How Much Does Cosmatic Claims On Insurance Increase Premiums By

Let's be real. When you're browsing through the latest beauty trends online, or perhaps indulging in a little retail therapy, the last thing on your mind is your insurance premium. We're talking about that delightful serum that promises to erase your fine lines, or maybe that daring new hair color you've been eyeing. These are the things that bring a little sparkle to our lives, right? But then, a thought might just nudge its way in, perhaps after a particularly successful beauty treatment: "Does this affect my insurance?"

And it’s not just about those fancy treatments. Think about it. We all have our little quirks and preferences. Some of us are meticulous about our skincare routines, others might be more adventurous with cosmetic procedures. It's all part of the modern tapestry of self-care and personal expression. But the universe, in its own quirky way, likes to keep things balanced. And sometimes, that balance involves the sometimes-mysterious world of insurance.

So, let's dive into this fascinating, and sometimes slightly nerve-wracking, intersection of beauty and premiums. How much does a cosmetic claim really impact your insurance costs? Grab a comfy blanket, maybe a soothing cup of herbal tea, and let's unravel this together. No complex jargon, just a friendly chat.

The Cosmetic Conundrum: It’s Not What You Think

First off, let's clear the air. For the most part, your routine beauty treatments – think facials, manicures, pedicures, or even that eyebrow microblading you’ve been considering – are generally not something you’d claim on your insurance. These are typically considered elective, purely for aesthetics and personal enjoyment. And insurance, at its core, is designed to protect us against unexpected and significant financial losses due to unforeseen events. A slightly imperfect manicure doesn't quite fall into that category, does it?

However, the conversation gets a little more nuanced when we talk about cosmetic procedures that might arise from accidents or medical necessity. For instance, if you've had an accident that resulted in facial disfigurement, and a reconstructive surgery is recommended, that's a whole different ballgame. In such cases, the primary purpose of the procedure is medical – to restore function or appearance due to injury. This is where your insurance might actually step in.

When Does Insurance Get Involved?

The key differentiator is medical necessity versus purely cosmetic enhancement. If a procedure is deemed medically necessary by a qualified healthcare professional, it’s far more likely to be covered by your health insurance. This could include things like reconstructive surgery after an accident, breast reconstruction after a mastectomy, or even certain procedures to correct congenital defects. These aren't about chasing a youthful glow; they're about restoring health and well-being.

But here’s where the cosmetic claim could indirectly lead to a premium increase, albeit not in the way you might initially imagine. If a health insurance claim is filed for a procedure that is partially cosmetic, even if it has a medical component, the insurer might assess the overall cost. While they may cover the medically necessary portion, the overall interaction with the insurance system, including the processing of claims, can sometimes play a small role in future premium calculations. It’s a bit like your car insurance premium going up after a minor fender-bender, even if the repair wasn't astronomically expensive. The fact that a claim was made is a data point.

The Unseen Ripple: How Claims Can Affect Your Premium

Now, let's get to the heart of it. If you do have a situation where a cosmetic procedure, or a procedure with a significant cosmetic component, is filed as an insurance claim (and this is usually only if there’s a strong medical justification), how much does it actually nudge your premium upwards? The answer, frustratingly, is often: it depends.

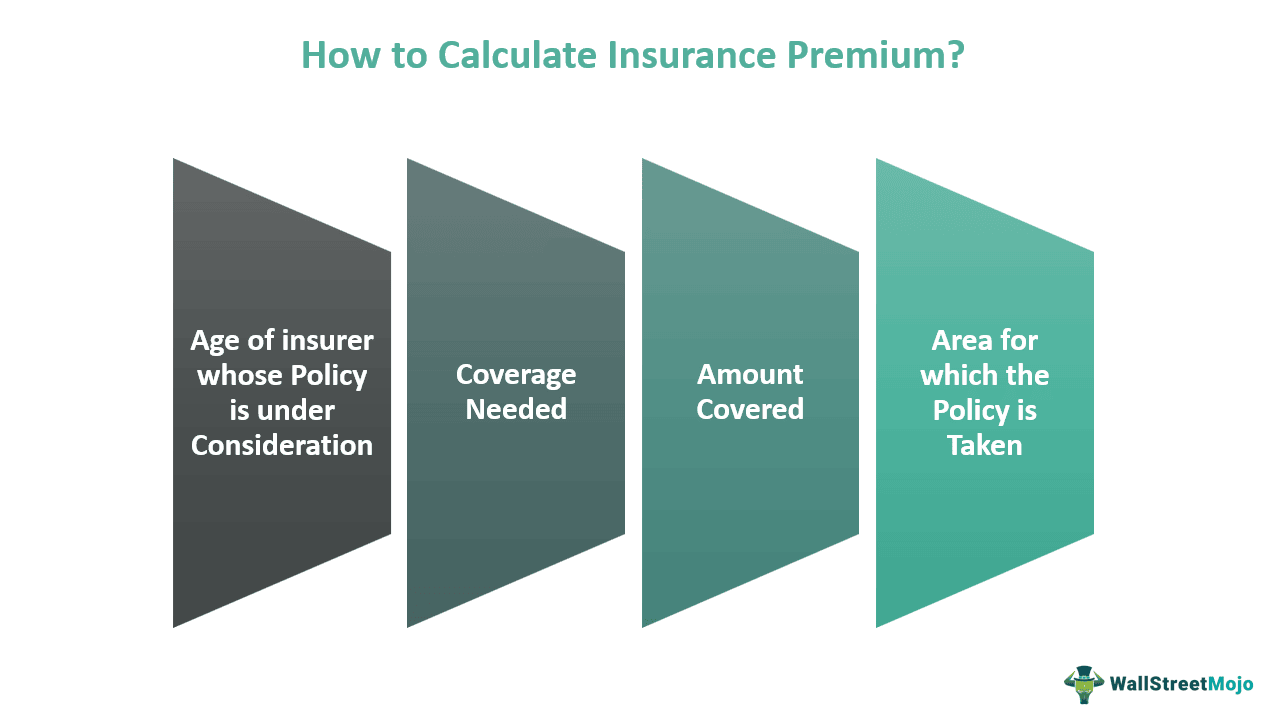

There's no universal price tag. Insurance premiums are calculated based on a complex algorithm that considers a multitude of factors. These can include:

![[HELP] Total cost of Insurance premiums paid in any given year since](https://external-preview.redd.it/opMRDRggIidtEchY7emfyoZXAZeY77yEQcF_cNSRVlA.png?auto=webp&s=847bf2d57a75cdd63932b137ef7b63e7669e3df8)

- Your age: Older individuals generally have higher premiums.

- Your health history: Pre-existing conditions can influence costs.

- Your location: Healthcare costs vary geographically.

- The type of policy: Different plans have different coverage levels and deductibles.

- The specific claim: The amount claimed, the nature of the procedure, and its perceived risk.

- Your insurer's risk assessment: Each company has its own way of evaluating potential future claims.

So, a single cosmetic-related claim, even if it’s a larger sum, might have a minimal impact if you're otherwise a low-risk policyholder. Conversely, if you have a history of claims or other factors that already place you in a higher-risk bracket, even a seemingly small cosmetic claim could be the straw that breaks the camel's back, so to speak.

The "Cosmetic" Label: A Stigma?

It’s also worth noting that insurance companies are generally quite savvy. They can often distinguish between a medically necessary procedure and one purely for aesthetic enhancement. If a claim is filed for something that is unambiguously cosmetic and not medically justified, it’s highly likely to be denied outright. This denial, in itself, wouldn't typically affect your premium. It's the approved claims that become part of your insurance profile.

Think of it like this: if you go to a fancy restaurant and order the most expensive caviar, and then have to ask the waiter to send it back because you didn’t like it, the restaurant might not charge you for it. But if you eat the whole thing and then try to get a refund, that's a different story. Insurance works similarly. They're there to cover the "unexpected meal gone wrong," not the "choice to order the pricey appetizer."

Beyond the Premium: Other Considerations

The impact of a cosmetic claim isn't always just about the monetary increase in your premium. There are other nuances to consider:

1. Deductibles and Co-pays:

Even if a procedure is partially covered, you'll likely still have to meet your deductible and co-pays. This means you’ll be footing a portion of the bill upfront, regardless of the premium increase. So, a claim, even if it leads to a small premium hike, also means an immediate out-of-pocket expense.

2. Policy Limits and Exclusions:

Many health insurance policies have specific exclusions for cosmetic procedures. This means they simply won't cover them, no matter what. It's crucial to read your policy details carefully to understand what is and isn't covered before you book that procedure.

3. Negotiating with Insurers:

In cases of medically necessary cosmetic procedures (like reconstructive surgery), you might have some leverage. If your doctor strongly recommends the procedure for functional or psychological well-being, they can often provide documentation that helps justify the claim. This documentation can be key to getting coverage and potentially mitigating any negative impact on your premium.

4. The "Accident" Factor:

If a cosmetic alteration is the result of an accident, the accident itself is the primary trigger for the claim. The subsequent reconstructive surgery, while having a cosmetic element, is seen as a direct consequence of the injury. This generally makes it more likely to be covered and less likely to be solely viewed as an elective cosmetic expense by the insurer.

Fun Facts and Cultural Touchstones

Did you know that the concept of cosmetic enhancement has been around for millennia? Ancient Egyptians used pigments to enhance their eyes and lips, and Roman elites would use chalk to lighten their skin. Fast forward to today, and we have everything from injectables to intricate surgeries. It’s a testament to our enduring desire to feel and look our best.

Consider the iconic Marilyn Monroe. While she was a natural beauty, she reportedly received some subtle cosmetic interventions. Back then, the insurance landscape was vastly different, but the underlying human desire for perceived perfection has always been a constant. Today, with the democratization of beauty treatments, the line between medical necessity and personal choice can sometimes blur.

In the realm of television, shows like "Extreme Makeover" and "Botched" often highlight the more dramatic aspects of cosmetic procedures. While entertaining, they also serve as a reminder of the significant financial and emotional investments people make in their appearance. And while these shows rarely delve into the insurance implications, they offer a glimpse into the world where appearance and health often intersect.

Practical Tips for Navigating the Beauty-Insurance Maze

So, how can you enjoy your beauty journey without causing a financial headache with your insurance?

Tip 1: Read Your Policy!

This is the golden rule. Before you commit to any procedure that might have a medical component, read your insurance policy. Understand your coverage, your deductibles, and any exclusions related to cosmetic procedures. Don't be afraid to call your insurance provider and ask clarifying questions. It’s better to be proactive than to be surprised later.

Tip 2: Consult Your Doctor First.

If you're considering a procedure that could be medically justified, have a thorough discussion with your doctor. Get their professional opinion on medical necessity. Their documentation can be your strongest ally when dealing with insurance companies.

3. Get Pre-Approval.

If you believe a procedure might be covered, always seek pre-approval from your insurance company. This process involves submitting details of the proposed treatment for their review. Pre-approval can save you a lot of heartache (and money) down the line.

4. Understand the "Why."

Be clear in your own mind, and with your healthcare provider, about the primary reason for the procedure. Is it to correct a medical issue, or is it purely for aesthetic preference? This clarity will help you in discussions with your insurer.

5. Consider Out-of-Pocket Costs.

For purely cosmetic procedures that are unlikely to be covered, budget accordingly. Look for reputable providers who offer transparent pricing and payment plans if needed. The peace of mind of knowing the exact cost upfront is invaluable.

A Gentle Reflection

In the grand scheme of things, our pursuit of beauty, well-being, and self-improvement is a natural and beautiful part of the human experience. Whether it's the thrill of a new haircut or the confidence gained from a corrective procedure, these are all about enhancing our lives. The insurance landscape, while sometimes complex, is designed to provide a safety net for the unexpected.

So, while it's wise to be aware of how cosmetic claims might influence your premiums, it shouldn't prevent you from making choices that contribute to your happiness and health. The key is to be informed, to communicate effectively, and to understand the subtle but significant difference between a treat-yourself moment and a genuine need. In the end, the most valuable asset you have is your well-being, and making informed decisions about both your appearance and your finances is a crucial part of nurturing that.