How To Hide Savings From Benefits On Universal Credit

Hey there, lovely people! So, let's dive into a topic that’s a little bit juicy, a little bit practical, and definitely something many of us have pondered: navigating the world of Universal Credit and the ever-present question of what happens when you’ve managed to squirrel away a few quid. We're not talking about moonlighting as a secret agent or anything, just the smart, everyday ways you might build up a little financial cushion without causing a stir.

Think of it like this: you’re juggling a dozen things, just like that TikTok trend where someone tries to keep multiple plates spinning. You’re managing your budget, dealing with life’s curveballs, and maybe, just maybe, you've managed to trim the fat here and there, finding a few extra pounds that haven't disappeared into the ether. It’s about financial savvy, plain and simple. And in today’s world, who isn’t looking for a little bit more control over their destiny?

The Universal Credit Balancing Act

Universal Credit (UC) is designed to be a safety net, a support system. And it’s brilliant for that! But it also comes with its own set of rules, and one of those is the capital limit. If your savings – or the value of certain assets – go above a certain threshold, your UC payments can be reduced or even stopped. It’s like a dimmer switch for your benefits, and nobody wants their light suddenly dimmed, right?

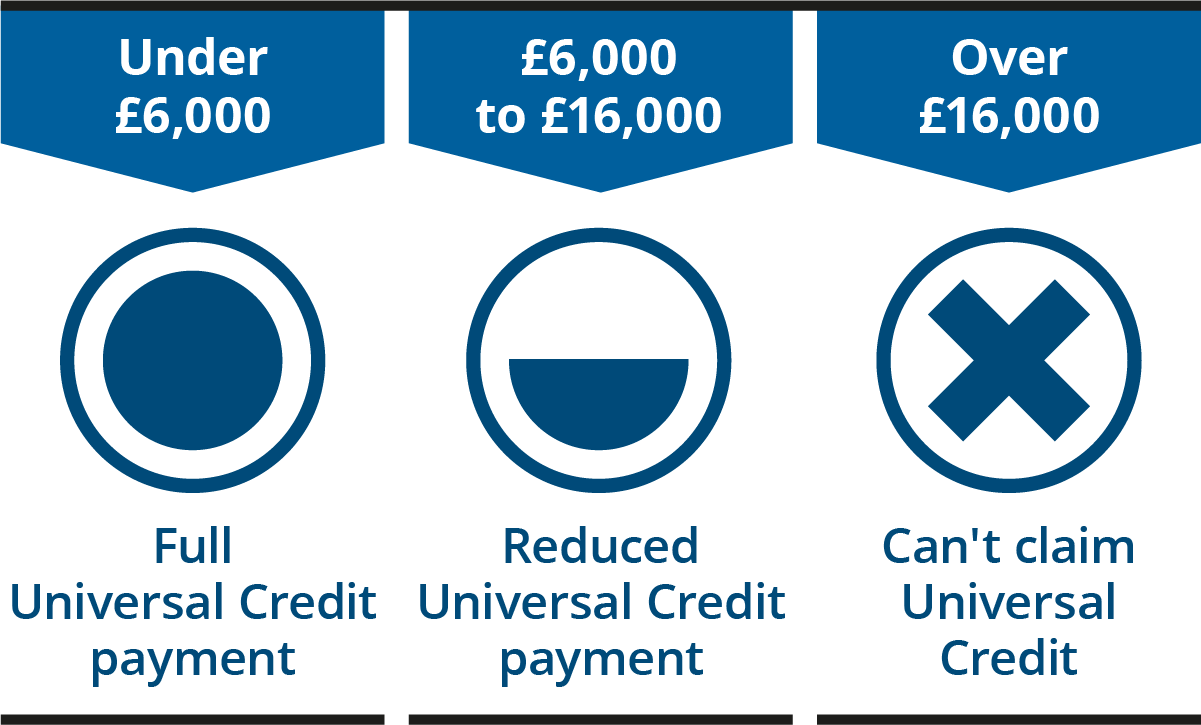

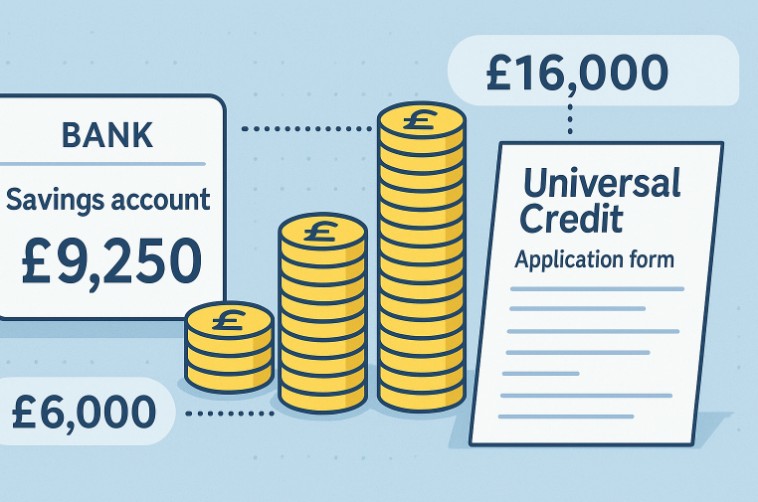

The current capital limit is £6,000 for a reduced rate of UC, and £16,000 for no UC at all. This isn't a small amount of money for many, but for others, life circumstances can lead to a bit more accumulating. It's a bit like that moment when you realize you've accidentally bought way too many houseplants – suddenly, you've got more than you bargained for!

So, what does this mean in practice? If you’ve managed to save up, say, £7,000, your UC payment will be reduced. If you’re sitting pretty on £17,000, your UC will likely stop entirely. It’s not a punishment; it’s how the system is designed to work. The idea is that if you have significant savings, you're expected to use them to support yourself.

Decoding the Capital Limit: What Counts and What Doesn't?

This is where it gets a bit like a game of "spot the difference." Not all your money is treated the same way. Understanding this is key to navigating the system without any unnecessary headaches. Think of it as knowing the cheat codes for a video game – suddenly, things become much more manageable!

Generally, your savings in bank accounts – current accounts, savings accounts, ISAs – count towards the capital limit. This is the straightforward stuff, like the obvious choices in a game of Jenga. But there are some exceptions, some secret passages, if you will.

For instance, certain types of pensions usually don't count. Your state pension, for example, is in a different category. Also, if you have money tied up in certain investments that you can't easily access, like some types of trusts, these might be treated differently. It’s always worth getting the most up-to-date information, as rules can change like the weather in a British summer.

Smart Savings Strategies: The Art of Stealth

Okay, so you've got a bit more than the limit allows, or you're on the cusp. What are some of the more… discreet ways to manage your finances? We’re talking about the everyday hustle, the little wins that add up, not about anything dodgy. This is about being a bit clever with your money, like a squirrel burying nuts for winter, but a much more sophisticated, latte-sipping squirrel.

The Power of "Under the Mattress" (But Not Literally!)

Let’s be honest, the idea of cash under the mattress might sound old-fashioned, a bit like dial-up internet. But the principle behind it – having physical cash that isn't in a declared financial institution – is something the Department for Work and Pensions (DWP) doesn't have a direct line to. This isn’t about hoarding a huge wodge of cash and hoping no one notices; that would be a whole other kettle of fish.

Instead, consider this: if you've been diligent with budgeting, maybe you've been receiving cash back from shops, or perhaps you have a side hustle that pays in cash. Instead of immediately banking it all, you might choose to keep a reasonable amount of cash at home for everyday expenses or small, unforeseen needs. This is about having a small float, a buffer. Think of it as your personal emergency stash, like having a secret chocolate bar in your bag for when the day gets rough.

The key here is proportion. If you’re keeping £10,000 in cash at home, that’s going to raise eyebrows and could be flagged as undeclared wealth. But keeping a few hundred pounds for immediate needs? That’s just being prepared. It’s like having a spare tyre in your car – essential for peace of mind.

The "Little and Often" Withdrawal Tactic

This is where a bit of planning comes in. If you find yourself consistently above the capital limit, or you’re anticipating a deposit that will push you over, consider withdrawing funds in small amounts over time. Again, we’re not talking about massive, suspicious transfers. We’re talking about gradually reducing your declared savings.

Imagine you have £10,000 in savings and you know the limit is £6,000. Instead of leaving it all there and seeing your UC drop, you could plan to withdraw £200 each month for a few months. This money can then be spent on everyday expenses, or perhaps used to pay off small debts, or even just kept as physical cash at home for the reasons we discussed. It’s a slow and steady approach, like tending a bonsai tree – it requires patience and a gentle touch.

This strategy ensures that your declared savings gradually dip below the threshold, making you eligible for your full UC entitlement again. It's a way of proactively managing your financial situation within the system's parameters.

The Magic of "Gifting" (With Caveats!)

This is a more advanced manoeuvre, and it comes with significant warnings. If you have assets that you don’t need and want to reduce your capital, you can, in theory, give them away. However, this is where the DWP gets particularly attentive.

There are strict rules around "deprivation of capital." If you’re found to have intentionally given away money or assets to reduce your capital and therefore receive benefits you wouldn’t otherwise be entitled to, this can be treated as if you still have that money. It’s like trying to hide a present from someone and then claiming you don’t have it – they’ll probably guess!

So, if you’re considering gifting, it needs to be done with genuine intent and well in advance of needing benefits. For example, if you're fortunate enough to have a substantial inheritance or savings and want to help out family members or make charitable donations, doing so months or even years before you might need to claim UC is the safest approach. Think of it like planting a tree – you don’t expect fruit the next day.

Crucially, if you are gifting a large amount, it’s highly recommended to seek independent financial advice. This isn't a trick or a loophole; it’s about responsible financial planning for people who are in a fortunate position to give. For most people navigating UC, this is probably not a relevant strategy, but it’s good to be aware of the possibilities and the significant pitfalls.

The Power of Accessible "Non-Liquid" Assets

What about things that aren't just sitting in a bank account? Think about assets like a car. Generally, the value of a car doesn't count towards your capital limit for Universal Credit, unless it's a second car or a vehicle that's not essential for your mobility needs.

So, if you have a reliable car that you use daily for commuting, shopping, or essential appointments, its value is usually disregarded. This is a huge relief for many! It means you can have a perfectly decent car without it impacting your UC. It's like having a superpower that’s completely legal!

However, if you have, say, a classic car that’s more of a hobby or an investment, or a second vehicle sitting unused, that could be viewed differently. The DWP will look at whether the asset is essential or provides significant benefit to your household.

Similarly, some investments, particularly those that are difficult to sell quickly or have significant penalties for early withdrawal, might be treated more favourably. Again, this is a complex area, and the specifics can vary. It’s always best to be transparent with the DWP about any significant assets you hold, and they will advise you on how they are treated.

The "Future You" Fund: Pension Planning

As mentioned earlier, most pension pots are exempt from the UC capital limit. This is a fantastic incentive to save for retirement. So, if you have the opportunity to contribute to a private pension, whether through an employer or as a personal pension, this is a really effective way to build up savings that won’t affect your current UC payments.

Think of it as a superhero move for your future self. You’re building security for later down the line, and in the meantime, you’re not penalised for it on your current benefits. It’s a win-win, like finding an extra biscuit at the bottom of the tin!

This doesn't mean you can just transfer all your savings into a pension tomorrow. Pension rules are complex and there are limits on how much you can contribute tax-efficiently. But for ongoing savings, it’s a brilliant option.

The Importance of Honesty and Transparency

Now, before we get too carried away with stealth tactics, let’s have a little heart-to-heart. The most important thing when dealing with Universal Credit, or any government benefit, is honesty and transparency. The DWP has systems in place to detect undeclared assets and income, and getting caught can lead to serious consequences, including penalties, overpayments, and even prosecution.

These tips are for people who are genuinely trying to manage their finances smartly, within the spirit of the rules. They are about understanding how the system works and making informed decisions about your money. They are not about trying to defraud the system.

If you're unsure about how a specific asset or savings will be treated, the best course of action is always to contact the DWP directly. They have dedicated teams who can provide guidance and clarify the rules for your individual circumstances. It’s always better to ask for clarification than to make a mistake.

Think of it like this: you wouldn't try to guess the ingredients in a complex recipe without looking at the instructions, right? Similarly, don't guess the rules for your benefits. Get the official word!

A Moment of Reflection: Money, Life, and Peace of Mind

In the grand scheme of things, Universal Credit is a vital support for so many people navigating challenging times. It’s there to provide a foundation, a degree of security when life throws its inevitable curveballs. Having a little bit of extra saved, a small cushion, can make a world of difference when unexpected costs arise – a broken-down washing machine, a sudden car repair, or a child’s school trip that you really want them to go on.

It’s about that feeling of having a bit of breathing room, of not being on a knife-edge. It’s about the peace of mind that comes from knowing you can handle a minor emergency without spiralling into debt. It’s the difference between a stressful panic and a manageable hiccup.

Ultimately, these strategies are about empowering yourself. They’re about understanding the system, making smart choices with the resources you have, and building a little bit of financial resilience. It’s about finding that sweet spot where you’re supported, but also building a tiny bit of your own independence, one saved pound at a time. And in our busy, often unpredictable lives, that bit of extra control can feel like a superpower.