How Much Does My Insurance Increase After An Accident: Price/cost Details & What To Expect

Buckle up, buttercups! We're diving into a topic that might sound a little scary, but trust us, it's more of a rollercoaster than a doom-and-gloom lecture. We're talking about that age-old question: what happens to your car insurance bill after a fender bender? It's like a secret society of numbers, and we're about to spill the beans!

So, you had a little mishap. Maybe it was a rogue shopping cart, a momentary lapse in concentration, or perhaps a squirrel staged a daring raid on your windshield. Whatever the cause, the aftermath can leave you wondering about the magic that happens behind the scenes at your insurance company. Does a tiny bump turn your premium into a mountainous beast?

Let's be honest, nobody enjoys thinking about their insurance rates going up. It's like finding out your favorite snack has been discontinued. But knowledge is power, and understanding how these things work can actually be… dare we say… empowering?

The Great Insurance Rate Reveal: What's Really Going On?

When you have an accident, your insurance company has to do a little bit of math. It's not rocket science, but it can feel like it when your wallet's involved! They look at a bunch of things to figure out if your "risk factor" has changed.

Think of it like this: you're a student, and your insurance company is your teacher. You've been a pretty good student, getting good grades (meaning, no accidents). But then, oops, you had a little slip-up (the accident). The teacher needs to decide if this one slip-up means you're now a "riskier" student who might need more supervision (higher premium).

The big question is: how much does that slip-up cost you? It’s the million-dollar question, or perhaps the thousand-dollar question for many!

The Price Tag: It's Not a One-Size-Fits-All Deal!

Here's where things get interesting, and where the mystery truly begins. There's no magic calculator that spits out a universal price increase. It's more like a recipe with a bunch of ingredients, and the final taste can vary wildly!

The amount your insurance goes up after an accident is a complex dance. It's influenced by a whole orchestra of factors. Your insurance company is like a detective, piecing together clues to assess your future driving behavior.

It's not just about the dollar amount of the damage. Oh no, that would be too simple! There are many other whispers in the wind that affect your premium.

Let's talk about fault. This is a HUGE one! Were you the driver who caused the accident? If so, the impact on your premium is likely to be more significant. It's like getting a detention for breaking a rule.

If the other driver was at fault, your insurance company might try to recover some of the costs from their insurer. This can sometimes soften the blow on your rates, but not always. It’s like the teacher understanding that someone else initiated the mischief.

Then there's the severity of the accident. A minor fender bender where only a bumper needs a little TLC is a different story than a multi-car pile-up involving significant injuries. Think of it as the difference between a scraped knee and a broken bone – both hurt, but one requires a bit more serious intervention.

The cost of repairs is also a major player. If the damage is extensive and costly to fix, your insurance company sees a bigger payout. This naturally leads them to believe you might be a riskier prospect in the future.

And let's not forget the type of coverage you have. Collision coverage is designed for this very scenario, and using it will likely have a bigger impact than if it were a claim under a different part of your policy.

Here’s a fun tidbit: your driving record is like your permanent report card. If you've been a model driver for years with a spotless record, one accident might not sting as much. But if you already have a few dings on your record, that new accident can feel like the final straw.

And believe it or not, your location can even play a role. Areas with higher rates of accidents or claims might see larger increases across the board. It’s like living in a neighborhood where everyone seems to be getting speeding tickets!

What to Expect: The Waiting Game and the Dreaded Bill

So, you've reported the accident. Now what? You enter the waiting game. Your insurance company will investigate, assess the damage, and determine fault. This can take anywhere from a few days to a few weeks, depending on the complexity of the situation.

Once they've got all their ducks in a row, you'll typically receive a notification. This might be a letter, an email, or even a call from your agent. It's the moment of truth, the grand reveal of your new premium!

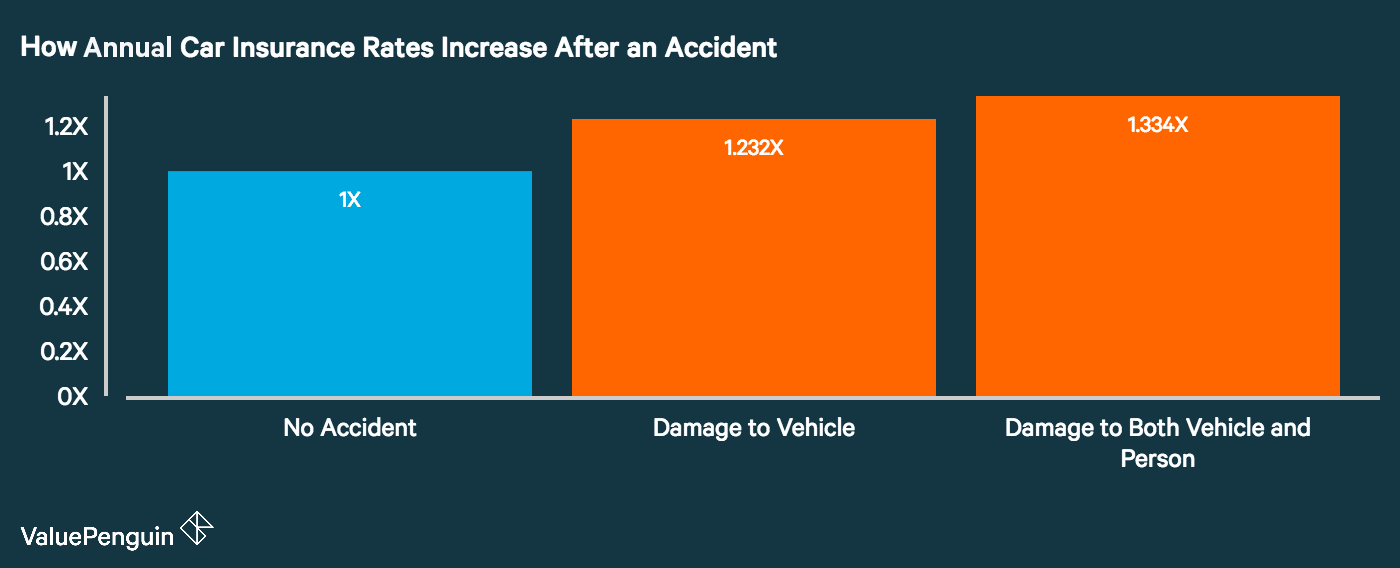

Generally, you can expect an increase. The question is, how much? Experts often cite figures ranging from 20% to 50% or even more after an at-fault accident. But remember, this is just an average, a ballpark figure. Your actual increase could be lower or higher.

For a minor at-fault accident, you might see an increase of a few hundred dollars per year. For more serious incidents, it could be significantly more. It’s like a surprise party – sometimes it’s a small gathering, other times it’s a full-blown bash!

The good news? Not all accidents are created equal. If you're not at fault, the impact on your rates might be minimal, or even non-existent, especially if your insurer can recover costs from the other party's insurance.

It’s also important to note that some insurance companies offer a "claims forgiveness" policy. This is like a get-out-of-jail-free card for your first accident! If you have this, your rates might not go up at all. Definitely something to ask your insurance agent about!

Making Sense of the Numbers: Where to Get the Inside Scoop

If you’re feeling a bit bewildered by all this, you’re not alone! The best thing you can do is to talk to your insurance agent. They are your guides through this sometimes-confusing landscape.

Your agent can explain exactly why your premium has changed and what factors contributed to the increase. They can also discuss options with you, like potential discounts you might be eligible for or different coverage levels.

Don't be afraid to shop around! Even if you have a great relationship with your current insurer, it never hurts to get quotes from other companies. A little comparison shopping could save you a significant amount of money, especially after an accident.

Remember, an accident is a bump in the road, not the end of your insurance journey. By understanding the factors that influence your rates, you can be better prepared and make informed decisions. It’s all about navigating the twists and turns of the road, and sometimes, that means adjusting your speed and your budget!

So, the next time you hear about an accident, don't just think "ouch!" Think about the intricate web of calculations and the fascinating, albeit sometimes costly, process that insurance companies undertake. It's a world of numbers, risk, and ultimately, trying to keep you safe and sound on the road. And who knows, maybe understanding it all will make that premium increase a little less painful!