Does Your Homeowners Insurance Go Up After A Claim? Answered

Hey there, homeowners! Let's talk about something that probably makes your eyes glaze over faster than a lecture on tax depreciation: homeowners insurance. Specifically, the big question that pops into your head after, say, a rogue squirrel decides your attic is its personal nut-burying factory, or a surprise hailstorm turns your perfectly good roof into a colander. Does filing a claim mean your premiums are going to skyrocket?

It's a fair question, and one that can feel a bit like navigating a minefield. You've just dealt with a stressful situation – maybe your washing machine decided to redecorate your laundry room with a tidal wave of suds, or a tree branch, with the dramatic flair of a Shakespearean actor, took a nosedive into your prize-winning petunias. The last thing you want is another headache, and for many of us, that headache comes in the form of a potentially higher insurance bill.

So, let's break it down, nice and easy. The short answer is: yes, it's possible that your homeowners insurance could go up after a claim. But here's the good news: it's not always a guaranteed "Houston, we have a problem!" situation. Think of it like this: you've had a little bump in the road. The insurance company is trying to figure out if it was a fender bender or a full-on highway pile-up.

Why Your Insurance Company Cares (More Than You Might Think)

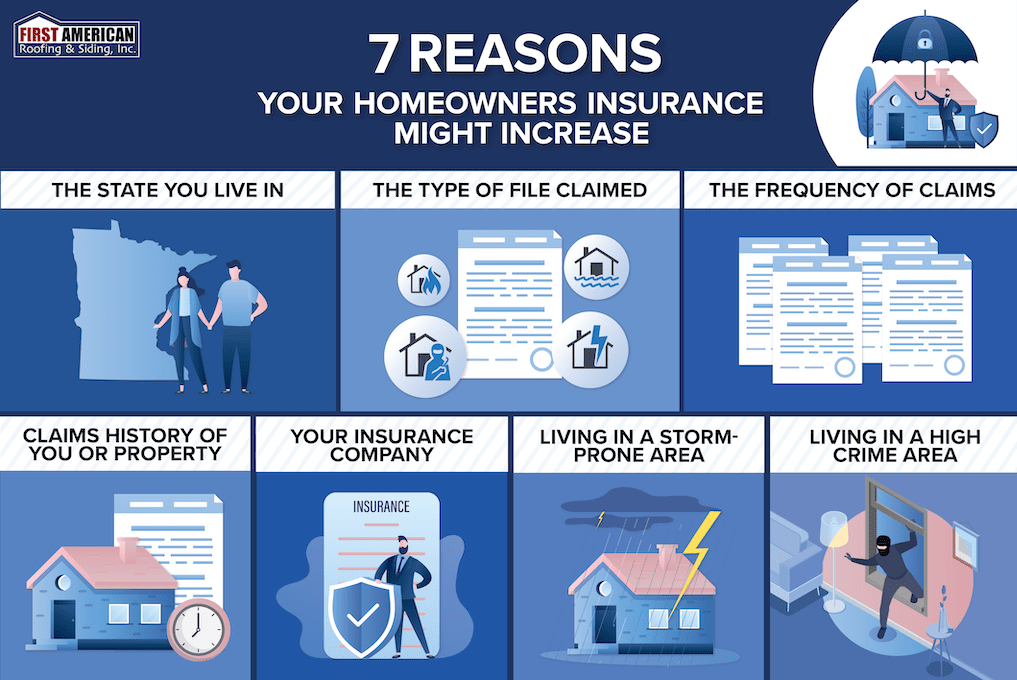

Insurance companies are in the business of managing risk. They pool money from a lot of people to pay out for the claims of a few. When you file a claim, you're essentially tapping into that pool. From their perspective, if you've had one incident, there's a slightly higher chance you might have another. It's not personal; it's just math. They're trying to predict future payouts based on past events.

Imagine you're at a potluck. If one person brings a dish that's a little... questionable, and then the next week, they bring another one that's even more questionable, you might start giving their contributions a wide berth at future gatherings, right? Insurance companies are kind of doing the same thing, but with your deductible and your premium.

Different Strokes for Different Folks (and Claims)

Now, here's where it gets a bit nuanced. Not all claims are created equal. A minor leaky faucet that caused a bit of water damage is going to be viewed differently than a house fire that leveled your entire kitchen.

Let's say your kid, in a moment of pure, unadulterated joy (or perhaps boredom), accidentally kicks a soccer ball through your living room window. That's a relatively small, isolated incident. Your insurance company might look at that, say "Oopsie!" and perhaps make a small adjustment, or maybe even no adjustment at all, especially if you have a good claims history.

On the other hand, if you have a series of claims within a short period – say, a burst pipe one year, a windstorm damage the next, and then a theft – that's a different story. That starts to look like a pattern, and your insurance company might decide that the risk associated with insuring your home has increased significantly. In that scenario, a premium increase is much more likely, and in some rare cases, they might even choose not to renew your policy.

The Impact of "No-Fault" Claims

Here's a little nugget that might make you smile: some claims might not affect your rates at all. These are often referred to as "no-fault" claims. Think about situations where you couldn't have reasonably prevented the damage. For example, if a massive, unexpected storm dumps a foot of hail on your roof, and a significant portion of your neighborhood experiences similar damage, your insurance company might be more understanding. They recognize that this was an act of nature, beyond your control.

Similarly, if a tree falls onto your property due to a lightning strike, that's another instance where they might be less inclined to penalize you with higher premiums. It's like if your neighbor accidentally backed into your mailbox while trying to parallel park – it was an accident, and while you'll get it fixed, it doesn't mean your relationship is suddenly on the rocks.

What About Multiple Claims?

This is where things can get a little trickier. Insurance companies often look at the frequency and severity of claims. One small claim in five years? Probably not a big deal. Two moderate claims in three years? Your premium might see a slight nudge. Three or more claims, especially if they're for significant amounts, within a shorter timeframe? That's when you're more likely to see a noticeable increase.

It's like going to the doctor. If you have one minor cold, the doctor might say "get some rest." If you're in the office every other week with a different ailment, the doctor might start recommending more thorough check-ups and lifestyle changes. Your insurance company is doing a similar kind of risk assessment.

So, Should You Be Afraid to File a Claim?

Absolutely not! This is the most important takeaway. Homeowners insurance is there for a reason. It's to protect you from the financial devastation of unforeseen events. If something genuinely bad happens to your home, you should feel empowered to use your insurance.

Imagine your precious antique vase, a family heirloom passed down for generations, gets accidentally knocked over and broken. You have insurance for a reason! You shouldn't live in fear of filing a claim for something like that. The potential for a small premium increase is a small price to pay for the peace of mind and financial security that insurance provides.

However, it's wise to be informed. Before you file a claim, especially for a smaller, more manageable issue, consider the following:

- Your Deductible: Is the cost of the repair significantly more than your deductible? If the damage is only a few hundred dollars and your deductible is $1,000, it might not be worth filing a claim. You'd be paying out of pocket anyway, and you'd still potentially have a claim on your record.

- The Severity of the Damage: As we've discussed, a minor incident is less likely to cause a significant rate hike than a major one.

- Your Claims History: If you have a long history of being a responsible, claims-free homeowner, one minor incident might not move the needle much at all.

Think of it like this: you wouldn't hesitate to call roadside assistance if your car broke down in the middle of nowhere, right? Your homeowners insurance is your "roadside assistance" for your home. Don't let the fear of a potential small increase keep you from using it when you truly need it.

How to Navigate the System

If you do decide to file a claim, be proactive and communicate with your insurance company. Understand their policies regarding claim frequency and its impact on your premiums. They can often provide you with information about how past claims might affect your rates.

And if you do see an increase after a claim, don't just accept it blindly. Shop around! Get quotes from other insurance providers. Your loyalty is appreciated, but your wallet might be happier elsewhere. Sometimes, a competitor might offer you a better rate, even with a claim or two on your record. It's always worth exploring your options.

Ultimately, homeowners insurance is a tool to protect your biggest investment. While it's wise to be aware of how claims can affect your premiums, the most important thing is to use your insurance when you need it. A little proactive thinking and a willingness to shop around can go a long way in keeping your home safe and your budget happy. So, go ahead, fix that leaky roof, replace that broken window, and sleep soundly knowing you're covered. That's what it's all about!