How Long Does The Underwriting Process Take For A Mortgage

Ah, the mortgage! That magical piece of paper that unlocks the door to your very own castle (or, you know, a charming fixer-upper). You’ve found the one, signed the paperwork, and now you’re dreaming of paint swatches and furniture layouts. But then comes the underwriting process. It sounds a bit like a secret agent mission, doesn't it? All hushed tones and mysterious evaluations. So, how long does this whole underwriting shindig really take? Buckle up, buttercups, because we’re about to dive into the sometimes-hilarious, often-frustrating, and ultimately heartwarming journey of getting your mortgage approved.

Imagine the underwriter as a super-sleuth, but instead of chasing criminals, they’re chasing down every single piece of information about your financial life. They’re the gatekeepers of your homeownership dreams, and their job is to make sure you’re not about to, you know, spontaneously combust financially after signing on the dotted line. Think of them as your financial guardian angel, albeit one who’s really, really good with spreadsheets and has the patience of a saint.

So, what’s a typical timeline? Well, just like a perfectly baked cookie, it depends on the ingredients! On average, you’re looking at anywhere from 20 to 45 days. That’s a good chunk of time, right? Enough to plan a surprise party for your future self, or maybe even learn a new language. But remember, this is just an average. Sometimes, if all your ducks are in a perfectly aligned row, it can be as quick as 10 days. Imagine that! You're practically skipping into your new home, still smelling the fresh paint. It's like winning the financial lottery!

However, life, as we know, is rarely that simple. If there are a few quirks in your financial story – maybe a slightly unusual income source, a previous blip on your credit report (we’ve all had those moments, haven’t we?), or you’re buying a property that’s a bit… unique – the process can stretch. We’re talking potentially 60 days or even longer. This is where the patience of a saint really comes into play. You might find yourself staring at your phone, willing it to ring with good news, while simultaneously re-watching your favorite comfort show for the tenth time. It’s a marathon, not a sprint, my friends.

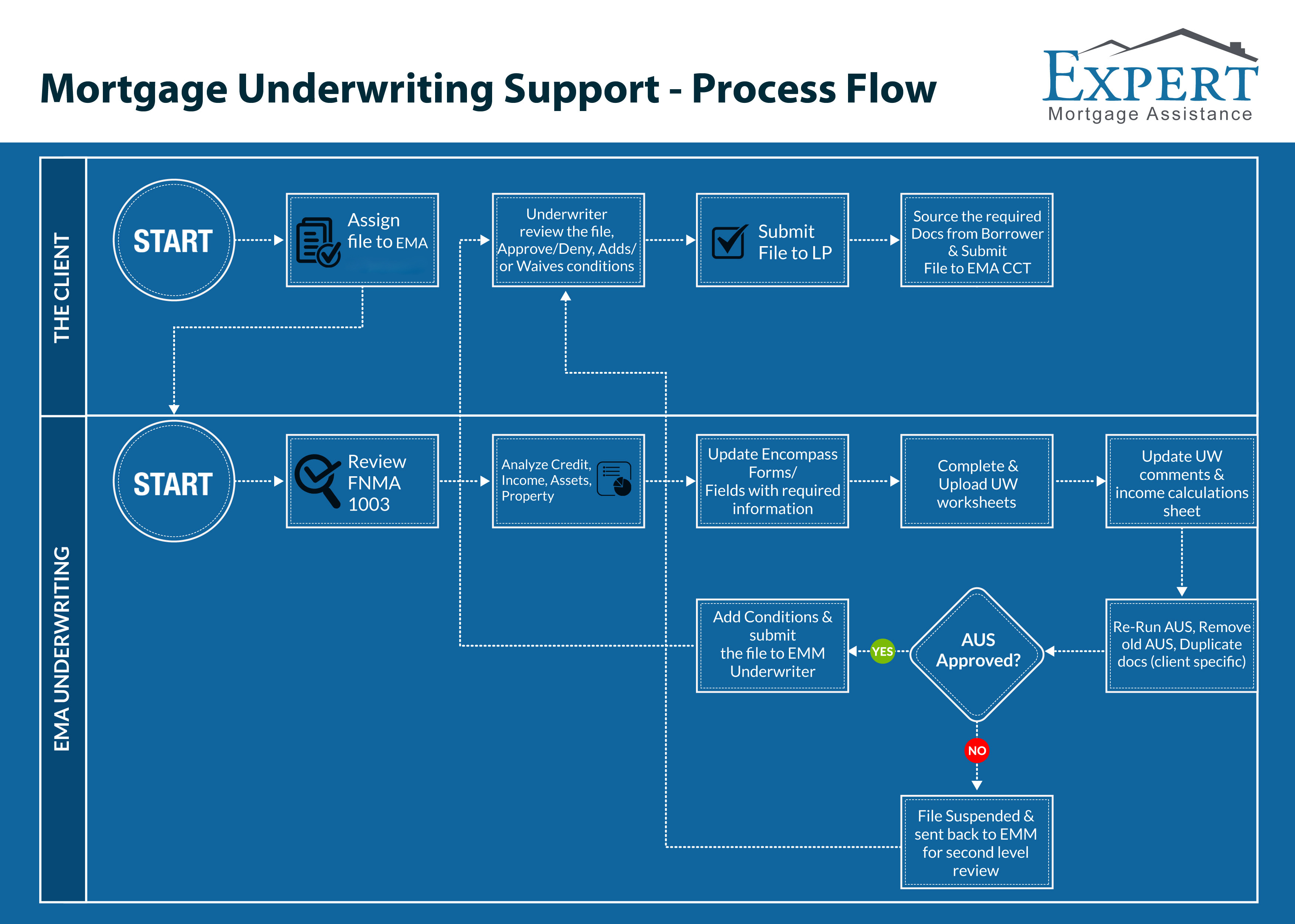

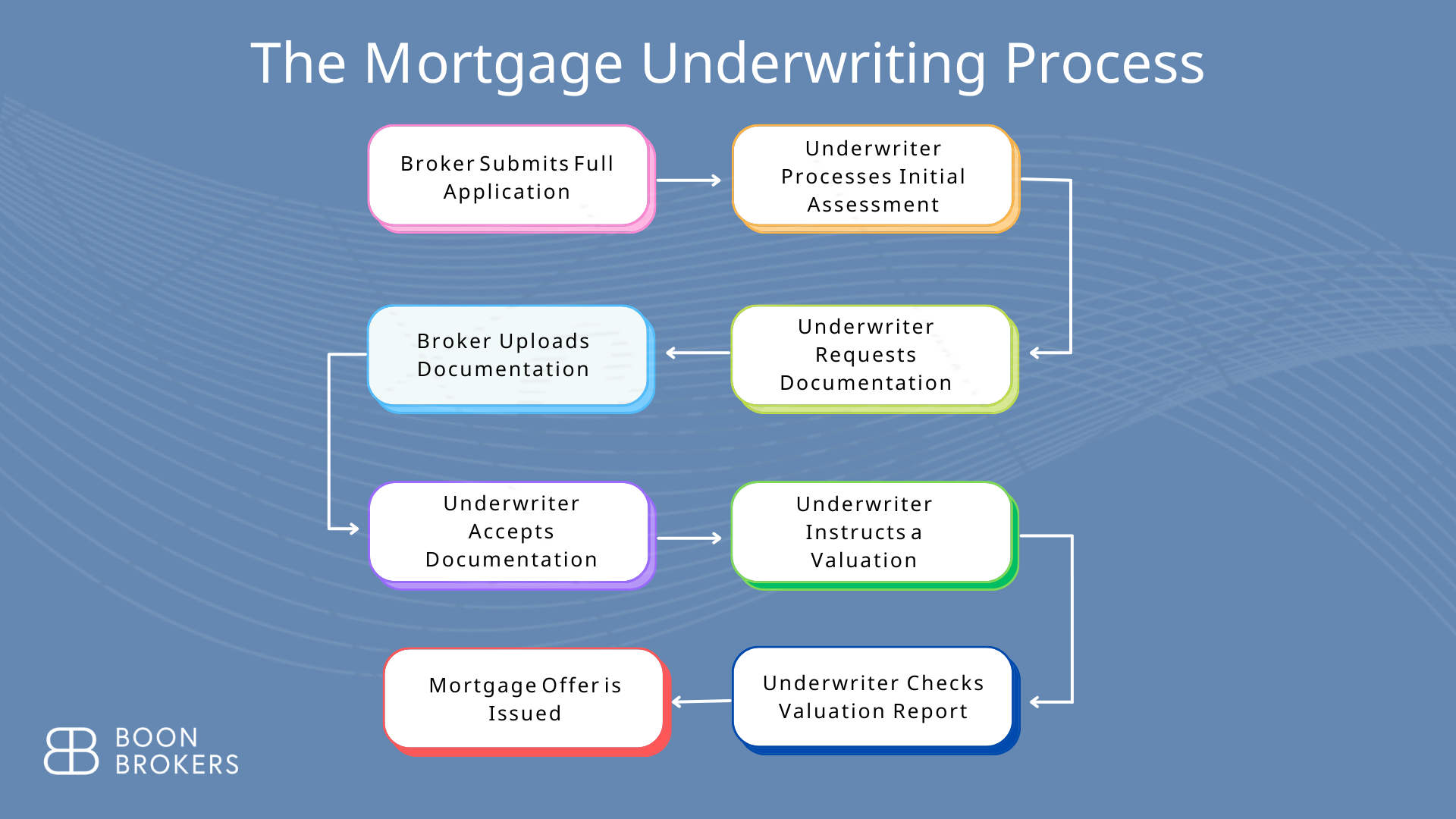

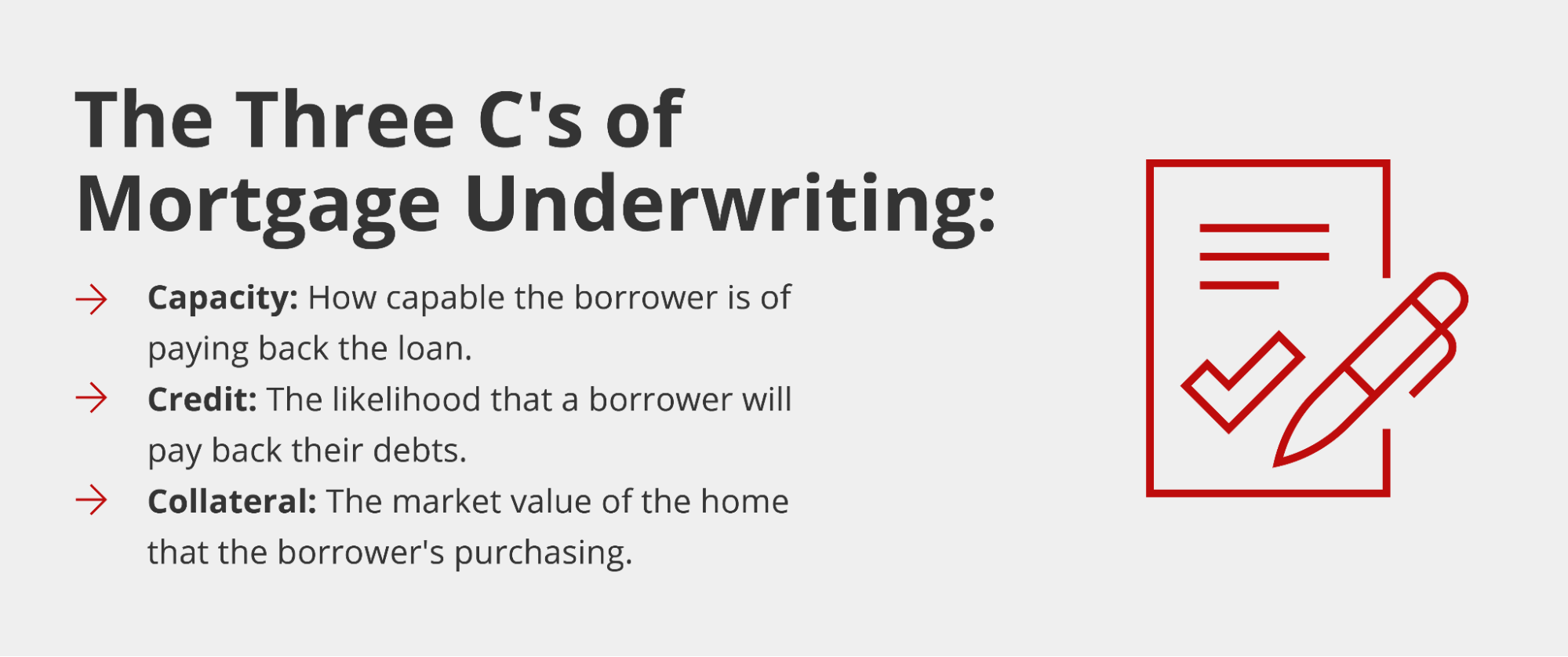

What actually happens during this time? It’s a bit like a treasure hunt for your finances. The underwriting team pores over your income verification (they want to make sure you’re not just pretending to have a job), your credit report (did you really pay that parking ticket from 2018?), and your debt-to-income ratio (are you living on ramen noodles and good vibes?). They also scrutinize the appraisal of your home. Imagine the appraiser as a discerning art critic, but for houses. They're making sure your potential castle is worth the king's ransom the bank is lending you.

“Sometimes, the underwriter is like a detective who loves a good puzzle. They’ll dig into your bank statements, your tax returns, and maybe even the ingredients list of your favorite obscure snack. It's all about building a complete picture.”

One of the most common reasons for delays? Missing documentation. It's like forgetting your keys when you're already halfway to the airport. You've got all your suitcases packed, you're ready to go, but… oh no! You need that one specific form. So, be prepared to be a document-gathering ninja. Your loan officer will likely send you a list, and it's your mission, should you choose to accept it, to round up every single item. Think of it as an epic quest for financial confirmation!

There are also those heartwarming moments, though. Sometimes, an underwriter will see a story behind the numbers. Maybe you had a temporary setback due to caring for a family member, or you’ve been diligently saving every penny for years. In these instances, a good underwriter might go the extra mile to understand your situation. It's like finding a compassionate librarian who helps you find that rare book you've been searching for – a bit of human kindness in the midst of all the financial rigor.

And then there are the surprises! You might get a call asking about a small, seemingly insignificant deposit from years ago. Suddenly, you’re transported back in time, racking your brain to remember that garage sale where you sold that slightly hideous lamp. The underwriter just wants to understand, and sometimes, your explanation can be downright hilarious. You might even develop a sort of quirky relationship with your underwriter, sharing amusing anecdotes about the financial mysteries you’re unearthing together.

Ultimately, the underwriting process is a testament to the fact that buying a home is a big deal. It’s not just about signing papers; it’s about building a future. The underwriters, in their diligent (and sometimes slightly obsessive) way, are helping to ensure that your dream of homeownership is built on a solid foundation. So, while you might be tapping your foot and checking your email a little too often, remember that this process, with all its twists and turns, is ultimately working in your favor. It’s the final hurdle before you can truly call a place your own, and that’s a pretty wonderful thing to wait for. Just try to enjoy the journey, maybe even with a good sense of humor. After all, you’re on your way to a new chapter, and that’s something worth celebrating!