Is 3 Good Mortgage Rate

Imagine this: you’re finally ready to snag that dream home, the one with the perfectly manicured lawn and the kitchen island begging for your famous cookies. You’ve saved diligently, navigated the maze of real estate agents, and now you’re staring at this mystical thing called a “mortgage rate.” It’s like a secret handshake into homeownership, and everyone wants to know if they’re getting the best one.

So, the big question pops into your head: is 3% a good mortgage rate? Let’s dive in, shall we? Think of your mortgage rate like the VIP pass to your new house. A lower rate means less of your hard-earned cash goes to the bank, and more stays in your pocket for, you know, that fancy espresso machine you’ve been eyeing.

Now, 3%… sounds pretty neat, right? It’s like finding a twenty-dollar bill in your old jeans. But is it the best? The truth is, the “best” rate is a bit like a unicorn – a beautiful concept, but its exact location can be a little elusive.

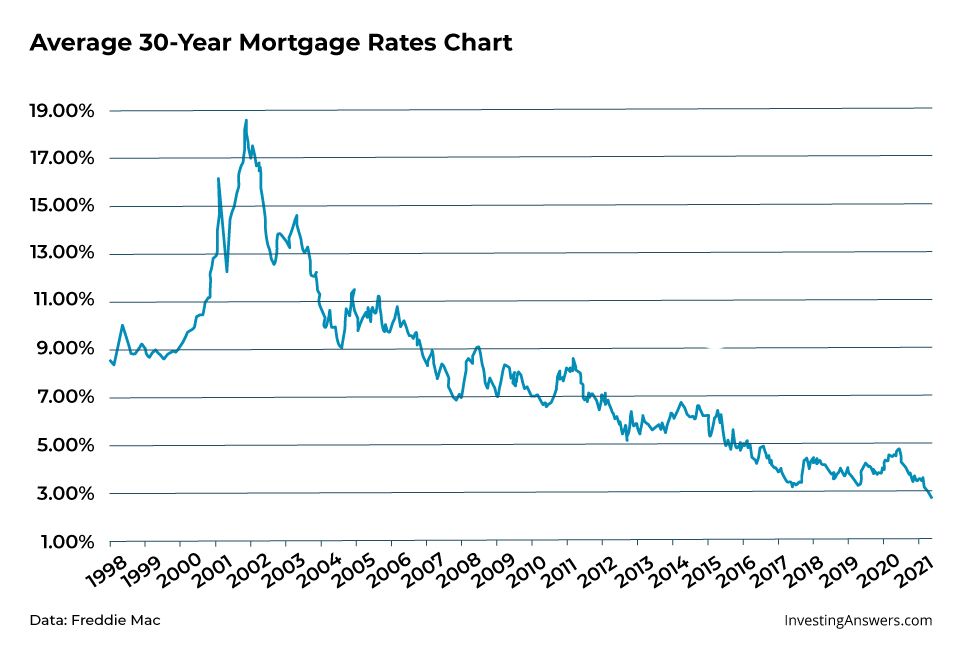

Let’s fast forward a bit, shall we? Picture a world where mortgage rates were, well, a bit more… enthusiastic. We’re talking rates that made your eyes water and your wallet weep. Back in the day, getting a rate that started with a ‘3’ would have been the stuff of legends. People would have broken out the champagne and possibly written folk songs about it.

Think of your grandparents, or maybe even your parents, trying to buy their first home. They might have been looking at rates that made a 3% rate seem like a distant, sunny dream. They might have spent years diligently paying off a loan that felt heavier than a bag of bricks.

So, when we talk about a 3% mortgage rate today, it’s important to remember the context. It’s a rate that, for many, represents a fantastic opportunity. It’s the kind of rate that could make homeownership feel a lot more achievable and a lot less like a financial Everest climb.

But here’s the funny part: the world of mortgages can be a bit like a quirky game of musical chairs. Rates are constantly dancing around, influenced by all sorts of invisible forces. Things like the Federal Reserve, the economy’s mood swings, and even how many people are trying to buy a house can make rates jiggle up and down.

So, while 3% is generally considered a really, really good deal in the grand scheme of things, it’s not the only factor in the homebuying fiesta. It’s like finding a perfectly ripe avocado – fantastic, but you still need to make sure it pairs well with your salsa.

What else matters, you ask? Well, there’s the concept of your credit score. Think of this as your financial report card. A squeaky-clean credit score tells lenders, “Hey, this person is responsible and pays their bills on time!” And because you’re a responsible financial wizard, they’re more likely to offer you a magical 3% rate.

On the flip side, if your credit score is looking a little… less than stellar, that 3% rate might be harder to catch. It’s like trying to get front-row tickets to a sold-out concert with a seat number way in the back.

Then there’s the whole “down payment” thing. This is the chunk of cash you put down upfront. A bigger down payment is like a superhero cape for your mortgage application. It shows you’re serious and reduces the risk for the lender, which, you guessed it, can lead to sweeter interest rates.

Imagine you’re buying a really fancy cake. If you’ve already paid for half of it, the baker (the lender) is going to feel a lot more comfortable letting you take it home, and maybe even offer you a little discount on the remaining frosting.

And let’s not forget the different types of mortgages! You’ve got your fixed-rate mortgages, which are like that steady, reliable friend who always shows up on time. Your monthly payments stay the same, offering a comforting predictability. This can be a real lifesaver when you’re trying to budget for all those new homeowner expenses, like, say, a really enthusiastic garden gnome collection.

Then there are adjustable-rate mortgages (ARMs). These are a bit more adventurous, like a roller coaster. The interest rate can go up or down depending on the market. For some, this is exciting and potentially cheaper if rates fall. For others, it’s a bit of a gamble, and they prefer the peace of mind of a fixed rate.

So, while a 3% rate is undeniably appealing for a fixed-rate mortgage, an ARM might start even lower, making it tempting. But remember that roller coaster analogy? It can go both ways!

Let’s talk about the heartwarming aspect. For so many, a mortgage is the key to building a life, raising a family, and creating memories. It’s not just about bricks and mortar; it’s about planting roots and watching them grow. A lower rate, like a 3% one, can make that dream feel so much more tangible.

Imagine a young couple, working hard, finally able to buy their first home. That 3% rate isn’t just a number; it’s a stepping stone to stability, to backyard barbecues, and to the sound of little feet running through the halls. It’s the difference between feeling overwhelmed by debt and feeling empowered by possibility.

It’s also about the surprising elements. Sometimes, you might think you’re getting the best rate, only to discover a lender you hadn’t even considered is offering something even more spectacular. It’s like finding a hidden gem at a flea market – unexpected and delightful.

The key is to do your homework, shop around, and talk to multiple lenders. Don't be afraid to ask questions, even if they seem silly. The mortgage process can feel like learning a new language, but with a little patience and persistence, you can become fluent!

Ultimately, whether 3% is a “good” mortgage rate depends on your personal circumstances and the current market. But generally speaking, in most recent times, it’s a rate that would make most aspiring homeowners do a little happy dance. It signifies a period where borrowing money to buy a home was relatively affordable, making that dream home a much more attainable reality for many.

So, the next time you hear about mortgage rates, remember that 3% is a number that carries a lot of weight, a lot of hope, and a lot of potential for building a wonderful future. It’s a number that can turn a house into a cherished home, and that, my friends, is pretty darn good.