Expansionary Monetary Policy: What It Means For Borrowers And Savers

Hey there! Ever heard folks on the news or maybe your uncle at Thanksgiving talking about the "Fed" doing something, and suddenly your ears perk up because it might actually affect your wallet? Well, today we're gonna dive into something called expansionary monetary policy. Sounds a bit fancy, right? But honestly, it’s not as scary as it sounds. Think of it as the central bank, usually the Federal Reserve in the U.S., giving the economy a gentle nudge to get things moving a bit faster.

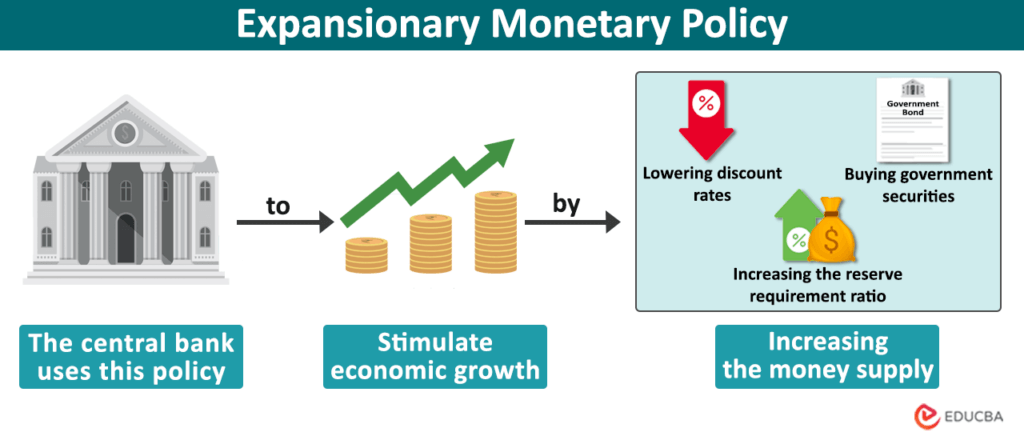

So, what exactly is this mysterious expansionary monetary policy? Imagine the economy is like a car that’s been chugging along, maybe a little too slowly, and the driver (that's the Fed!) wants to give it a bit more gas. They want to encourage people and businesses to spend more money, invest more, and generally get things buzzing. Why? Usually, it's when the economy is feeling a bit sluggish, maybe facing the threat of a recession, or when inflation is a little too low (which can also be a problem, believe it or not!).

How Do They "Give It More Gas"?

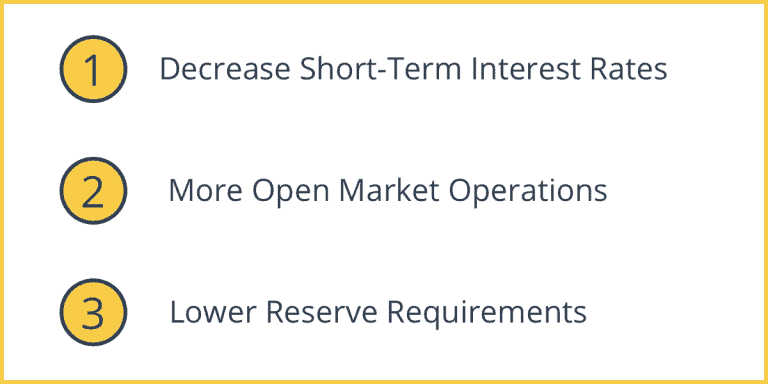

The Fed has a few main tools in its toolbox to achieve this. It's kind of like a chef deciding which spices to add to a dish to make it tastier. One of the most common ways is by lowering interest rates. You know those rates you see when you take out a loan or even when you look at savings accounts? The Fed can influence those.

Think about it like this: when interest rates are low, it's cheaper to borrow money. It's like finding a sale at your favorite store. Suddenly, that car you've been eyeing or that expansion for your small business doesn't seem so financially daunting anymore. So, people and companies are more likely to take out loans to buy things, build things, or invest in new projects. This, in turn, creates more demand for goods and services, which can lead to more jobs and a stronger economy.

Another trick the Fed might pull is called quantitative easing (QE). This one’s a bit more complex, but stick with me! Imagine the Fed buying up a bunch of government bonds or other financial assets from banks. What does this do? It injects more money into the banking system. It's like giving the banks a bigger pile of cash to lend out. More money available means it's easier for businesses and individuals to access loans, and again, encourages spending and investment. It’s all about making money flow more freely through the economy.

What Does This Mean for Borrowers?

Alright, let's get to the juicy part for those of us who might be thinking about borrowing money. If the Fed is implementing expansionary monetary policy, it's generally good news for borrowers! Why? Because, as we mentioned, interest rates tend to go down.

So, if you're dreaming of buying a house, now might be a fantastic time. Your mortgage payments will likely be lower because the interest rate is less. Think of it as getting a discount on the biggest purchase of your life! It’s like finding out your dream vacation just went on a huge sale – exciting, right?

What about that car you want to upgrade? Or maybe you're a small business owner looking to expand your operations, buy new equipment, or hire more staff? Lower interest rates make those loans much more affordable. This can free up your cash for other things, like investing in more inventory, marketing, or even just giving your employees a well-deserved raise. It’s like getting a financial boost to help your dreams become a reality.

Even for credit cards, you might see those interest rates dip a bit, making it less costly to carry a balance. Of course, it's always wise to pay off your credit card debt as quickly as possible, but a lower rate certainly doesn't hurt!

And What About Savers? The Flip Side of the Coin

Now, here's where things get a little less exciting for the savers out there. While it's a great time to borrow, it's often not so great for saving. When interest rates are low, the returns you get on your savings accounts, certificates of deposit (CDs), and even some bonds tend to be pretty meager.

Imagine you've been diligently putting money aside in a savings account, hoping to see it grow. With low interest rates, that growth is going to be slow. It's like planting a seed and expecting it to sprout overnight – it just doesn’t happen that way. Your money is still safe, but it’s not working as hard for you.

This can be a bit frustrating if you're relying on your savings for income, like retirees often do. Or perhaps you're saving up for a big down payment on a house, and you're hoping that interest will contribute a little something extra. In an expansionary environment, that "little something extra" might be very little indeed.

Some savvy savers might look for alternative places to put their money where they can potentially earn a higher return. This could involve investing in the stock market, which can be more volatile but also offers the potential for higher gains. However, it’s crucial to remember that with higher potential returns often comes higher risk. It’s a classic trade-off: safety versus growth.

The Bigger Picture: Why Does the Fed Do This?

So, why would the Fed intentionally make things less rewarding for savers? It's all about balancing the economy. Their main goals are usually to keep inflation stable and to promote maximum employment. If the economy is too slow, unemployment can rise, and that’s bad for everyone.

By making borrowing cheaper, the Fed hopes to stimulate spending and investment, which creates jobs and gets businesses producing more. It’s a bit like giving the economy a shot of adrenaline to wake it up. The hope is that this increased economic activity will eventually lead to a stronger, healthier economy for all.

It’s important to remember that these policies aren't always perfect. Sometimes, the economy might overheat, leading to too much inflation. Other times, the stimulus might not be enough. It’s a constant juggling act for the central bank.

Ultimately, understanding expansionary monetary policy helps you see how the big economic decisions made by institutions like the Fed can ripple down and affect your own financial life. Whether you're looking to borrow for a big purchase or trying to grow your savings, knowing the general direction the economy is heading can help you make more informed decisions. Pretty neat, huh?