Health Insurance That Cover Pre Existing Conditions

So, I was chatting with my friend Sarah the other day, and she was telling me about her dad. He’s got this chronic condition, a really manageable one, but it means he needs regular check-ups and a few specific medications. For years, he’d been trying to find new health insurance, and let me tell you, it was like navigating a minefield. Every application, every phone call, it always came back to that same old phrase: "pre-existing condition."

She was so frustrated, and honestly, I don't blame her. It felt like he was being penalized for something he had no control over. He wasn’t trying to pull a fast one; he just needed consistent care. It got me thinking, how many people are in Sarah’s dad’s shoes? How many of us know someone who’s faced this wall when all they want is peace of mind and decent healthcare?

It turns out, it’s a pretty big deal. The whole idea of health insurance is to protect you when things go wrong, right? But for a long time, if you had something going on before you even signed up, insurers could just say, "Nope, can't cover that." And that, my friends, is where the seemingly simple concept of health insurance that covers pre-existing conditions becomes absolutely crucial. It’s not just a nice-to-have; for many, it's a lifeline.

The "Pre-Existing" Predicament: A Blast from the Past (Not a Good One!)

Let’s rewind a bit, shall we? Back in the not-so-golden days of health insurance, before some pretty significant legislative changes, the landscape for people with pre-existing conditions was, to put it mildly, grim. Imagine this: you’ve got asthma, diabetes, heart disease, or maybe you just had a baby and are dealing with postpartum complications. You’re trying to get health insurance, and bam! The insurer slams the door shut, or they’ll offer you a plan but with a massive surcharge, or they’ll exclude coverage for everything related to your condition.

It was a Catch-22 situation. You needed insurance because of your condition, but you couldn't get it because of your condition. Kind of makes you want to… well, you know. Sigh dramatically. It was enough to make people delay or even forgo necessary medical care, which, of course, only made their conditions worse and ultimately cost the healthcare system more in the long run. Brilliant, right?

This wasn't just about rare, complex diseases. This affected millions of people with common, manageable conditions. Think about someone who had a bout of cancer a few years ago but is now in remission. They might still be deemed "high risk" and face prohibitive costs or outright denial. It felt inherently unfair, like being punished for being sick.

Enter the Game Changers: What Changed (and Why It Matters)

Okay, so thankfully, things have shifted. The big one, especially in the United States, was the passage of the Affordable Care Act (ACA). This was a monumental piece of legislation that, among many other things, fundamentally changed how pre-existing conditions are treated in the health insurance market. It basically said, "No more!"

Under the ACA, health insurance companies are generally prohibited from denying you coverage, charging you more, or excluding benefits based on a pre-existing condition. This is HUGE. It means that if you have a chronic illness, a past injury, a mental health condition, or any other health issue that was diagnosed before you applied for insurance, you can’t be discriminated against because of it.

So, what does this actually look like in practice? Well, it means you can shop for health insurance plans knowing that your existing health needs will be considered. You can choose a plan that offers the best network of doctors and specialists for your condition, the most convenient prescription drug coverage, and the right level of benefits, all without the looming fear of being rejected or facing astronomical bills for your ongoing care.

This isn't just about a specific law; it's about a fundamental shift in how we approach healthcare and access. It's about recognizing that everyone deserves a chance to be healthy and to manage their health conditions without being shut out of the system.

So, How Does It Actually Work? Decoding the Jargon

Let's break down what "health insurance that covers pre-existing conditions" really means, especially now with these protections in place.

Understanding "Pre-Existing Condition"

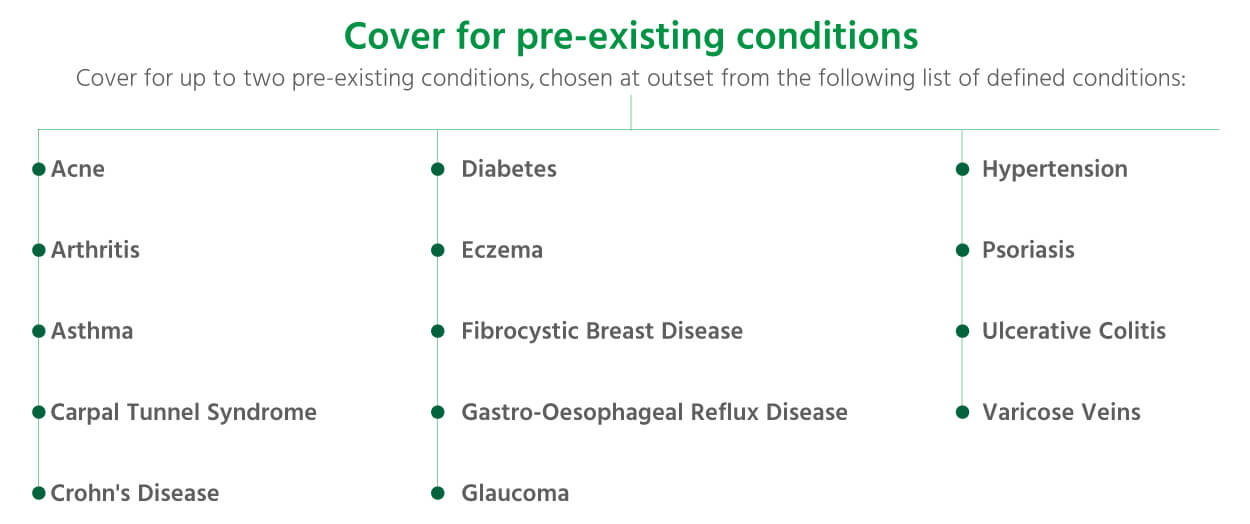

First off, what is a pre-existing condition? In simple terms, it's any medical condition that you had before the date your new health insurance coverage became effective. This can include:

- Chronic illnesses like diabetes, asthma, arthritis, heart disease, COPD.

- Mental health conditions like depression, anxiety disorders, bipolar disorder.

- Past injuries or surgeries that might require ongoing care or monitoring.

- Pregnancy at the time of enrollment (yes, even pregnancy was often a pre-existing condition!).

- Conditions that have been diagnosed but are not currently symptomatic but could flare up.

Basically, if you've been diagnosed or treated for something before you get your insurance, it counts. And again, the good news is, thanks to regulations like the ACA, insurers can't use that against you when selling you a plan in most markets.

What "Coverage" Entails

When we talk about coverage for pre-existing conditions, it means the insurance plan will cover services and treatments related to that condition. This isn't a magic wand that makes your condition disappear, but it means:

- Doctor Visits: Your regular appointments with specialists or primary care physicians related to your condition will be covered, subject to your plan's copays and deductibles.

- Medications: Prescriptions needed to manage your condition should be covered according to your plan's formulary (the list of covered drugs) and copay structure.

- Hospital Stays: If you need to be hospitalized due to your condition, those costs will be covered as per your plan benefits.

- Therapies and Procedures: Physical therapy, mental health counseling, surgeries, or other medical procedures necessary for your condition will be part of your covered benefits.

It's crucial to remember that "coverage" still means you'll be responsible for your share of the costs, like deductibles, copayments, and coinsurance, as outlined in your specific plan. The insurer isn't footing the entire bill, but they are sharing the risk and making the costs manageable.

Navigating the Marketplace: Tips for Finding the Right Plan

Okay, so you know that coverage for pre-existing conditions is pretty much a given (in many places, at least!), but how do you pick the right plan? It’s not just about ticking a box; it's about finding the best fit for your health needs and your budget. Think of it like choosing a doctor – you want someone who really gets you and your situation.

1. Know Your Needs (And Be Honest!)

This sounds obvious, but seriously, take stock. What conditions do you have? What medications do you take regularly? What specialists do you see? The more you understand your own healthcare needs, the better you can compare plans. Don't be shy about it; this is for your health!

2. Explore Your Options

Where can you find these plans? In the US, the Health Insurance Marketplace (Healthcare.gov) is a primary place to look. You can compare plans side-by-side, see the costs, and understand the benefits. If you have an employer, your HR department can tell you about the company's group health insurance options.

There are also private insurance brokers who can help you navigate the market, though be sure they are reputable. And sometimes, state-specific marketplaces offer additional plans or subsidies.

3. Compare Plan Details (Beyond Just the Premium)

The monthly premium is the most visible cost, but it's rarely the whole story. Look at:

- Deductible: The amount you pay out-of-pocket before your insurance starts paying for most services. A lower premium often means a higher deductible, and vice-versa.

- Copayments (Copays): A fixed amount you pay for a covered healthcare service after you’ve met your deductible (or sometimes, even before, for certain services like doctor visits).

- Coinsurance: Your share of the costs of a covered healthcare service, calculated as a percentage (e.g., 20%) of the allowed amount for the service.

- Out-of-Pocket Maximum: The most you’ll have to pay for covered services in a plan year. Once you reach this limit, your health plan pays 100% of the allowed amount for covered benefits. This is your ultimate safety net!

- Network: Does your preferred doctor or hospital network? This is super important. If your current doctor isn't in the network, you might have to pay more or find a new one.

- Formulary: What medications are covered, and at what tier (which affects your copay/coinsurance)? Check if your regular prescriptions are on the list.

Think about which costs you're most comfortable with. Are you willing to pay a bit more each month for lower copays when you visit the doctor? Or do you prefer a lower monthly payment and are okay with a higher deductible if you don't anticipate needing a lot of care?

4. Read the Fine Print (Seriously, Read It!)

Okay, I know, nobody loves reading insurance documents. They’re dense, full of jargon, and can make your eyes glaze over. But this is where the crucial details live! Pay attention to what's excluded (though exclusions for pre-existing conditions are now very limited in many markets), the rules for referrals, and any limitations on coverage.

5. Ask Questions!

Don't be afraid to call the insurance company or a broker and ask for clarification. If something isn't clear, or if you're worried about a specific aspect of your care being covered, ask. It’s better to get an answer upfront than to be surprised later.

The Broader Impact: Why This Matters to All of Us

The fact that health insurance now widely covers pre-existing conditions isn't just a win for individuals with those conditions; it's a win for society as a whole. When people can access healthcare without fear of being denied, they are more likely to:

- Stay healthy: Early detection and consistent management of chronic conditions prevent more serious, costly problems down the line.

- Be productive: People who are healthy can work, contribute to the economy, and participate fully in their communities.

- Reduce the burden on emergency care: When people have consistent access to primary and preventive care, they are less likely to rely on expensive emergency rooms for routine or manageable issues.

- Have peace of mind: Knowing that you and your loved ones are covered, no matter what life throws at you health-wise, is invaluable.

It creates a more stable and equitable healthcare system, one that’s designed to support everyone, not just the perfectly healthy. It’s a reflection of a society that values the well-being of all its members.

So, while Sarah’s dad’s situation was a personal frustration, it’s a powerful reminder of how far we've come, and why continuing to ensure robust coverage for pre-existing conditions is so incredibly important. It’s about making sure that a health diagnosis doesn't become a financial disaster or a barrier to living a full and healthy life. And that, my friends, is something worth celebrating and protecting.