How Much Does Insurance Go Up After An Accident

Let's talk about something that, let's be honest, can send a shiver down anyone's spine: car accidents. We all try our best to be super-vigilant, right? Like that episode of Seinfeld where George is trying to become a "master of his domain" – in this case, the domain is the road, and the master is… well, you!

But sometimes, despite our best intentions and superhuman reflexes, things happen. A rogue squirrel, a moment of distraction, a slick patch of road – suddenly, you're staring at a fender bender. And then comes the inevitable question, the one that echoes in your mind as the tow truck pulls away: "How much is my insurance going to jump after this?"

It’s a bit like asking, “How long is a piece of string?” but with more dollars involved. The truth is, there’s no single, universal answer. Your insurance premium isn’t a set-it-and-forget-it kind of deal. It’s a dynamic beast, constantly recalculating your risk profile. Think of your insurance company as a high-stakes poker player, and your accident is like a revealed hand of cards – they're reassessing the odds.

The Big Reveal: What Actually Happens to Your Premium?

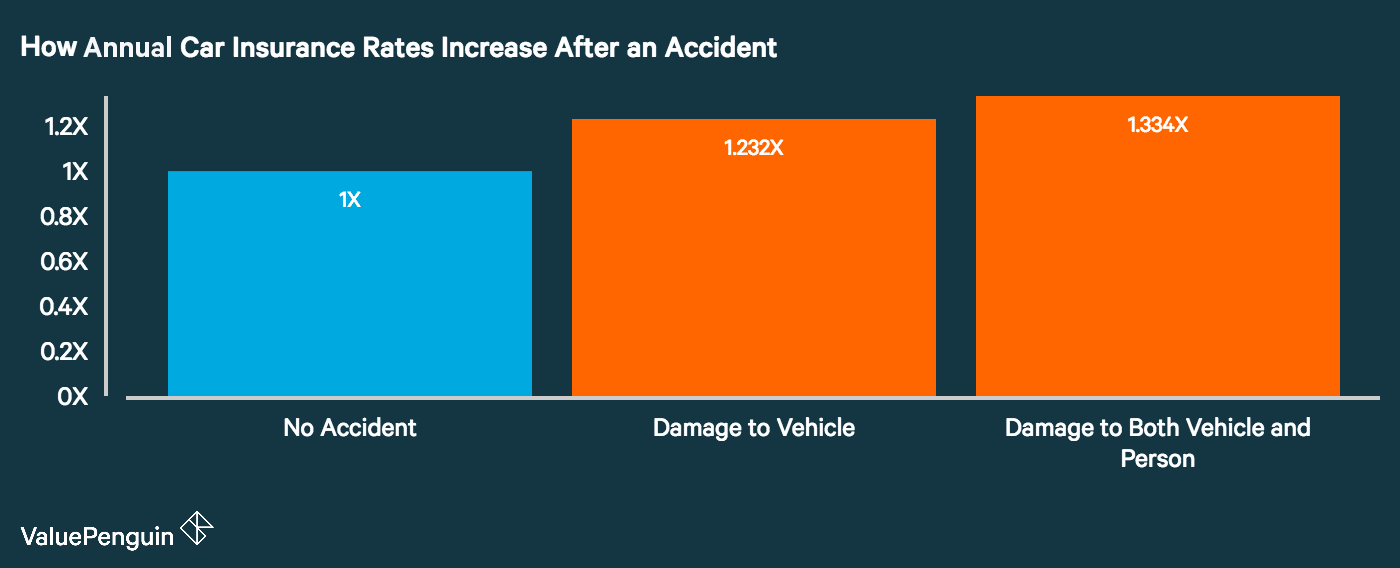

So, let's break down the mystery. When you file a claim after an accident, your insurance provider will do a few key things. Firstly, they'll assess the severity of the damage. Was it a minor scrape that barely ruffled your car's paint job, or a full-blown symphony of crunching metal?

Secondly, and perhaps most importantly, they’ll determine who was at fault. This is where things can get a little nuanced. If you were clearly the at-fault driver, expect a more significant impact on your premium. If it was a no-fault accident, or the other driver was deemed responsible, the increase might be minimal or even non-existent. It’s like a grading system, and "guilty" usually means a lower grade on your insurance report card.

A fun little fact: In some states, like Massachusetts and Michigan, there are specific laws about how much your rates can increase after an accident, regardless of fault. So, your location can play a surprisingly big role in the post-accident financial fallout. It's not just about your driving; it's about the driving rules of the land!

Factors That Play the Premium Game

Beyond fault and damage, several other factors influence the premium increase. Your driving record is your insurance resume. A spotless record with years of safe driving is your superpower. One accident, especially if it's your fault, can temporarily dim that superpower.

Your coverage levels also matter. If you have comprehensive and collision coverage, which are designed to cover damage to your own vehicle, you'll likely see a bump if you use them to fix your car after an accident. It’s like using your warranty – it signals that you've utilized their service for a specific event.

And let's not forget your insurance history. If this is your first rodeo with an accident, insurers might be more lenient, viewing it as an anomaly. However, if you have a history of claims or tickets, that one extra accident could be the straw that breaks the camel's back, leading to a more substantial increase. It's the cumulative effect, like a game of Jenga – one wrong move can destabilize the whole tower.

Think about it like this: if your favorite band released a critically acclaimed album every year for a decade, and then one album was a bit… meh, people might forgive it. But if they’ve had a string of less-than-stellar albums, that “meh” one would feel like a nail in the coffin of their creative peak. Your insurance company is kind of like your most loyal, but also most critical, fan.

The 'How Much' Question: A Range of Possibilities

Okay, so you want numbers. I get it. While a precise figure is elusive, we can talk in general terms. For a minor, at-fault accident, you might see an increase of anywhere from 10% to 25%. This could translate to a few hundred dollars more per year, depending on your current premium. It's like finding out your favorite coffee shop is raising prices by 50 cents – annoying, but not exactly life-altering.

For a more serious, at-fault accident, especially one involving significant damage or injuries, the increase can be much steeper. We're talking 50% or even more. In extreme cases, some insurers might even consider you too high a risk to insure and could non-renew your policy. That's when you might need to explore the world of non-standard auto insurance, which can be a bit like shopping for a bespoke suit – more expensive, but you can usually find something that fits.

A cool anecdote: Did you know that some insurance companies offer a "claims forgiveness" program? This is often reserved for drivers with a long history of safe driving. If you qualify, your first at-fault accident might not impact your rates at all. It's like getting a free pass, a golden ticket to insurance tranquility. Definitely worth looking into if you've been a model driver!

Navigating the Post-Accident Landscape

So, what can you do to mitigate the damage, both to your car and your wallet? Firstly, understand your policy. Know your deductibles, your coverage limits, and any specific clauses related to accidents. It’s like knowing the cheat codes to a video game – it gives you an advantage.

Secondly, shop around. After an accident, your current insurer might not be your best friend anymore in terms of price. Don't be afraid to get quotes from other insurance companies. Prices can vary wildly, and a little bit of research can save you a significant amount of money. Think of it as a treasure hunt for better rates, and the treasure is saved cash!

Thirdly, consider raising your deductible. If you're confident you won't have another at-fault accident in the near future, a higher deductible can lower your premium. Just make sure you can actually afford to pay that deductible if the worst-case scenario unfolds. It's a trade-off, a calculated risk, much like choosing the spicier option on the menu – potentially more rewarding, but with a higher risk of… well, consequences.

And here's a pro-tip: If the accident wasn't your fault, make sure your insurance company has all the documentation to prove it. Police reports, witness statements, and photos can be your allies in ensuring your rates don't unjustly skyrocket. Be your own insurance advocate! It’s like being the detective in a mystery novel, piecing together the clues to get to the truth.

When Accidents Become a Habit (Not a Good Habit!)

What if you have a string of accidents? This is where things get serious. Multiple at-fault accidents can lead to your insurer non-renewing your policy. This is their polite way of saying, "We're not comfortable insuring you anymore."

If this happens, you'll need to look into the high-risk insurance market. These policies are designed for drivers with less-than-stellar records. They come with higher premiums, but they ensure you're legally covered. It’s a bit like buying a premium subscription for something that used to be free – you’re paying for the privilege of being insured.

A fascinating tidbit: Some jurisdictions have assigned risk pools or state-run insurance plans for drivers who can't obtain coverage elsewhere. These are often referred to as "assigned risk plans" or "residual markets." They're a safety net, but not necessarily a comfortable one. Think of it as the last resort resort – you're getting a room, but it might not have a view.

The Long Game: Rebuilding Your Insurance Reputation

The good news is that accidents don't last forever on your record. In most places, at-fault accidents will impact your rates for about three to five years. After that, their influence wanes. This is your chance to prove yourself again. Drive safely, obey traffic laws, and avoid any further incidents.

Over time, your driving record will clean up, and your premiums will likely start to decrease. It’s a marathon, not a sprint, when it comes to your insurance standing. Focus on being a consistently good driver, and eventually, the system will recognize your efforts.

It's like that time you tried that new, incredibly difficult recipe, and it was a disaster. But you didn't give up. You practiced, learned from your mistakes, and eventually, you mastered it. Your driving record is similar. A stumble doesn't define the entire culinary journey. Keep practicing good driving habits, and you'll get back to a place of insurance equilibrium.

A Moment of Reflection

Ultimately, the cost of an accident isn't just about the insurance premium hike. It’s about the inconvenience, the stress, and the potential for a much bigger financial hit if things go wrong. It’s a stark reminder that while we may feel invincible on the road, we're all just human, susceptible to the unpredictable nature of life.

So, next time you’re behind the wheel, take a deep breath. Put down the phone. Enjoy the music. And remember that a few extra dollars on your insurance bill is a small price to pay for arriving safely at your destination. The road is a shared space, and a little bit of mindfulness goes a long way, not just for your wallet, but for everyone on that asphalt adventure with you. It’s the simple stuff, the everyday decisions, that truly shape our journey, on and off the road.