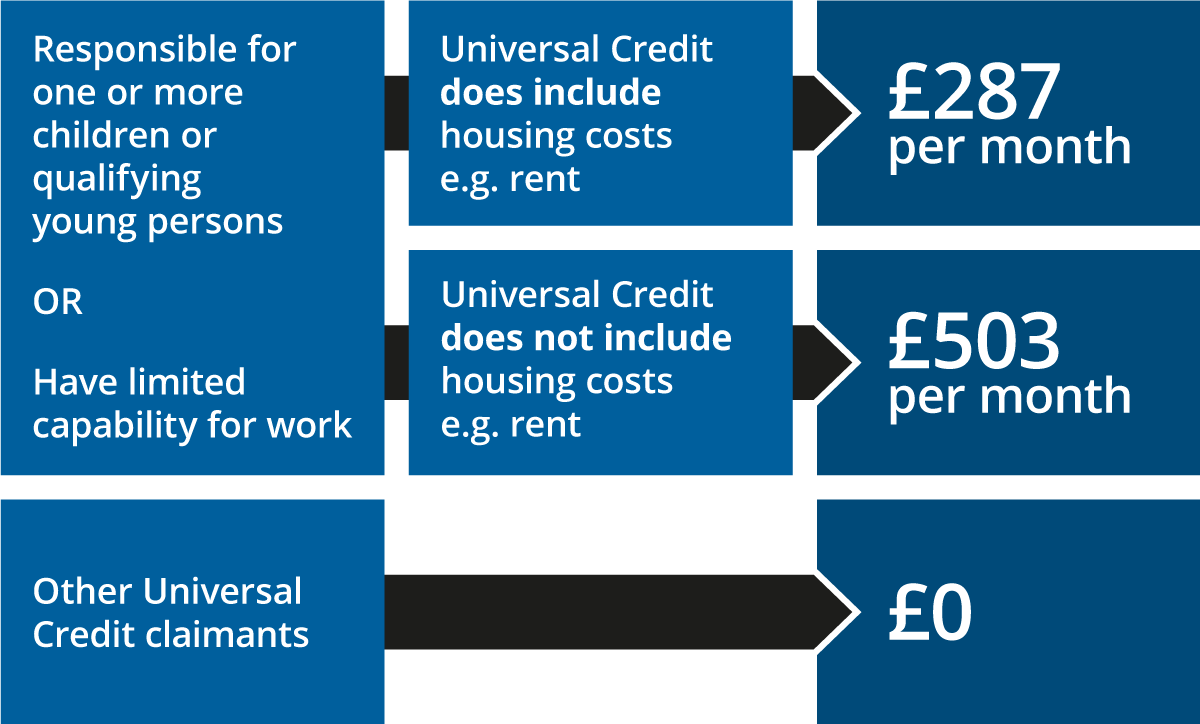

How Long Does Inheritance Affect Universal Credit

So, you've had a bit of unexpected good fortune land in your lap, perhaps from a much-loved relative who's popped off to the great big bingo hall in the sky. And now you're wondering about your Universal Credit. It’s a bit like a financial rollercoaster, isn't it? One minute you’re on a steady track, the next you’re wondering if this new cash injection is going to send you flying off the rails. Let's dive into this exciting, sometimes slightly baffling, world of inheritance and how it plays with your Universal Credit.

First things first, getting an inheritance is usually a wonderful thing! It’s a testament to someone's love and care, and it can offer a real safety net or even a chance to get ahead. But, when it comes to the government's welfare system, they tend to like to keep an eye on everyone's pockets. Think of Universal Credit as a very diligent friend who always asks, "So, what's new financially?"

Now, the big question: how long does this inheritance party affect your Universal Credit? The simple answer is: it depends! It's not a one-size-fits-all kind of deal. The most important thing to remember is that the rules are pretty clear about capital. Your inheritance is considered 'capital'. And the government has a couple of magical numbers for this capital thing.

There are two main thresholds: the lower capital limit and the higher capital limit. If your inheritance, plus any other savings and investments you have, pushes you over the higher capital limit, then sadly, your Universal Credit claim is likely to stop. Think of this higher limit as the "You've got enough, thanks very much!" line. At the moment, that magic number is £16,000. So, if your total savings and investments go above this, you won't get Universal Credit anymore.

But what if your inheritance is a bit more modest? This is where the lower capital limit comes into play. This limit is currently set at £6,000. If your total capital is between the lower and higher limits (so, between £6,000 and £16,000), your Universal Credit won't stop completely, but it will be reduced. How much it's reduced by is quite a clever calculation. For every £250 (or part of £250) that your capital is over the lower limit, you'll lose £4.70 from your monthly Universal Credit payment. It's like a slow, steady tick-down.

This reduction is often called 'tariff income'. It’s as if the government assumes your money is earning a bit of interest, even if it's just sitting in your bank account. So, even a few thousand pounds can make a difference to your monthly payments. It’s this gradual chipping away that makes the whole process so interesting to watch!

The other crucial factor is how quickly you spend this money. If you're sensible and spend down your inheritance to below the lower capital limit of £6,000, then your Universal Credit payments can start to return to their full amount. This is where the 'how long' question really gets its answer. It’s entirely in your hands, or rather, in your spending habits!

So, if you inherit, say, £10,000, and you have no other savings, you’ll be in that middle bracket. Your Universal Credit will be reduced. If you then decide to use £5,000 of that inheritance to, for example, pay off some debts, buy a car you desperately need, or even put a deposit down on a place to live, your remaining capital will drop. If it falls below £6,000, your Universal Credit should go back up. It’s a dynamic game!

It's super important to be upfront and honest with the Department for Work and Pensions (DWP) about your inheritance. Keeping it a secret is never a good idea and can lead to bigger problems down the line. When you receive the money, you need to declare it. They’ll then assess how it affects your Universal Credit. Think of them as the referees in this financial game.

What makes this whole situation so fascinating is the personal journey it represents. An inheritance can be a chance to change your circumstances, to finally tackle those nagging financial worries, or even to invest in your future. The way Universal Credit interacts with it is a direct reflection of these big life changes.

It’s not just about the numbers; it’s about the possibilities. Maybe that inheritance means you can afford to take a course to improve your skills, or perhaps it allows you to move to a place with better job opportunities. The reduction in Universal Credit might be a temporary blip on your path to greater financial independence. It’s a sign that you’re moving up in the world, financially speaking.

Some people might find it a bit frustrating, of course. But look at it as a nudge. A nudge to think strategically about your money. How can you best use this windfall? Is it better to have a slightly reduced Universal Credit payment while you slowly spend down your savings, or to use the money quickly to get yourself on a more stable footing? These are the juicy questions!

The key takeaway is this: an inheritance will affect your Universal Credit, but the duration and impact depend on how much you receive and how you choose to use it. It’s a temporary dance, a financial negotiation. So, if you're in this situation, get informed, be honest, and then strategise. It's your money, your inheritance, and your journey. And navigating the system, while it might seem daunting, is part of making the most of this special gift.

Remember, the DWP website has all the official details, and talking to them directly or seeking advice from a welfare rights organisation can be incredibly helpful. They can guide you through the specifics of your situation. It's like having a personal financial guide for this particular chapter of your life. Embrace the process; it’s a unique part of managing your money and your benefits!