Fidelity Money Market Spaxx

Ever feel like your hard-earned cash is just lounging around, doing absolutely nothing? Like it's chilling on a beach somewhere, sipping tiny umbrella drinks, while you're out there wrestling with bills and trying to remember where you parked? Yeah, me too. That’s where a little something called a money market fund, specifically Fidelity's SPAXX, can come in handy. Think of it as giving your idle money a comfortable, low-key job.

Now, before you start picturing spreadsheets and guys in suits with stern faces, let’s break it down. A money market fund isn't some complex Wall Street wizardry. It's more like a really well-organized piggy bank for your spare change, only instead of quarters and dimes, it's holding slightly more sophisticated IOUs. And SPAXX? That’s just Fidelity’s particular flavor of this money-holding magic.

Imagine you’ve just gotten a bonus, or maybe you sold that antique lamp you’ve been meaning to get rid of for ages. Suddenly, you have a chunk of cash that’s not earmarked for anything specific. It’s not going into your checking account, because hello, overdraft fees. It’s not going into your investment portfolio, because you’re not quite ready to dive into the thrilling, and sometimes terrifying, world of stocks and bonds. It’s just… there. Like that one perfectly good spatula you never use.

So, what do you do with this sudden windfall of cash? You could stuff it under your mattress, which, while traditional, is a bit like giving your money a permanent nap. Or, you could put it into something like SPAXX. It’s like giving your money a comfy, albeit somewhat boring, hotel room to stay in while it waits for its next adventure.

Here’s the deal: SPAXX invests in very, very safe, short-term debt. Think of it as lending your money to the government or big, reputable companies for a tiny, short period. They promise to pay you back with a little bit of interest. It's not going to make you a millionaire overnight, and it's definitely not going to send you on a spontaneous trip to the Maldives (unless you already were a millionaire). But it’s a heck of a lot better than your money just sitting there, gathering dust and doing nothing.

The "Safe" Part: Why It's Not Your Typical Investment Gamble

Let’s talk about "safe." In the world of money, "safe" often means "not very exciting." Think of it like choosing vanilla ice cream over a seven-layer death-by-chocolate cake. It’s reliable, it’s predictable, and you know exactly what you’re getting. SPAXX is the vanilla ice cream of the money world. It aims to preserve your principal – meaning, the money you put in is pretty much guaranteed to still be there. This is a big deal. It’s like sending your kid to kindergarten; you expect them to come home in one piece, not having joined a circus troupe.

Contrast this with, say, buying a meme stock because your cousin Barry told you it was "going to the moon." Barry might be a great guy, but his financial advice is usually as solid as a Jell-O mold in a hurricane. Money market funds like SPAXX are the opposite. They're designed for stability. They're the sensible shoes in your financial closet.

The interest rates on money market funds can fluctuate. Sometimes they're a little higher, sometimes a little lower. It’s like the weather – sometimes it’s sunny and warm, and sometimes you need a jacket. But generally, it’s aiming for a steady, modest return. It’s not going to send your bank account into a frenzy of excitement, but it’s also not going to give you those heart palpitations you get when you check your stock portfolio after a particularly volatile trading day.

Think of it this way: you’ve got a bunch of LEGO bricks. You can build a super-duper, intricate spaceship that might crash and burn spectacularly, or you can build a sturdy little house that’s always there for you. SPAXX is your LEGO house. It’s not going to win any architectural awards, but it’s a solid, reliable place for your money to hang out.

The "Yield" Part: Getting a Little Something Back

So, if it's so safe, what's in it for you? Ah, the yield! This is the little bonus, the tiny reward for letting your money do its low-key job. SPAXX earns a bit of interest. It’s like finding a few forgotten dollar bills in your winter coat pocket. It’s not enough to retire on, but it’s a pleasant surprise.

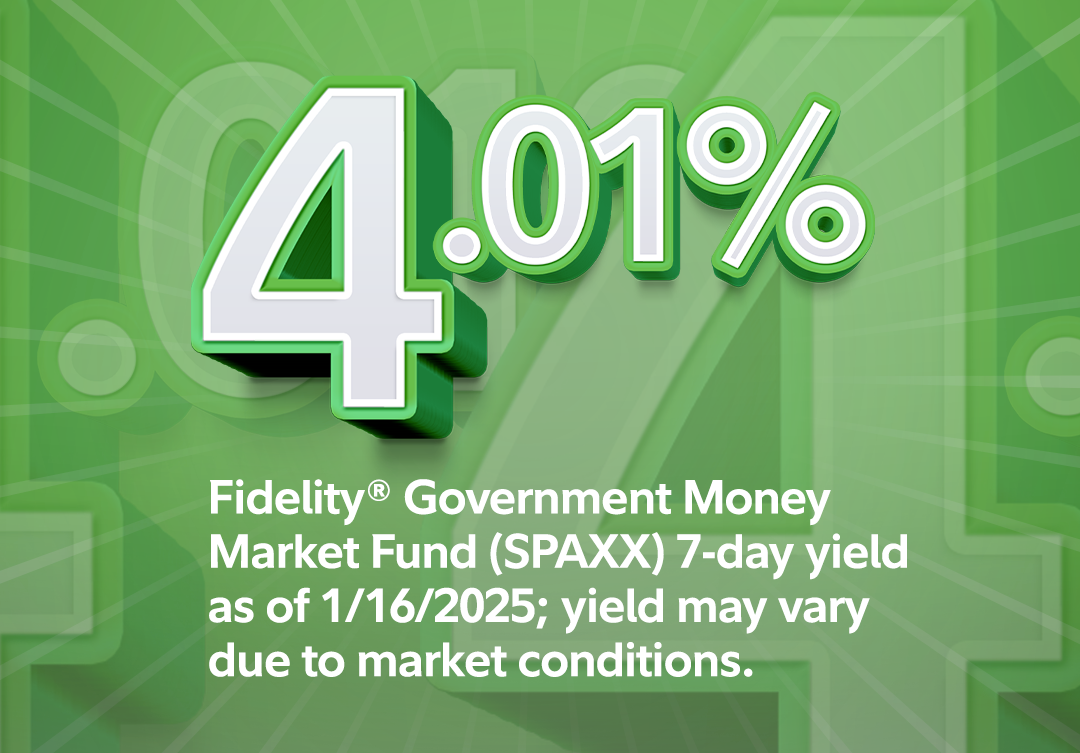

The current yield on SPAXX can be found on Fidelity’s website, and it's usually updated regularly. It’s like checking the daily specials at your favorite diner. Sometimes the soup of the day is a bit more appealing, sometimes it’s just… soup. But at least there is a special!

When interest rates are higher overall, the yield on SPAXX tends to go up. This is when your money market fund starts to feel a little less like vanilla and a bit more like a salted caramel swirl. Conversely, when interest rates are low, the yield might be a bit more… well, vanilla. It's all part of the natural ebb and flow, like the tide coming in and out.

This earned interest is usually reinvested, meaning it gets added back into your fund. So, your money is not only safe, but it’s also slowly, gently, growing. It’s like watering a small plant; it might not look like much day-to-day, but over time, it can blossom. Without the risk of it suddenly sprouting wings and flying away.

SPAXX vs. Your Checking Account: The Ultimate Showdown

Let’s be honest, most of us have a checking account. It’s where our paychecks land, and where our bills get whisked away to. It’s the workhorse of our daily finances. But here’s the dirty little secret about checking accounts: they usually earn next to nothing in interest. Zilch. Nada. It’s like having a super-fast sports car but only ever driving it in first gear. You have the potential, but you're not really using it.

SPAXX, on the other hand, offers a yield. Even a modest yield is more than the often-zero interest from a checking account. Think of your checking account as a bustling marketplace – money is constantly coming in and going out. It’s chaotic but necessary for daily life. SPAXX is more like a quiet, well-guarded vault where you store cash you don’t need to access immediately. It’s less exciting, but it’s safer and earns you a little something.

So, what’s the difference in practical terms? Imagine you have $10,000 sitting in your checking account for a year. You’ll likely earn… well, let’s just say you won’t be buying a yacht. Now, imagine that same $10,000 in SPAXX. Depending on the yield, you could earn a couple of hundred dollars, maybe more. That’s not life-changing money, but it’s certainly better than nothing. It’s like getting a free coffee every now and then, just because your money decided to be productive.

The key difference is accessibility. You can whip out your debit card and spend money from your checking account in seconds. SPAXX, while liquid and generally easy to access (especially through Fidelity's online platform), might have a slight delay. It’s not like you can use your SPAXX to buy a latte on the fly. It's more for money you're planning to use in the near future, but not this very second.

Think of it like this: your checking account is your wallet, full of cash for everyday purchases. SPAXX is like a well-stocked pantry. You know the food is there, you can get to it when you need to cook a meal, but you’re not going to grab a can of beans to munch on while you’re out and about.

Who is SPAXX For? The "Just-in-Case" Crowd and Beyond

So, who is this SPAXX character best suited for? Well, if you're someone who likes to have a bit of a safety net, a little cushion for unexpected expenses, then SPAXX could be your jam. It's for the "just-in-case" crowd. The folks who like to have a "rainy day fund" that’s actually earning something when it’s not raining. It’s like having an umbrella that’s not just a prop, but an actual, functional umbrella.

It's also great for people who are saving up for a specific, relatively short-term goal. Maybe you're planning a big vacation in six months, or you're saving for a down payment on a car. You don't want to tie that money up in something too risky, but you also don't want it to just sit there doing nothing. SPAXX is like a holding pen for your goal money, keeping it safe and sound while you get ready for the big event.

Fidelity also offers SPAXX within their retirement accounts. This is a bit different. In a retirement account, like an IRA, your money is locked away for a longer period. So, using SPAXX within that context means you’re essentially putting your retirement savings into a very conservative, low-yield investment. This is a strategic choice for some, especially those closer to retirement who want to reduce risk. It's like deciding to switch from a high-octane race car to a comfortable, reliable sedan when you know you're almost at your destination.

If you’re an active investor who’s constantly trading stocks and bonds, SPAXX can also be a great place to temporarily park your cash between trades. It's like a pit stop for your investment money, allowing you to quickly move it back into the market when an opportunity arises, without losing out on a little bit of interest in the meantime. It’s the financial equivalent of having a comfy waiting room.

The Bottom Line: A Simple Choice for Your Spare Cash

At the end of the day, Fidelity’s SPAXX is a straightforward, no-frills way to earn a little bit of interest on your cash while keeping it safe and accessible. It’s not going to revolutionize your financial life, and it’s certainly not a get-rich-quick scheme. But it is a sensible option for money that you don't need to access immediately.

Think of it as giving your spare cash a pleasant, low-risk retirement from its usual checking account hustle. It gets to relax, earn a tiny bit of passive income, and be there for you when you need it. It’s like having a responsible, slightly boring friend who always has your back and occasionally buys you a coffee.

So, if you've got some extra dough sitting around, not doing much, and you're looking for a simple, reliable place to put it, SPAXX is definitely worth considering. It's the financial equivalent of putting on your comfortable slippers after a long day – it just makes sense.