How To Calculate Value Of Shares In A Private Company

Hey there, future financial wizard! So, you've got a stake in a private company, huh? That's pretty cool! It's like having a secret recipe for awesomeness, and unlike those publicly traded stocks that are plastered all over the news (and sometimes give us more anxiety than a surprise pop quiz), private company shares are a bit more… mysterious. But don't worry, figuring out their value isn't rocket science, though it might feel like navigating a jungle gym sometimes. We're going to break it down in a way that's as easy as pie (and hopefully, just as sweet when you see that number!).

First things first, why bother calculating the value of these elusive shares? Well, maybe you're thinking about selling a few, bringing on new investors, or perhaps you're just plain curious. Whatever the reason, knowing what your piece of the pie is worth is pretty darn important. It's like knowing how many sprinkles you've got for your ice cream – crucial for maximum enjoyment!

Now, unlike public companies where you can just hop on Google Finance and see the stock price fluctuating faster than your mood swings on a Monday, private companies don't have a ticker symbol. No handy-dandy charts here! This means we've got to do a little more digging. Think of it like being a detective, but instead of a magnifying glass, you've got spreadsheets and financial statements. Pretty exciting, right?

Let's dive into the nitty-gritty, but we'll keep it light, I promise. We’re not aiming for a finance degree here, just a good understanding. So, grab your favorite beverage, maybe a cookie or two, and let's get this valuation party started!

The Big Picture: Why is it Tricky?

Okay, so why is valuing private company shares a bit like trying to catch a greased pig? Well, there are a few key reasons:

Lack of Market Transparency: This is the big one. Public companies have a constant stream of buyers and sellers, setting a price for their shares daily. For private companies, transactions are few and far between, and often happen behind closed doors. It's like trying to find the going rate for a unicorn – not exactly readily available information!

Information Asymmetry: Sometimes, the people running the company know a lot more about its inner workings than an outsider (or even a minority shareholder). This can make it harder to get a truly objective picture of the company's worth.

Illiquidity: Selling shares in a private company can be a lot harder than selling stock on the open market. You can't just click a button and have cash in your account tomorrow. This lack of easy access to cash (liquidity) can affect the valuation.

Control Premiums: If you're buying a significant chunk of a private company, you might be paying a bit extra because you'll have more control. This is called a "control premium," and it's not something you see with public stocks, where you’re just a tiny drop in a very big ocean.

But fear not! Despite these hurdles, we have ways of making you value!

Method 1: The "Look at What Others Paid" Approach (Comparables)

This is probably the most intuitive way to start. You look at similar companies that have recently been bought or sold, or that have raised money. It's like saying, "Well, Brenda down the street sold her amazing cookie business for $10,000, and my cookie business is pretty darn similar, so mine must be worth around that!"

Public Company Comparables (Public Comps)

This involves looking at publicly traded companies that are in the same industry and have a similar business model. We then use their valuation multiples (like how much investors are willing to pay for each dollar of revenue or profit) and apply them to your private company.

How it works:

- Identify Similar Public Companies: Find companies that do what yours does, are roughly the same size, and operate in the same geographical areas.

- Gather Financial Data: Get their revenue, earnings (profit), and market capitalization (total value of all their shares).

- Calculate Multiples: This is where the magic happens! Common multiples include:

- Price-to-Earnings (P/E) Ratio: Market Cap / Net Income. This tells you how much investors are willing to pay for each dollar of earnings.

- Price-to-Sales (P/S) Ratio: Market Cap / Revenue. Useful for companies that aren't yet profitable.

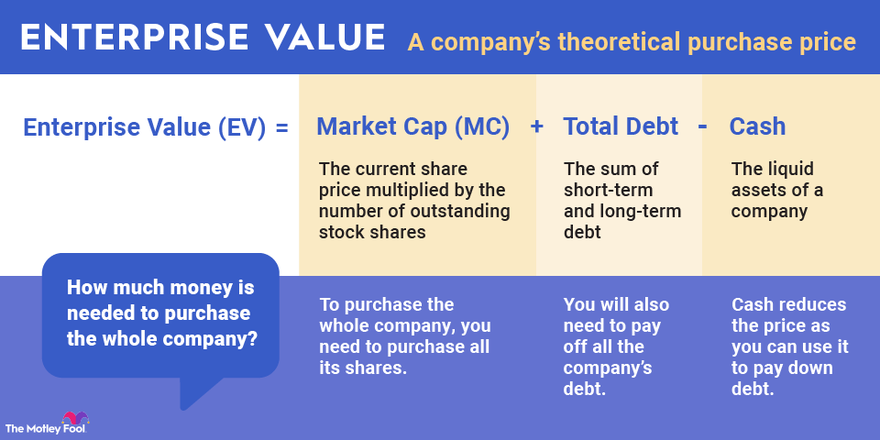

- Enterprise Value (EV) to EBITDA: EV is a broader measure of value than market cap. EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) is a measure of operating performance.

- Apply to Your Company: Take the average multiple from the comparable public companies and multiply it by your private company's relevant financial metric (e.g., net income, revenue).

Example Time (for fun!): Let's say you have a fantastic artisanal dog treat company. You find three public dog food companies whose P/E ratios are 20x, 25x, and 22x. The average is 22.33x. If your dog treat company made $100,000 in net profit last year, you might say your company is worth approximately $100,000 * 22.33 = $2,233,000. Ta-da! (Remember, this is a simplified example. Real-world valuations are more complex.)

The Catch: Public companies are generally much larger and more mature than private companies. Also, they're subject to more scrutiny and regulations, which can affect their valuations. So, you need to adjust for these differences. It's like comparing a fancy, Michelin-starred restaurant to your favorite cozy diner – both serve food, but the expectations and prices are different!

Precedent Transactions (M&A Comps)

This is similar to public comps, but instead of looking at ongoing public companies, you're looking at actual deals where similar private companies were bought or sold. This can be more relevant because you're comparing apples to apples (or at least, slightly less bruised apples).

How it works:

- Find Recent Acquisition Data: Search for news and databases that track mergers and acquisitions of companies in your sector.

- Identify Similar Transactions: Look for deals involving companies with similar size, business models, growth rates, and profitability.

- Extract Valuation Multiples: See what multiples (revenue multiples, EBITDA multiples, etc.) were paid in those transactions.

- Apply to Your Company: Use these multiples to estimate your company's value.

The Challenge: Finding reliable data on private company transactions can be tough. It's often not publicly disclosed. You might need to consult with valuation professionals or use specialized databases.

Method 2: The "What Will It Earn in the Future?" Approach (Discounted Cash Flow - DCF)

This method is all about looking into the crystal ball… or rather, projecting your company's future cash flows and discounting them back to today's value. It's a more in-depth approach that focuses on the company's intrinsic earning power.

The Core Idea

Money today is worth more than money tomorrow, right? Because you could invest that money today and earn a return. The DCF method accounts for this by "discounting" future cash flows to their present value. Think of it as finding out how much a promise of future ice cream is worth in chocolate coins right now.

How it Works (The Slightly More Technical Bits)

- Project Future Free Cash Flows: This is the most critical step. You need to forecast how much cash the company will generate each year for a certain period (e.g., 5-10 years). This involves a lot of assumptions about revenue growth, expenses, capital expenditures, and working capital changes. You're basically creating a detailed financial roadmap.

- Estimate a Terminal Value: Since you can't project forever, you need to estimate the value of the company beyond your explicit forecast period. This is often done using a perpetual growth model or an exit multiple.

- Determine the Discount Rate: This is the rate of return investors expect to earn on an investment of similar risk. For companies, this is often the Weighted Average Cost of Capital (WACC), which blends the cost of debt and equity. A higher discount rate means future cash flows are worth less today.

- Discount Future Cash Flows: Apply the discount rate to each year's projected free cash flow and the terminal value to arrive at their present values.

- Sum Them Up: Add up all the present values of the future cash flows and the terminal value. This gives you the estimated enterprise value of the company.

- Adjust for Debt and Cash: Subtract any outstanding debt and add any cash to get the equity value.

- Calculate Per-Share Value: Divide the total equity value by the number of outstanding shares.

The Pros: This method is considered very robust because it focuses on the company's ability to generate cash, which is the ultimate source of value. It's also forward-looking.

The Cons: It's heavily reliant on assumptions. A small change in your growth rate or discount rate can lead to a big difference in the final valuation. It's like predicting the weather – you can make a good guess, but it might still rain on your parade!

Method 3: The "What Are Its Assets Worth?" Approach (Asset-Based Valuation)

This method looks at the value of the company's tangible and intangible assets. It's like saying, "Okay, if we sold off all the furniture, computers, patents, and goodwill, what would we get?"

Tangible vs. Intangible Assets

Tangible assets are things you can touch: buildings, machinery, inventory, cash. You can often get a pretty good idea of their market value through appraisals or by looking at recent sales of similar assets.

Intangible assets are less concrete: brand recognition, patents, customer lists, software, goodwill. Valuing these is trickier and often involves looking at the income they generate or what someone would pay to acquire them.

How it Works (Simplified)

- Identify All Assets: List everything the company owns.

- Determine Fair Market Value: Appraise each asset to figure out what it would sell for in a hypothetical sale.

- Subtract Liabilities: Deduct all the company's debts and obligations.

- The Remainder is Your Value: What's left is the value of the company based on its assets.

When is this method best? This method is often used for companies that have a lot of physical assets, like manufacturing companies, or for companies that are struggling or being liquidated. It's less common for fast-growing tech companies that rely more on intellectual property and future earnings.

The Caveat: This method often undervalues a going concern because it doesn't capture the value of a well-run business that generates profits over and above its asset value. It's like valuing a cake based on the cost of the flour and sugar, without considering the baker's skill and the delicious final product!

Method 4: The "How Much Profit Did We Make?" Approach (Earnings Multiples)

This is a more direct cousin of the public comps method, but we're focusing solely on your company's own earnings or revenue. It's a quick and dirty way to get a ballpark figure.

The Simple Math

You take a measure of your company's performance (like net profit, EBITDA, or revenue) and multiply it by a "multiple." This multiple is derived from industry benchmarks, historical performance, or what similar companies have been valued at.

Example: If your company made $200,000 in net profit last year, and the industry average earnings multiple is 5x, your company might be worth $200,000 * 5 = $1,000,000. Easy peasy, right?

The Challenges: The biggest challenge is choosing the right multiple. A slightly off multiple can lead to a wildly inaccurate valuation. It also doesn't account for future growth or specific company risks as well as other methods.

Other Factors to Consider (The Secret Sauce!)

Beyond the numbers, a few other things can sway the value of your private company shares:

- Stage of the Company: Is it a fledgling startup or a mature business? Startups are riskier but have higher growth potential.

- Management Team: A stellar team can significantly boost a company's perceived value. People invest in people!

- Market Conditions: Is the overall economy booming or busting? Is your industry hot or not?

- Customer Concentration: If 90% of your revenue comes from one client, that's a risk!

- Intellectual Property: Strong patents or proprietary technology can be a huge asset.

- Synergies: If someone is buying your company, they might see ways to combine operations and save money, which they'll factor into their offer.

Putting It All Together: It's Not One-Size-Fits-All

Here's the thing: there's no single "correct" way to value a private company. Often, professionals will use a combination of these methods to arrive at a valuation range. They'll triangulate the results, like a financial GPS finding the best route.

It's also crucial to remember that valuation is subjective, especially for private companies. What one person thinks your shares are worth, another might see differently. This is where negotiation and professional advice come into play.

When to Call in the Pros

If you're dealing with a significant transaction, like raising a large round of funding, selling your stake, or merging with another company, it's often worth hiring a professional business valuation expert. They have the experience, tools, and objectivity to give you a reliable valuation. Think of them as the seasoned detectives who can crack the toughest cases!

The Sweetest Part: What Your Shares Are Really Worth to YOU

So, after all that number crunching and head-scratching, you've got a figure (or a range of figures). But remember, the "value" of your shares isn't just a number on a spreadsheet. It's a reflection of the hard work, innovation, and passion that has gone into building this company. It's the potential for future growth, the impact it makes, and the opportunities it creates.

Whether it's a booming tech startup, a charming local business, or a company with a truly game-changing idea, your shares represent a piece of something special. So, take a moment, pat yourself on the back, and smile. You've navigated the wonderful world of private company valuations, and that, my friend, is pretty darn impressive. Go forth and be awesome!