Elizabeth Is The Beneficiary Of A Life Insurance: Complete Guide & Key Details

Hey there! Ever wondered what happens to all those life insurance policies people have? It can sound a bit… serious, right? Like something out of a legal drama. But what if I told you it’s actually pretty interesting, and sometimes even a little bit heartwarming? Today, we’re going to dive into the world of life insurance beneficiaries, with a special look at someone we're calling "Elizabeth." Think of this as your chill guide to understanding why being a beneficiary like Elizabeth can be a really big deal, and all the cool stuff that comes with it.

So, let’s imagine Elizabeth. Maybe she’s a sister, a best friend, or even a favorite aunt. Someone someone loved deeply enough to set up a life insurance policy for her. It's like a final, thoughtful gift, a way to say, "Hey, I cared about you, and I want to make sure you're okay, even when I'm not around." Pretty neat, huh?

Elizabeth: The Star of Our Insurance Story

In the grand scheme of life insurance, the beneficiary is the lucky duck, the one who gets the payout. And in our case, that's Elizabeth! It's not just about getting some money; it's about what that money represents. It's a tangible piece of someone's legacy, a way for their love and care to continue in a very practical way.

Think of it like this: when someone names Elizabeth as their beneficiary, they're essentially saying, "This part of my financial planning is for you, Elizabeth. This is a safety net, a helping hand, a way to ease any burdens you might face." It’s a gesture that goes way beyond words.

Why Being a Beneficiary Isn't Just About the Dough

Sure, the money part is a significant aspect, and we’ll get to that. But let's not forget the emotional weight behind it. For Elizabeth, receiving this payout is often tied to memories, to the person who chose her. It’s a reminder of their presence, even in their absence. It’s like receiving a special hug from the past.

It can help cover immediate expenses, of course. Things like funeral costs, which can be surprisingly high, or outstanding debts. But it can also be so much more. Imagine if Elizabeth was saving up for a down payment on a house, or wanted to go back to school. This payout could be the rocket fuel that makes those dreams a reality!

It’s like someone leaving you a treasure map, and the treasure is pretty darn useful. It's not just random luck; it's a carefully planned act of love and foresight.

The Key Details Elizabeth Needs to Know

Now, let's get down to the nitty-gritty. What does Elizabeth actually need to do and know when she’s the beneficiary? It’s not rocket science, but there are a few important steps to keep things smooth.

Step 1: The Official Notification

Typically, the insurance company will reach out to the beneficiary. They’ll need proof that the insured person has passed away, usually with a death certificate. It’s a somber process, no doubt, but it’s the first official step to unlocking that benefit.

Sometimes, the beneficiary might know they are listed and initiate the contact. Either way, the insurance company is there to guide them through the process. They have teams dedicated to helping people like Elizabeth navigate these sometimes confusing waters.

Step 2: Filling Out the Forms (Don't Panic!)

There will be some paperwork. Think of it like filling out an application for a really cool club, where the membership fee is zero and the perks are pretty sweet. These forms help the insurance company verify Elizabeth's identity and process the claim.

They might ask for identification, bank details for the payout, and other relevant information. The insurance company usually provides clear instructions, and if Elizabeth is unsure, she can always call them for help. They’re not trying to trick her; they just need to make sure they’re giving the money to the right person!

Step 3: The Payout – Cha-ching!

Once everything is processed and approved, Elizabeth gets the money! This can be done via a lump sum, which is often the most straightforward, or sometimes in installments, depending on the policy and what was agreed upon.

A lump sum is like getting a big, wonderful surprise all at once. It gives Elizabeth immediate control and flexibility. She can decide exactly how she wants to use it. Want to pay off your student loans with it? Go for it! Want to invest it and watch it grow? Smart move!

What Kind of Life Insurance Are We Talking About?

It's worth mentioning that there are different types of life insurance. The two main ones are term life insurance and permanent life insurance.

Term life insurance is like renting an apartment. You have coverage for a specific period (the "term"), and if the insured person passes away during that time, the beneficiary gets the payout. If the term ends and they're still around, the policy expires (unless it's renewed).

Permanent life insurance is more like owning a house. It lasts for the insured person's entire life, and it often builds up a cash value over time that can also be accessed. So, the payout is pretty much guaranteed eventually.

The type of policy will influence how and when the beneficiary benefits, but the core idea remains the same: a financial gift intended for someone else.

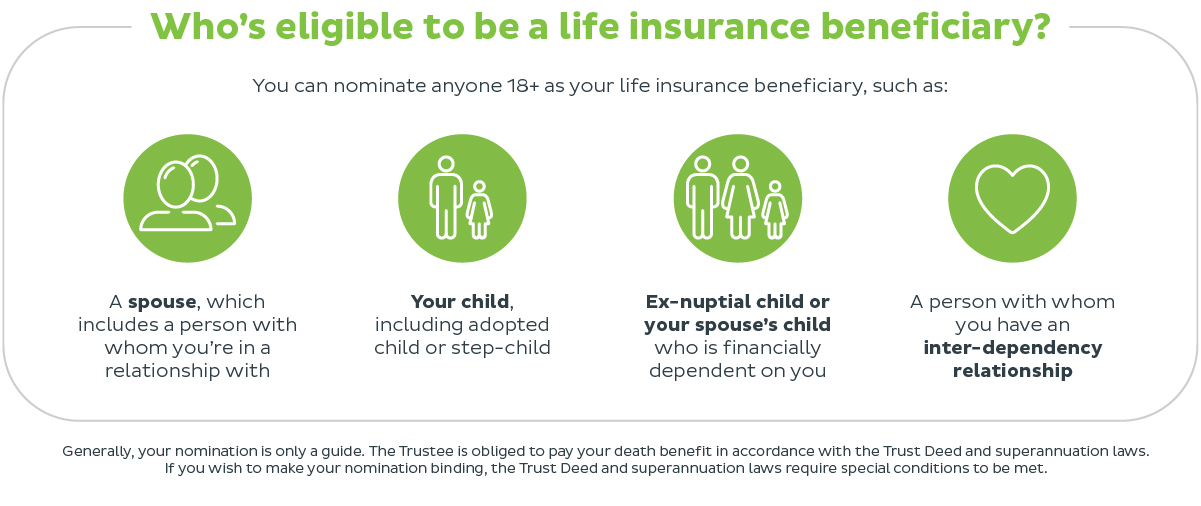

The "Primary" vs. "Contingent" Beneficiary Shuffle

Sometimes, there’s a bit of a backup plan involved. You might hear terms like "primary beneficiary" and "contingent beneficiary."

Elizabeth, if she’s the primary beneficiary, is the first in line to receive the payout. She’s the VIP. But what if, for some reason, Elizabeth isn't around or can't receive the benefit? That's where the contingent beneficiary comes in. They’re like the understudy, ready to step in if the main star isn't available.

It's all about making sure the money goes to where the insured person intended it to go, no matter what life throws at them.

Taxes and Life Insurance: A Quick Peek

This is a question many people have: "Do I have to pay taxes on life insurance money?" Generally speaking, life insurance death benefits are not taxed as income in the United States. Pretty sweet, right?

However, there can be exceptions, especially if the payout is part of a larger estate that exceeds certain tax thresholds. But for the vast majority of beneficiaries like Elizabeth, the payout comes tax-free. It’s another way the policy acts as a clear benefit, without unexpected deductions.

It’s always a good idea to consult with a tax professional if Elizabeth has any specific concerns, but the good news is, it’s usually a straightforward situation.

What If Elizabeth Doesn't Claim It?

This is a sad thought, but it happens. If a beneficiary doesn’t claim the life insurance payout within a certain timeframe, the money can go to the estate of the deceased, or to the contingent beneficiary if one was named. Insurance companies can't hold onto the money forever without action.

This is why it’s so important for beneficiaries to be aware and to act when they are notified. It’s a gift waiting to be received!

The Big Picture: A Gift of Security and Love

So, there you have it. Being a beneficiary like Elizabeth isn't just about a financial transaction; it's a testament to someone's love, planning, and desire to provide security. It's a way for their care to extend beyond their lifetime, offering comfort, support, and opportunities.

Whether it helps cover immediate needs, fund a dream, or simply provides peace of mind, the life insurance payout is a powerful tool. It’s a tangible expression of what mattered most to the person who took out the policy. And for Elizabeth, it’s a chance to honor their memory by using this gift wisely and making the most of it. It’s a beautiful, albeit bittersweet, part of life’s journey.