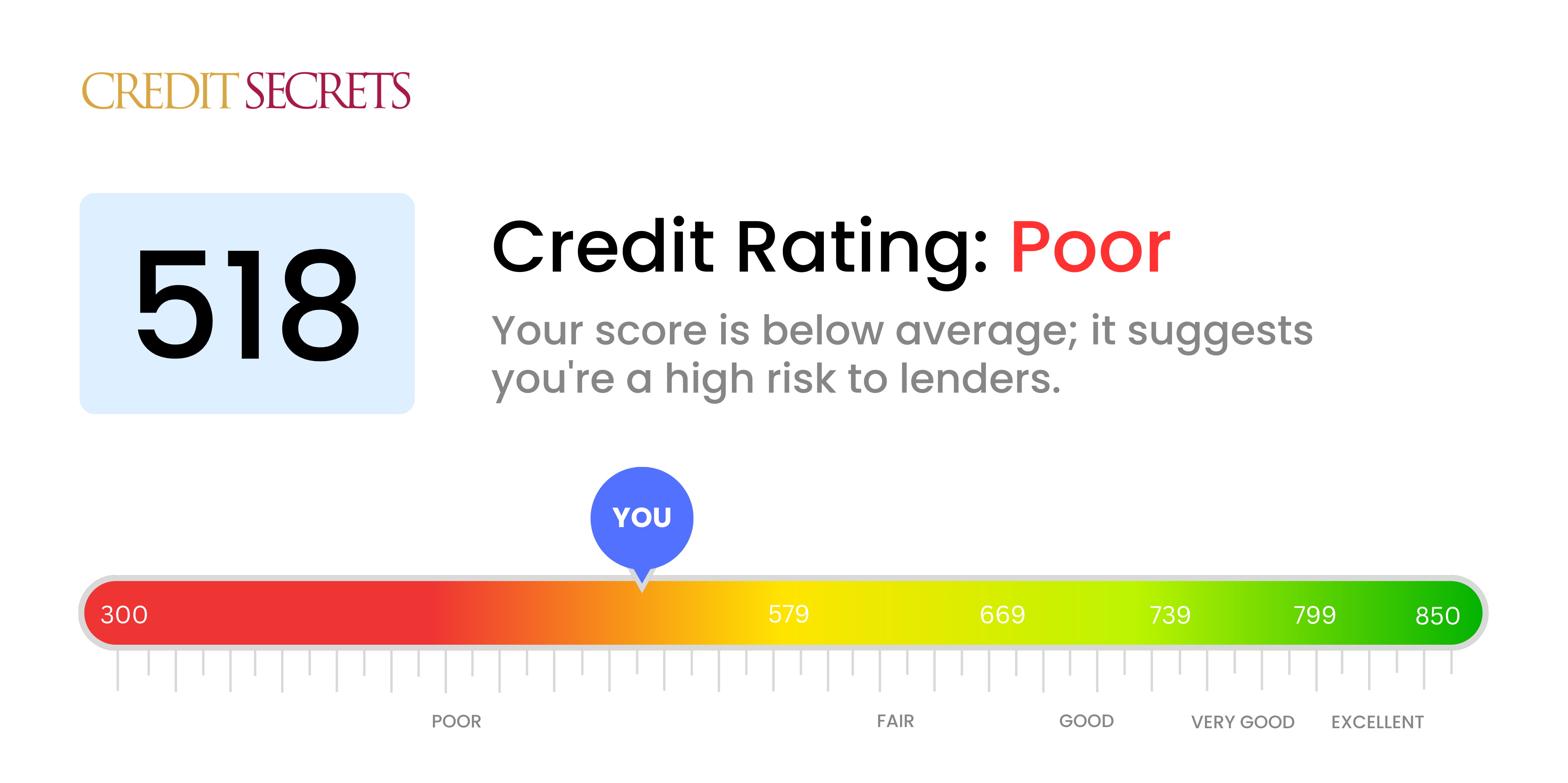

Is 518 A Bad Credit Score

Alright, gather 'round, folks! Let's spill the beans, or should I say, the credit scores. We're here to talk about 518. Is it a number that makes lenders sweat like they've just run a marathon in a sauna? Does it whisper sweet nothings of doom into your financial future? Let's dive in, armed with humor and a healthy dose of reality.

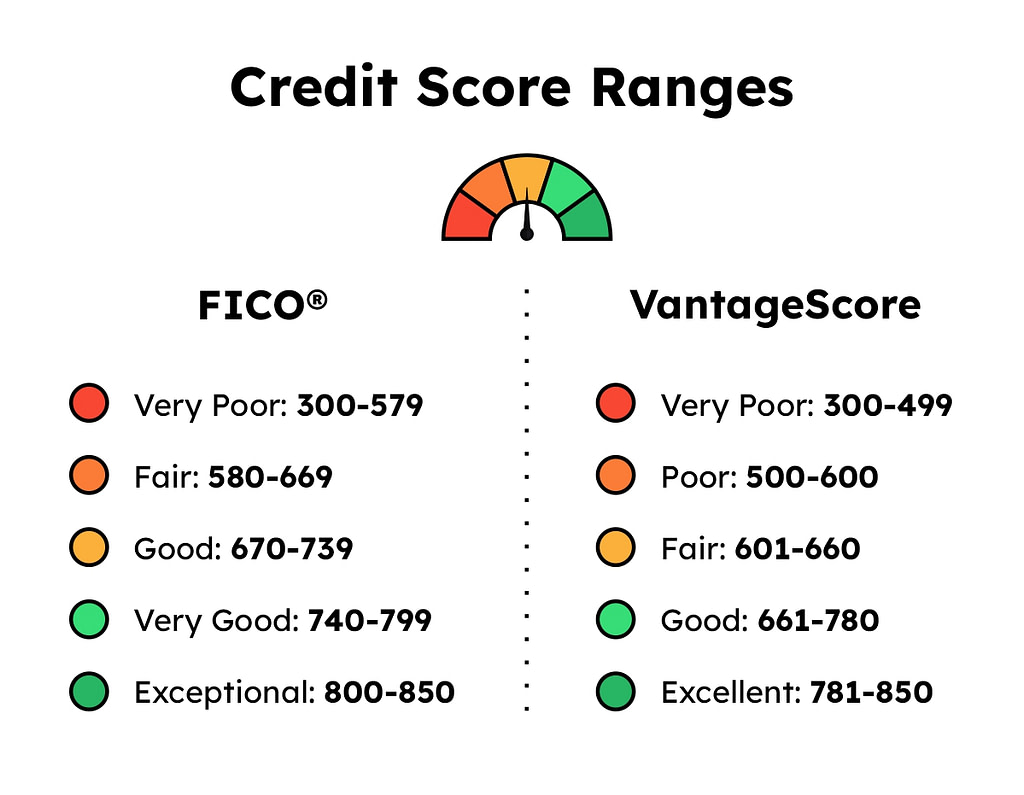

So, 518. Imagine your credit score as a report card for how well you play the grown-up money game. A perfect 850 is like getting straight A's, maybe even a gold star from your very stern math teacher. 700 and above? That’s a solid B+, your parents are proud, and you might even get that new gaming console. Below 600? Uh oh, that’s starting to look like a parental lecture about responsible spending. But 518… that’s in a whole other zip code of… well, let’s just say challenged.

Think of 518 as the credit score equivalent of showing up to a fancy wedding in ripped jeans and a t-shirt that says "I tried." It's not technically the worst thing ever, but it’s definitely not turning heads for the right reasons. It’s the credit score equivalent of a sigh, a raised eyebrow, and maybe a little internal monologue from a bank manager that goes something like, “Bless their heart.”

Now, let's be brutally honest, is 518 bad? Yes. Unequivocally, absolutely, positively, with a side of extra cheese, it's bad. It falls squarely into the "subprime" or "deeply subprime" category. Imagine trying to get a loan with a score like this. It's like trying to convince a cat to take a bath; possible, but you're going to need a lot of treats, a very thick skin, and maybe some protective gear.

Why is 518 Such a Woeful Wanderer?

So, what makes this number a financial pariah? It usually means there's been some serious bumps and bruises on your credit history. Think of the "big three" of credit score sins:

The Three Deadly Sins of a 518 Score

- Late Payments: Not just one or two. We're talking a whole choir of late payments, singing off-key and out of tune with your due dates. It's like forgetting your best friend's birthday every single year. Eventually, people start to wonder if you actually care.

- Collections: This is when a debt goes so sour, the original creditor throws their hands up and says, "You know what? Someone else can deal with this mess." It’s the financial equivalent of a bad breakup where you owe your ex money for that artisanal cheese board.

- Bankruptcy or Foreclosure: These are the nuclear options of financial mishaps. They're like dropping a financial bomb and then trying to rebuild a sandcastle in the crater. These events have a long-lasting, soul-crushing impact.

A 518 score is often the result of a cocktail of these, mixed with maybe a dash of maxed-out credit cards and a sprinkle of too many credit applications in a short period. It's like your credit report is a crime scene, and the score is the detective’s bewildered sigh as they survey the wreckage.

What Does a 518 Score Mean for Your Wallet?

Let’s talk about the real-world impact. Trying to get approved for a loan with a 518 is about as easy as finding a unicorn serving artisanal lattes. If you do manage to find a lender willing to take a chance, prepare for the following:

- Sky-High Interest Rates: They’re going to charge you an arm and a leg, plus maybe your firstborn. Think of it as a "risk premium." They're basically saying, "We're taking a HUGE gamble on you, so you're going to pay us a small fortune for the privilege." It's like buying a lottery ticket where the prize is just getting your money back.

- Huge Down Payments: Forget about getting that fancy new car with zero down. They'll want a down payment that'll make your eyes water, probably enough to buy the dealership outright.

- Limited Options: Your choices will be like a buffet with only three sad-looking peas. You might only qualify for secured loans (where you put up collateral) or loans from lenders specializing in… shall we say… less-than-perfect credit. These are often called "payday loans," and let me tell you, they're the financial equivalent of a leaky faucet – a constant drip, drip, drip of money going down the drain.

- Difficulty Renting or Getting Utilities: Even renting an apartment can become a Herculean task. Landlords see a 518 and might picture you redecorating with spray paint and leaving a trail of unpaid bills. You might also have to put down a hefty security deposit or even pay for utility services upfront.

It's not all doom and gloom, though. Think of it as a wake-up call. A really, really loud, obnoxious, alarm-clock-shattering wake-up call.

Can You Pull a 518 Out of the Financial Abyss?

Yes! Absolutely! It's not a life sentence. It’s more like a temporary detention. The good news is that credit scores are like muscle – they can be built up with effort and consistency. It’s going to take time and dedication, but climbing out of the 500s is totally achievable.

Steps to Financial Redemption

- Face the Music (and Your Bills): First, you need to understand why your score is so low. Pull your credit reports from the three major bureaus (Equifax, Experian, and TransUnion). Look for errors! Sometimes, a simple mistake can drag you down. If you find an error, dispute it. It's like finding a typo in your own obituary; you want to fix it before it's too late.

- Pay Everything On Time, Every Time: This is the absolute, non-negotiable golden rule. Set up automatic payments. Get reminders. Tattoo your due dates on your forehead if you have to. Seriously, even being a day or two late can send you tumbling back down.

- Tackle Those Debts: Start chipping away at any outstanding balances, especially those in collections. Even making small, consistent payments can show lenders you're making an effort. Focus on high-interest debt first. It’s like playing whack-a-mole with your finances, but the goal is to not get whacked.

- Keep Credit Utilization Low: If you have credit cards, try to keep the balance below 30% of your credit limit. Ideally, aim for below 10%. Maxing out your cards is like showing up to a diet competition with a donut in each hand.

- Avoid New Debt Like the Plague (for now): Resist the urge to open new credit accounts. Each application can ding your score slightly, and you don't need any more hits right now. Think of it as a "no unnecessary shopping" phase.

- Consider a Secured Credit Card: This is like a training wheels credit card. You put down a deposit, which becomes your credit limit. Use it responsibly, pay it off on time, and it can help you build positive credit history. It’s like getting a puppy; you have to train it, but it can bring a lot of joy (and a better credit score).

It might feel like an uphill battle, like trying to ski uphill in flip-flops. But remember, every step you take towards better financial habits is a step away from that dreaded 518. It's a journey, not a sprint, and with perseverance, you can transform that number from a financial frown into a financial smile.

So, is 518 a bad credit score? You bet your sweet bippy it is. But is it the end of the world? Absolutely not. It’s simply a signal to hit the reset button and start playing the money game with a little more finesse. Now, go forth and conquer those credit reports! Just try not to spill any coffee on them.