How Can I Avoid Capital Gains Tax: Everything You Need To Know Right Now

Hey there, savvy savers and aspiring investors! Ever find yourself staring at a lovely chunk of profit from selling, say, a stock, a piece of art you finally parted ways with, or maybe even that quirky little cottage you inherited? Awesome! You’ve done the investing thing, and it’s paid off. But then, a little voice in the back of your mind whispers… “Taxes.” Dun dun DUN! Don't let that thought dim your sunshine, though. Because today, we're diving into the wonderfully (yes, I said wonderfully!) world of capital gains tax and how you can keep more of your hard-earned cash. Think of it as a treasure hunt for your financial future, and the treasure is… more money in your pocket!

Now, I know what you might be thinking. "Taxes? Fun? Are you kidding me?" Hear me out! Understanding taxes isn't about being a number-crunching robot. It's about being smart. It's about making your money work for you, not just disappear into the ether. And when you feel in control of your finances, that's seriously empowering. It's like leveling up in your own personal game of life. So, let's ditch the dread and get ready to get enlightened. Ready to become a capital gains ninja?

So, What Exactly Is Capital Gains Tax?

Alright, let's break it down, super simple. When you sell an asset – and by asset, we mean anything from stocks and bonds to real estate, collectibles, or even your prized comic book collection – for more than you originally paid for it, that profit is called a capital gain. And guess what? The government usually wants a slice of that pie. That slice is the capital gains tax. Simple as that! It's not a punishment, it's just how the system works. But like anything in life, there are ways to play the game strategically.

Think of it like this: you buy a cool vintage t-shirt for $20. You polish it up, maybe add a snazzy frame, and then sell it for $100. That $80 profit? That's your capital gain. The taxman might ask for a little bit of that $80. Now, multiply that by a few more items, and suddenly, understanding capital gains becomes a pretty big deal, right?

Short-Term vs. Long-Term Gains: The Crucial Difference!

This is where things get really interesting and where you can start making some smart moves. The government divides capital gains into two main categories: short-term and long-term. And the tax rates are wildly different. This is your first big clue, your flashing neon sign pointing to tax-saving opportunities!

Short-term capital gains are profits from assets you've owned for one year or less. The kicker? These are taxed at your ordinary income tax rate. Ouch. That could mean a pretty hefty chunk being taken out. So, if you're looking to flip assets quickly, just know the tax implications are usually higher.

/images/2024/10/07/capital_gains_tax_posit-it_1.png)

But here's the golden ticket: Long-term capital gains! These are profits from assets you've held for more than one year. And the magic? They are taxed at much lower rates. We're talking 0%, 15%, or 20%, depending on your overall taxable income. See? Patience is a virtue, especially when it comes to your money. Holding onto those assets for that extra month or two can save you a bundle. It’s like waiting for the perfect moment to strike – a strategy that’s rewarded!

Strategies to Help You Dodge (or at Least Minimize!) Capital Gains Tax

Okay, now for the fun part. How do we actively work towards reducing that tax bill? It’s not about illegal loopholes, folks. It’s about smart, legal financial planning. Think of these as your secret weapons in the fight for your financial freedom.

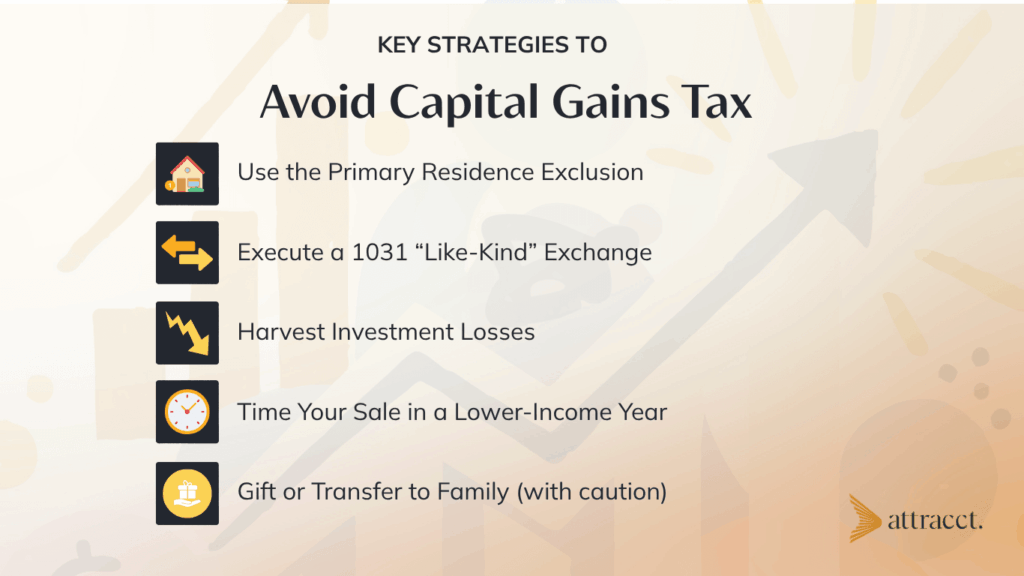

1. The Power of Holding On (Long-Term Capital Gains!)

I know, I know, I just said it. But it’s that important. If you have the luxury of time, holding onto appreciated assets for over a year is your absolute best friend when it comes to minimizing capital gains tax. This is the low-hanging fruit of tax savings. So, the next time you’re tempted to cash in a quick profit, do a quick calculation: "Is it worth waiting a little longer for a significantly lower tax rate?" Often, the answer is a resounding YES!

2. Tax-Loss Harvesting: Turning Lemons into… Well, Less Tax!

This is a clever tactic that can feel like a financial superpower. Tax-loss harvesting involves selling investments that have lost value to offset capital gains. Here’s the scoop: you can use those losses to cancel out your capital gains, dollar for dollar. And if your losses are more than your gains, you can even deduct up to $3,000 of those excess losses against your ordinary income each year! Anything beyond that can be carried forward to future years. It’s like a financial magic trick where losses become your allies!

Imagine you have a stock that’s taken a dip, but you also have another that’s soared. You can sell the losing stock to offset the gain on the winning stock, effectively reducing your taxable profit. Pretty neat, right? It requires a little bit of juggling, but the rewards can be substantial. Just be mindful of the wash-sale rule – you can't buy back the same or a substantially identical security within 30 days of selling it at a loss. So, plan your moves carefully!

3. Gift It Away! (Strategically, of Course)

This is where things can get really interesting, especially if you're thinking about passing on wealth or helping out loved ones. You can gift appreciated assets to others. When you gift an asset, you don't realize a capital gain at that moment. The recipient then takes on your original cost basis. This can be particularly advantageous if the recipient is in a lower tax bracket. So, gifting a stock that has appreciated significantly could save both you and the recipient a good chunk of tax down the line. It's like spreading the financial sunshine!

There are annual gift tax exclusion limits, so it's worth understanding those nuances. But the principle is sound: strategic gifting can be a beautiful way to manage capital gains.

![10 Tips on How to Avoid Capital Gains Tax on property [2025]](https://www.legendfinancial.co.uk/wp-content/uploads/2024/03/Capital-Gain-Tax-Calculator.jpg)

4. The Magic of Retirement Accounts

This is a big one, and it’s a no-brainer for most people. Investing within tax-advantaged retirement accounts, like a 401(k) or an IRA, is a fantastic way to defer or even eliminate capital gains taxes. When you sell an asset within these accounts, you don't owe capital gains tax on the profits at that time. If it's a Roth IRA, those qualified withdrawals in retirement are tax-free! For a traditional IRA or 401(k), you defer the taxes until you withdraw the money in retirement, and by then, your income tax rate might be lower. It's like putting your investments in a special tax-free vault!

So, if you're not already maxing out your retirement contributions, this is a huge incentive to start. It’s not just about saving for your golden years; it’s about making your money grow without the immediate tax bite.

5. Real Estate Moves: The Primary Residence Perk

If you own a home, this is a biggie. When you sell your primary residence, you can often exclude a significant amount of the profit from capital gains tax. For individuals, this exclusion is up to $250,000, and for married couples filing jointly, it's up to $500,000. To qualify, you generally need to have owned and lived in the home for at least two of the five years before the sale. This is a massive benefit designed to encourage homeownership and stability. So, that cozy little house you’ve made your sanctuary? It comes with a pretty sweet tax perk!

There are also other considerations for real estate, like 1031 exchanges, which allow you to defer capital gains tax on the sale of investment properties if you reinvest the proceeds into a like-kind property. This is a more complex strategy, but it’s a powerful tool for real estate investors.

6. Charitable Contributions: Do Good and Feel Good (and Save on Taxes!)

Believe it or not, giving back to your favorite causes can also have tax benefits. If you donate appreciated stock directly to a qualified charity, you can typically deduct the fair market value of the stock (as long as you’ve held it for more than a year) and avoid paying capital gains tax on that appreciation. It's a win-win-win: you support a cause you believe in, you get a tax deduction, and you avoid paying capital gains tax. It’s a beautiful synergy of generosity and smart financial planning.

Don't Be Scared, Be Prepared!

Look, nobody wakes up in the morning excited about tax forms. But understanding capital gains tax isn’t about drudgery; it’s about empowerment. It’s about knowing how your money works and how you can optimize it. It’s about making informed decisions that can lead to a more secure and prosperous future. When you feel in control of your finances, it’s incredibly liberating. It opens up more possibilities for travel, for investments, for pursuing your passions!

This is just the tip of the iceberg, of course. Tax laws can be intricate, and your personal situation is unique. But the key takeaway is this: with a little knowledge and some strategic planning, you can significantly reduce your capital gains tax liability. It’s about being a proactive participant in your financial journey, not just a passive observer. So, don't let the fear of taxes hold you back from celebrating your investment wins. Embrace the knowledge, explore the possibilities, and get ready to watch your wealth grow!

Now, go forth and get informed! Dive deeper into these strategies, talk to a trusted financial advisor, and start making your money work even smarter for you. Your future self will thank you!