How To Get Out Of Car Finance With Negative Equity

So, you’ve got a car. Awesome, right? But what if that car owes you more than it’s worth? Yup, we’re talking negative equity. It’s like owing your best friend for a pizza you already ate… and then some. Sounds a bit sticky, doesn’t it?

Don’t panic! This isn’t the end of your automotive dreams. In fact, it’s kind of a fun little puzzle to solve. Who doesn't love a good financial challenge? It's like a real-life video game, but with less annoying loading screens and more actual money involved. Plus, understanding this stuff makes you sound super smart at parties. Guaranteed.

Think of your car as a fancy, depreciating tech gadget. The moment you drive it off the lot, poof, its value starts its epic descent. It's a bit like a banana on a hot day. Delicious at first, but its prime is fleeting. And when that banana's value is less than what you owe on it? That's your negative equity.

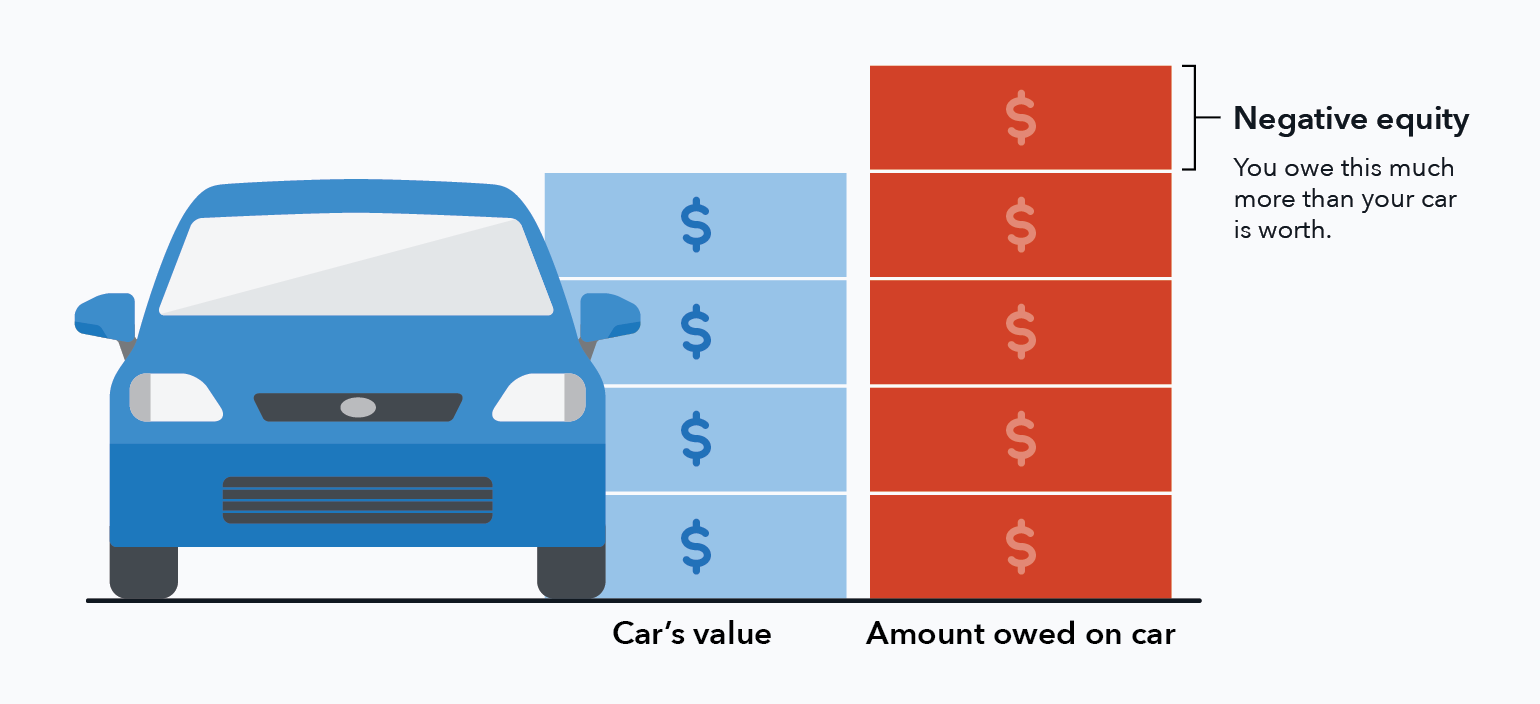

So, What Exactly IS Negative Equity?

Simple! You owe more on your car loan than the car is currently worth. Let's say you bought a car for $25,000 and financed the whole thing. A year later, the market says your car is only worth $18,000. You still owe, let’s say, $20,000 on that loan. That's a $2,000 gap. That's your negative equity. That $2,000 is just… floating out there, like a ghost of a past financial decision.

It’s a bit like owning a rare Beanie Baby. You thought it was the next big thing, but the market has moved on. Except, you can’t exactly cash in a slightly beat-up Honda Civic for a fortune. Unless it’s really beat up and you’re selling it for scrap, which is probably not the goal here.

This happens most often when you buy a new car. They lose a chunk of their value instantly. Like, blink and you’ll miss it. Some cars depreciate faster than others. Ever seen a flashy sports car from ten years ago? Probably worth way less than its original sticker price, even if it’s in mint condition. That’s the depreciation beast at work.

Why Is This Even a Thing to Talk About?

Because cars are expensive! And sometimes, life happens. You need a new car, and maybe you didn't get the best loan terms. Or perhaps you rolled negative equity from a previous car into your current one. It's a common financial kink, like a stubborn cat that won't budge from its favorite sunbeam. And knowing how to untangle it is pretty darn useful.

It’s also just… interesting! The mechanics of it, the market forces, the psychology of buying a car. We attach so much to our cars, don’t we? Freedom, status, a place to sing badly to the radio. So, when they don't hold their value, it feels like a personal slight.

Getting Out of the Negative Equity Funk

Okay, deep breaths. We’re not going to pretend this is as easy as finding a twenty-dollar bill in your old jeans. But it’s definitely doable. Think of it as a fun financial scavenger hunt!

Option 1: The Long Haul (AKA, Just Keep Paying)

This is the most straightforward. Just keep making your car payments. Over time, you’ll pay down the loan. Eventually, you’ll owe less than the car is worth. It’s like slowly chipping away at a mountain. Eventually, you’ll reach the peak. Or, you know, a point where the car’s value catches up to the loan balance.

The downside? It takes time. And during that time, if you really need to sell your car, you'll have to cover that negative equity gap yourself. That’s the part that stings. It’s like having a delicious donut in front of you, but you can only eat half of it. Sad.

Quirky fact: Some people actually find satisfaction in this. They see it as a personal victory, conquering their debt one payment at a time. It’s like a very slow, very expensive marathon.

Option 2: The Smart Trader-Upper

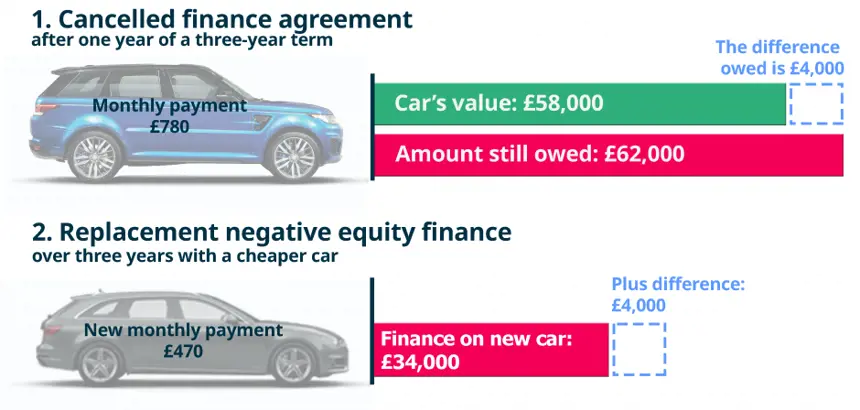

You want a new car? Or maybe just a different car? When you trade in your current car, the dealership will offer you its market value. If that’s less than what you owe, they’ll roll that negative equity into your new car loan. This is where things can get… interesting. And potentially more expensive in the long run.

It’s like putting all your laundry into one giant load. Easier in the moment, but it can get complicated. You're essentially borrowing even more money. So, while it gets you out of the old car, it doesn’t magically fix the negative equity problem.

Pro tip: Try to put down a significant down payment on your next car. This helps offset any negative equity you might be carrying. A bigger down payment is like a force field against financial woes.

Option 3: The Side Hustle Hero

Want to speed things up? You need to make extra cash. This is where the fun really begins! Think outside the box. Can you sell some stuff you don't need? That collection of novelty teacups? That slightly questionable art from your college days? Every little bit helps.

Gig economy, anyone? Driving for a ride-sharing service? Delivering food? Freelance writing? Knitting custom cozies for squirrels? (Okay, maybe not that last one, but you get the idea!) The more extra money you make, the faster you can chip away at that negative equity. It’s like leveling up in a game, but with real-world rewards!

This approach lets you keep your current car while you attack the debt. It’s a targeted strike. You’re not just hoping for the best; you’re actively making it happen. Plus, learning new skills or picking up a fun hobby can be a bonus.

Option 4: The Sell-It-Yourself Savior

This is for the brave! Selling your car yourself on platforms like Craigslist or Facebook Marketplace often nets you a higher price than a dealership. This is where you can potentially get closer to the car’s actual market value, or even more if you’re a good negotiator.

But here’s the catch: if you owe more than you sell it for, you still have to pay the difference out of pocket. This is the "pay the gap" scenario. It's like selling a slightly used, but still valuable, piece of art. You might not get back what you paid, but you’re trying to get the best possible price.

This method requires effort. Photos, descriptions, meeting potential buyers, dealing with lowball offers. It’s a mini-business venture. But if you’re good at it, you can definitely reduce or even eliminate that negative equity!

Option 5: The Refinance Ranger

Sometimes, you can refinance your car loan. If your credit has improved, or if interest rates have dropped, you might qualify for a loan with better terms. This could lower your monthly payments, freeing up cash to put towards the principal. It’s like giving your loan a makeover.

This won’t magically eliminate negative equity on its own, but it can make it easier to manage. It’s a helpful tool in your arsenal. Think of it as getting a smoother ride for your financial journey.

The Bottom Line: Be Proactive!

Getting out of negative equity isn't always fun, but it's definitely empowering. It’s about taking control of your finances and making smart choices. Don't let that car debt drive you crazy!

Remember, your car is a tool. It’s there to get you places. It doesn’t need to be a financial albatross around your neck. So, explore these options. Talk to your lender. Get creative. You’ve got this!

And hey, at least you're not dealing with negative equity on a pet rock. That would be truly bizarre. Happy driving (and managing your money)!