How Long Does A Default Stay On Your Credit Report

Hey there, friend! Grab your coffee, settle in. We’re gonna chat about something that makes most people’s eyes glaze over, but honestly, it’s kinda important. You know, that thing called your credit report? And specifically, that dreaded word: default. Oof. Just saying it feels… heavy, right?

So, you’re probably wondering, “How long does this… thing… stick around?” Like, is it a boomerang? Does it just keep coming back to haunt you forever and ever? And what even is a default, really? Let’s break it down, no jargon, just real talk.

Basically, a default happens when you seriously drop the ball on a payment. Like, you miss it by a mile, and then some. It's not just being a day late, though that’s not ideal either, mind you. A default is usually when you’re way behind. We’re talking 30, 60, 90 days or more. It’s a big ol’ red flag waving in the face of whoever lent you money. Uh oh.

And guess what? The credit bureaus, those watchful eyes of the financial world, they love to keep records. It’s like they have an elephant’s memory for this stuff. So, when you default on something – a credit card, a loan, maybe even your rent if it’s reported – it’s gonna show up. And not just for a hot minute, either. Nope.

The Big Question: How Long Does It Linger?

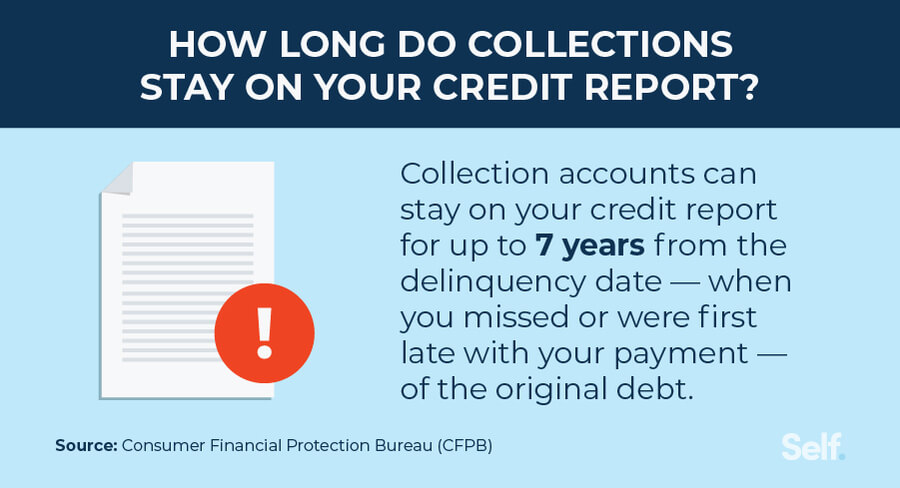

Alright, here’s the million-dollar question, or at least the “how-much-will-my-interest-rate-go-up” question. How long does a default really stay on your credit report? The standard answer, the one you’ll hear from most experts, is seven years.

Seven years! That sounds like a lifetime when you’re thinking about it, right? It's like that one embarrassing photo from your awkward teen years that keeps popping up in your social media memories. But here’s the kicker: it’s actually seven years from the date of the delinquency. Not from when you paid it off, not from when you finally got your act together, but from when you first missed that crucial payment.

Think of it like this: you stub your toe. It hurts like crazy for a bit, right? But then, it starts to heal. A default is kind of like that, but the bruise sticks around for a while longer. And it’s a big bruise on your financial health.

Different Types of Defaults, Different Timelines?

Now, you might be thinking, “Is it the same for everything?” Good question! While the general rule is seven years, there are a couple of nuances, like sprinkles on your financial sundae.

For most common things like credit cards and personal loans, it’s that classic seven-year timeframe. You know, the stuff that helps you buy a car or a couch on credit. But what about bigger, scarier things?

Consider a foreclosure. That’s a pretty serious default, isn’t it? When you can’t pay your mortgage and the bank takes your house. That one? It can stick around for a whopping seven years from the date of the original delinquency, just like the others. But the impact? Oh, that’s way bigger. It’s like a default is a papercut, and a foreclosure is… well, a pretty deep gash.

What about bankruptcies? Now, that’s a whole different ballgame. A Chapter 7 bankruptcy, the kind where you get a fresh start, can stay on your report for 10 years. Yep, a whole decade. And a Chapter 13 bankruptcy? That one usually stays for seven years, or until the payment plan is completed, whichever is longer. So, it can be a longer haul for those.

It’s like some financial mistakes are just… more permanent souvenirs than others. You know? Like that time you decided to dye your hair bright blue in high school. Some things just leave a more vivid impression. And unfortunately, a default is one of those things.

What Does A Default Actually Do?

So, why are we even obsessing over this seven-year mark? Because, my friend, a default is like a financial villain in your credit report’s story. It’s going to mess with your credit score. Like, seriously mess with it.

Your credit score is basically your financial report card. It tells lenders how likely you are to pay them back. And a default? It screams, “I’m a risk!” So, your score plummets. Down, down, down it goes.

This means getting approved for things becomes a whole lot harder. Want a new apartment? Forget it, unless you have a co-signer with a saintly credit score. Need a car loan? Prepare for sky-high interest rates, if you get approved at all. Even getting a new phone plan can be a challenge. It’s like trying to get VIP access with a ticket that’s been… well, defaced.

And the interest rates! Oh, the interest rates. Lenders see that default and think, “Okay, this person might not pay us back on time, so we need to charge them a lot more money to make it worth our while.” It’s like they’re charging you extra for the privilege of borrowing. Fun, right?

It’s not just about the big stuff, either. Sometimes, even smaller things can feel more expensive. Think of it as a little tax on your financial life, just because of that past mistake.

Does It Go Away On Its Own?

So, the big question is, does it just… vanish after seven years? Like magic? Well, yes and no. After that seven-year mark, the default itself should be removed from your credit report by the credit bureaus. Poof! Gone.

But here’s where the nuance comes in. While the reporting of the default stops, the consequences can linger. If you’ve had to deal with collections agencies because of that default, those collection accounts can also stay on your report for seven years from the date of the original delinquency. So, even if the original debt is considered old news, the collection activity can still be visible.

And let’s be real, the damage to your credit score from a default isn’t instantly erased the moment it falls off your report. It takes time and consistent good financial behavior to rebuild that score. It’s like a scar – the wound heals, but the mark might remain for a while.

So, while the official reporting period is a key number, it’s not always an instant “all clear” signal for your credit score. You’ve gotta put in the work to make things better. It’s like finally cleaning out your garage after years of neglect. It’s a process, not a single event.

What Can You Do About It?

Okay, so we know the bad news. It sticks around for a while. But here’s the good news, my friend: you’re not powerless! There are things you can do.

First things first, check your credit report regularly. Like, at least once a year. You can get free copies from AnnualCreditReport.com. It’s like a financial check-up. You wanna know what’s going on in there, right?

If you find an error on your report – maybe the default date is wrong, or it’s an account you never even had – you can dispute it. It’s not always easy, but it’s totally worth it. You’re basically telling the credit bureau, “Hey, something’s not right here!”

If the default is accurate, well, then it’s time to get your financial house in order. That means paying your bills on time, every time. This is the most crucial thing you can do to rebuild your credit. It's the bedrock of good credit. Seriously, set up reminders, auto-pay, whatever works for you. Just don’t miss another payment.

Also, try to pay down any outstanding debts. The lower your credit utilization ratio (that’s how much credit you’re using compared to how much you have available), the better. Think of it as decluttering your financial life.

And remember, consistency is key. A few months of good behavior won’t magically fix years of financial missteps. It takes time, patience, and a whole lot of responsible decision-making to see real improvement.

The Takeaway: Be Patient and Persistent

So, to wrap this up with a nice little bow, a default generally stays on your credit report for seven years from the date of delinquency. For major things like bankruptcies, it can be longer.

It’s a significant mark, and it’s going to affect your credit score and your ability to get credit for that entire period. But it’s not the end of the world. It’s a bump in the road, a tough lesson.

The most important thing is to learn from it. Be responsible going forward. Pay your bills on time. Keep your credit utilization low. And eventually, with time and good habits, your credit score will recover. It’s like tending to a garden – it takes consistent effort to see it bloom again.

So, don’t despair. Just be aware, be proactive, and be patient. Your credit report is a marathon, not a sprint. And you’ve got this! Now, who needs a refill?