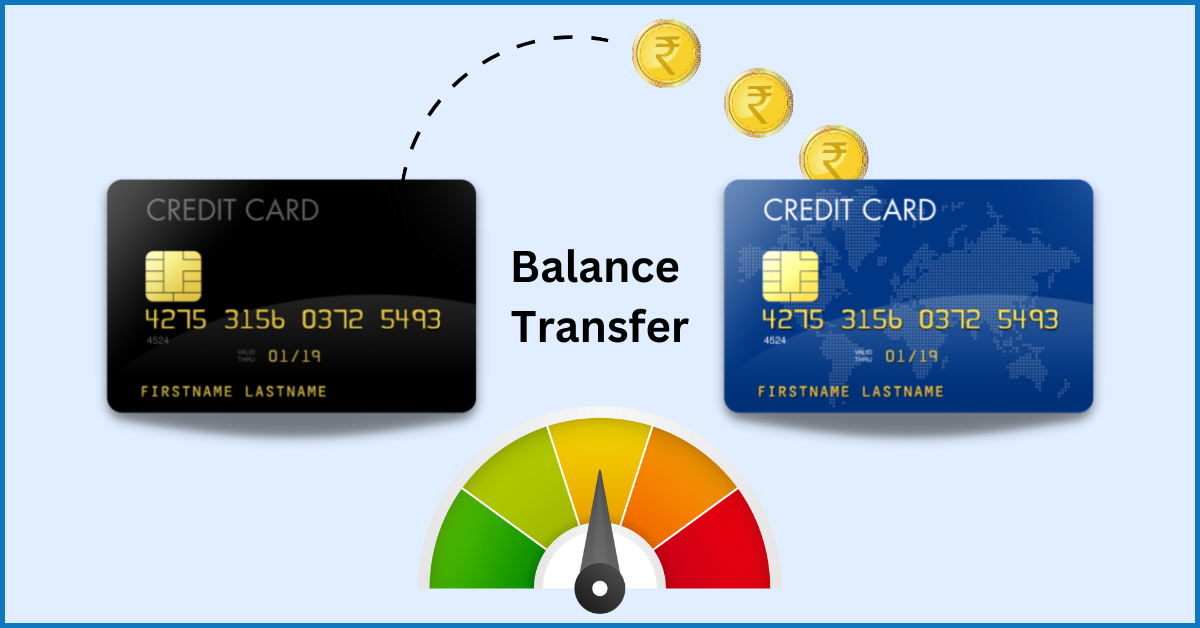

So, what exactly is a balance transfer? Imagine you've got a couple of credit cards, both with balances that are starting to feel like a heavy backpack. One might have a sky-high interest rate, making it feel like you're paying more for that fancy dinner you bought last year than the actual meal itself! Another might be just fine, but you're looking to simplify things.

A balance transfer is like packing up all the items from those two backpacks and neatly arranging them into one, hopefully, much lighter and more organized, suitcase. You take the balance from one (or more!) credit cards and move it to a new credit card, often one that boasts a sweet, sweet 0% introductory APR for a set period. The idea is to give yourself some breathing room to tackle that principal debt without the pesky interest piling up like laundry.

So, Does This Move Affect Your Score? Let's Spill the Beans!

The short answer is: yes, it can, but it's not necessarily a bad thing! It's more like a little shuffle on the dance floor of your creditworthiness. It’s not a permanent scar; it’s more of a temporary swirl.

Let's break down the ways it can ripple through your credit score:

1. The New Account Opening Effect: A Little Dip, Perhaps?

When you open a new credit card account to do that balance transfer, it’s recorded on your credit report. This is similar to applying for any other line of credit, like a car loan or a mortgage. Every time you apply for new credit, there's a hard inquiry. These inquiries can cause a small, temporary dip in your credit score, usually just a few points. Think of it like the first time you tried to parallel park a stick shift – a little jerky at first, but you get the hang of it.

This effect is usually minimal, especially if you have a strong credit history. Credit scoring models understand that people sometimes open new accounts. So, while there might be a tiny blip, it's generally not the end of the world. Your credit score is a marathon runner, not a sprinter; a small hurdle won't derail it.

2. The Credit Utilization Ratio: Where the Real Magic Happens

This is a biggie and often the most significant way a balance transfer can impact your score. Your credit utilization ratio is the amount of credit you're using compared to the total credit available to you. It's calculated by dividing your total outstanding balances by your total credit limits.

For example, if you have two cards with $5,000 limits each, your total available credit is $10,000. If you owe $2,000 on one and $3,000 on the other, your total debt is $5,000. That's a 50% utilization ratio ($5,000 / $10,000). Experts generally recommend keeping this ratio below 30%, and ideally, below 10% for the best scores.

Now, imagine you transfer that $5,000 balance to a new card with a $10,000 credit limit. Your old cards will now have a $0 balance (hooray!), and your new card will have a $5,000 balance. Let's say this new card has a $10,000 limit.

On the old cards, your utilization drops to 0%! That's fantastic. On the new card, your utilization is 50% ($5,000 / $10,000). This can be a bit of a mixed bag. If you managed to consolidate a high utilization from multiple cards onto one, and the new card has a generous limit, you might actually see your overall utilization ratio improve!

Think of it like this: you've got a messy closet with clothes spilling out of three drawers. You decide to organize everything into one big, beautiful wardrobe with plenty of space. Your closet (your credit utilization) might look much tidier and more manageable afterwards. This improved utilization can be a real boost to your credit score.

3. Closing Old Accounts: A Potential Misstep

Now, here's a little cautionary tale. Sometimes, people think, "Great! I've moved my balance. I don't need this old card anymore. Let's close it!" While it might seem like decluttering your financial life, closing an old credit card can actually hurt your credit score, especially if that card has a long history and a good payment record.

Why? Two reasons. First, it reduces your total available credit. If you had a $5,000 limit on that card you closed, and your total available credit was $20,000, it now drops to $15,000. If your balances stay the same, your credit utilization ratio will automatically go up. It’s like taking away one of the shelves in your wardrobe – suddenly, everything feels more crammed!

Second, the length of your credit history is a factor in your score. Older accounts, especially those managed well, demonstrate a longer track record of responsible credit use. Closing a well-established account can shorten your average credit history length, which isn't ideal.

So, if you're doing a balance transfer, it's usually better to keep those old accounts open, especially if they don't have annual fees. Just use them sparingly for small purchases and pay them off quickly to keep them active.

4. Payment History: The Unchanging King

Here's the good news: the act of transferring a balance doesn't directly affect your payment history. Your payment history is built on whether you pay your bills on time. As long as you continue to make your minimum payments (or, ideally, more!) on the new card where you transferred your balance, and keep up with any other accounts you have, your payment history will remain strong. This is the single most important factor in your credit score, so staying on top of your payments is paramount.

Who Benefits Most from a Balance Transfer?

People who are serious about paying down debt and can take advantage of a 0% APR period are prime candidates. If you have a plan to aggressively pay off the transferred balance before the introductory period ends, you can save a significant amount of money in interest. It's like finding a shortcut on a long road trip – you get to your destination faster and with less fuel!

It's also a great option if you're feeling overwhelmed by multiple high-interest payments. Consolidating can bring peace of mind and a clearer path to financial freedom.

The Takeaway: Balance Transfers are Tools, Not Magic Wands

So, does transferring credit card balances affect your credit score? Yes, it can. But usually, it's a manageable effect, and often, it can even lead to an improvement in your credit utilization ratio, which is a powerful score booster. The key is to be informed, have a plan, and understand how it all works.

Think of it like this: a balance transfer is a financial tool. Used wisely, it can help you save money and get out of debt faster. Used carelessly, it could have some minor downsides. Just remember to do your research, compare offers, and always, always prioritize paying off that debt. Happy transferring, and here's to a healthier credit score!