How Much Am I Allowed To Earn Before Paying Tax

Hey there, coffee buddy! Let’s chat about something that can feel a bit like a mystery, right? That whole “how much can I actually keep before the tax folks start knocking?” question. It’s the million-dollar query, or maybe, just the few-thousand-dollar query. You know, that sweet spot where you’re making some dough but not feeling like you’re handing over half your paycheck to Uncle Sam. So, how much am I allowed to earn before paying tax? It’s a question that pops up more often than a rogue sock in the dryer, I swear.

Now, before we dive in, let’s get one thing straight. I’m not a tax professional, okay? Think of me as your friendly neighborhood guide, pointing you in the right direction. The real nitty-gritty, the super-duper official stuff, is best left to the pros. But we can totally get a handle on the general idea, right? It’s like knowing how to read a map without being a cartographer. We’re aiming for understanding, not a full-blown tax audit seminar. Phew!

So, the short answer, and I know you love a good short answer, is… drumroll please… it depends! Gasp! I know, I know, it’s the most annoying answer ever, isn’t it? It's like asking your friend what's for dinner and they say, "Whatever we feel like!" But seriously, it truly does depend. And it depends on a whole bunch of things, like where you live, whether you’re flying solo or part of a tax-filing duo, and what kind of income we’re even talking about. So many variables, it’s enough to make your head spin like a record on the fritz!

Let’s break it down a little, shall we? We’re talking about something called a tax-free allowance or a personal allowance. Think of it as your personal bubble of income that the government says, "Alright, you can keep this much, no sweat." It’s like a free pass for your hard-earned cash. Pretty neat, huh? This is the amount you can earn before you even have to think about income tax. It’s your initial shield against the tax man’s reach. This is the golden ticket, the get-out-of-jail-free card for your earnings!

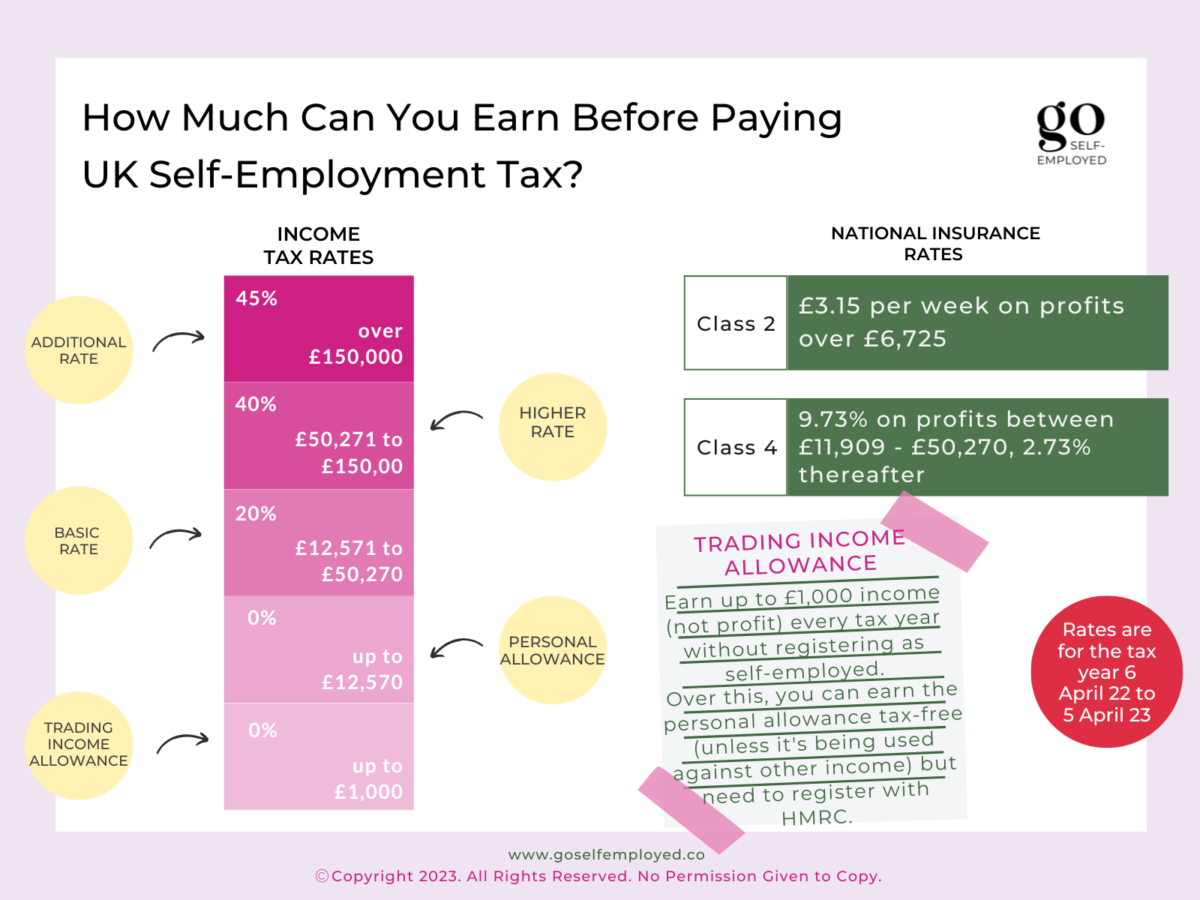

In the UK, for instance, this is a pretty generous chunk of change. For the current tax year, most people get a personal allowance of £12,570. That’s a decent amount, right? So, if you’re earning, say, £12,000 a year, congratulations! You’re probably not paying any income tax. You can high-five yourself, do a little jig, and spend that money guilt-free. It’s your money, after all, earned through blood, sweat, and maybe a few tears from that really tough project at work.

But here’s where it gets a little bit more complicated, and I’m not going to lie, it can be a tad confusing. That £12,570 isn’t set in stone for everyone. Nope. There are people, and you might be one of them, whose personal allowance gets reduced. It’s like a shrinking violet. And this happens when you start earning more than a certain amount. They call this the High Income Child Benefit Charge, which is a mouthful, I know, but basically, if you or your partner receive child benefit and one of you earns over £50,000, your personal allowance starts to dip. For every £2 you earn over £50,000, you lose £1 of your personal allowance. So, if you’re earning £60,000, poof! Your personal allowance is gone. Kaput. Vanished into thin air. And if you earn over £100,000, your personal allowance is zero. Zilch. Nada. So, if you’re in that higher earning bracket, you’ll be paying tax on all your income. Bummer, I know.

It’s like a sliding scale of generosity. The more you earn, the less of that special tax-free allowance you get to keep. It's a bit of a game, isn't it? A really important game with real money involved. And we all want to play it right, so we don't end up with a nasty surprise in the mail. Nobody wants that, right? The dreaded red envelope. Shudder.

Now, let's talk about different types of income. Because not all money is created equal in the eyes of the taxman, apparently. That £12,570 we were talking about is usually for your employment income. That’s the salary you get from your job. Easy enough, right? But what about if you’re a freelancer, a side-hustler, or raking in cash from investments? Ah, this is where it gets interesting!

For self-employed individuals, the rules can be a little different. You still get a personal allowance, but you’ll be reporting your income through something called Self Assessment. It’s a whole system designed for folks who aren’t on a PAYE (Pay As You Earn) system. You have to keep track of your income and expenses, and then tell HMRC (Her Majesty’s Revenue and Customs, for those not in the know) all about it. It’s like being your own mini-accountant. Exciting, right? Well, maybe not exciting, but necessary.

And then there are things like rental income from properties you own. Or dividend income from shares you’ve invested in. Or even interest from your savings accounts. These often have their own specific allowances and tax rates. For example, there’s a trading allowance of £1,000 for small trading or miscellaneous income. If your side hustle or casual earnings are under that, you might not need to declare it at all! Boom! More money in your pocket. It’s like finding a forgotten fiver in an old coat. A pleasant surprise.

The dividend allowance is currently £1,000 for the tax year 2023-24. So, if you receive up to £1,000 in dividends, you won’t pay any tax on it. After that, dividends are taxed at different rates depending on your income tax band. It’s a bit like a tiered cake – the first slice is free, but then you start paying for the fancier layers.

And let’s not forget savings interest. For most people, you get an annual savings allowance. This means you can earn a certain amount of interest tax-free. For basic-rate taxpayers, it’s £1,000. For higher-rate taxpayers, it’s £500. If you’re an additional-rate taxpayer, well, sorry, no allowance for you! Again, it’s about your overall income level. It’s like a VIP club, and higher earnings mean you don't get the free pass on savings interest.

So, to recap this little adventure, you have your main personal allowance for your employment income. Then you’ve got separate allowances for things like dividends and savings interest. And if you’re self-employed, there’s that whole Self Assessment world to navigate. It’s a lot to keep track of, I know. It’s like juggling flaming torches while riding a unicycle. Potentially dangerous if you drop something!

Now, what about allowances for married couples or civil partners? This is where things can get even more interesting, especially with things like the Marriage Allowance. If one of you is a basic-rate taxpayer and earns less than your personal allowance, and the other is a non-taxpayer, you can actually transfer up to 10% of your unused personal allowance to your partner. This can result in a tax saving of up to £250 a year. It’s like a little financial boost for your partnership. Who doesn't love a little extra cash, especially when it's for your significant other? It’s a win-win situation!

This Marriage Allowance is a fantastic way to reduce your combined tax bill. It’s not a huge amount, but every penny counts, right? Especially when you’re trying to save for that dream holiday or a new sofa that doesn’t have questionable stains. It's those little wins that make life a bit sweeter.

And what about allowances for parents? Well, as we touched on with the Child Benefit charge, having children can definitely impact your tax situation, but not always in a way that directly increases your tax-free allowance. The child benefit itself is a payment from the government to help with the costs of raising children. But if your income goes over a certain threshold, you might have to pay some of it back through a tax charge. So, it's more about receiving support rather than a direct tax-free allowance on your earnings due to having kids. It's a bit of a tricky one, and it's easy to get confused. You're getting money, but then you might have to give some back. It’s like a boomerang. It comes back to you, but not quite in the same way you sent it out.

Let’s talk about tax bands. Once you’ve used up your personal allowance, any additional income falls into different tax bands. In the UK, there are typically basic rate, higher rate, and additional rate bands. So, the first bit of income above your personal allowance is taxed at the basic rate (currently 20%). Then, if you earn more, you hit the higher rate band (currently 40%), and then the additional rate band (currently 45%). It’s like climbing a ladder of tax rates. The higher you climb, the more you pay. And those higher bands kick in at different income levels, so what counts as “higher rate” for one person might be “basic rate” for someone earning more. It’s a bit of a tiered system, designed to tax those who can afford to pay more.

The threshold for these bands changes, so it’s worth keeping an eye on. For the 2023-24 tax year, the basic rate is up to £37,700 (after your personal allowance), the higher rate is from £37,701 to £125,140, and anything above that is the additional rate. So, if your income is £30,000, you'll pay 20% tax on £17,430 (£30,000 minus your £12,570 allowance). If your income is £50,000, you'll pay 20% on the first £25,130 (which is £37,700 minus your £12,570 allowance) and then 40% on the remaining £12,300 (£50,000 minus £37,700). See? It’s a bit of a mathematical puzzle. A puzzle that affects your wallet!

So, when you’re asking yourself, “How much am I allowed to earn before paying tax?”, remember that it’s not a single, simple number for everyone. It’s a combination of your personal allowance, any other allowances you might be eligible for, and the specific tax bands that apply to your income. It’s like a financial cocktail – a mix of different ingredients that create your final tax situation. And the recipe can change depending on your circumstances.

The key takeaway, my friend, is that understanding these allowances is super important. It helps you budget better, plan your finances, and avoid any nasty surprises. It’s about being in control of your money, rather than letting it control you. And who doesn’t want that? We’re all trying to make the most of our hard-earned cash, so a little bit of tax knowledge goes a long way. It’s like having a secret superpower for your finances.

If you’re ever in doubt, or if your financial situation is a bit complex, please, please, please consult a qualified accountant or tax advisor. They’re the wizards who can navigate the labyrinth of tax laws and make sure you’re not paying a penny more than you have to. And they can also make sure you’re not accidentally breaking any rules, which is equally important! Nobody wants to be on the wrong side of the law, especially when it comes to money. So, get yourself a tax guru, and sleep soundly at night knowing your finances are in good hands. They’re the real MVPs of the tax world!

But for a general idea, that £12,570 personal allowance is your starting point for employment income. Anything above that starts to get taxed, unless you have other specific allowances or reliefs that apply. It’s the foundation of your tax calculation. Build on that wisely, and you’ll be a lot happier with the outcome. So, go forth and earn, but earn smart, and keep a little bit of that knowledge tucked away for when you need it. Cheers to understanding our finances!