Is An Ira Safer Than A 401k

Hey there, friend! Ever find yourself staring at your pay stub, seeing that little chunk disappear for retirement, and wondering, "What is all this stuff, anyway?" If so, you're definitely not alone. It can feel like trying to navigate a spaghetti junction of financial jargon. Today, we're going to untangle a couple of these big players in the retirement game: the IRA and the 401(k). And we'll do it in a way that's more like chatting over coffee than a stuffy lecture. So, grab your favorite mug, get comfy, and let's dive in!

First off, let's set the scene. Imagine your retirement savings as your future "fun fund." This is the money that'll pay for those epic trips you've been dreaming of, those hobbies you never had time for, or maybe just a really nice, quiet retirement with plenty of time for your beloved cat (or dog, or ferret – no judgment here!). Both IRAs and 401(k)s are like special piggy banks designed to help you build up that fund for the long haul. They offer some pretty sweet tax advantages, which is like getting a bonus in your savings account without doing any extra work.

Now, the big question: Is an IRA safer than a 401(k)? This is where things get a little nuanced, like trying to decide whether pizza or tacos are "safer" for your diet – it really depends on what you mean by "safer," right? Let's break it down.

The Mighty 401(k): Your Workplace Buddy

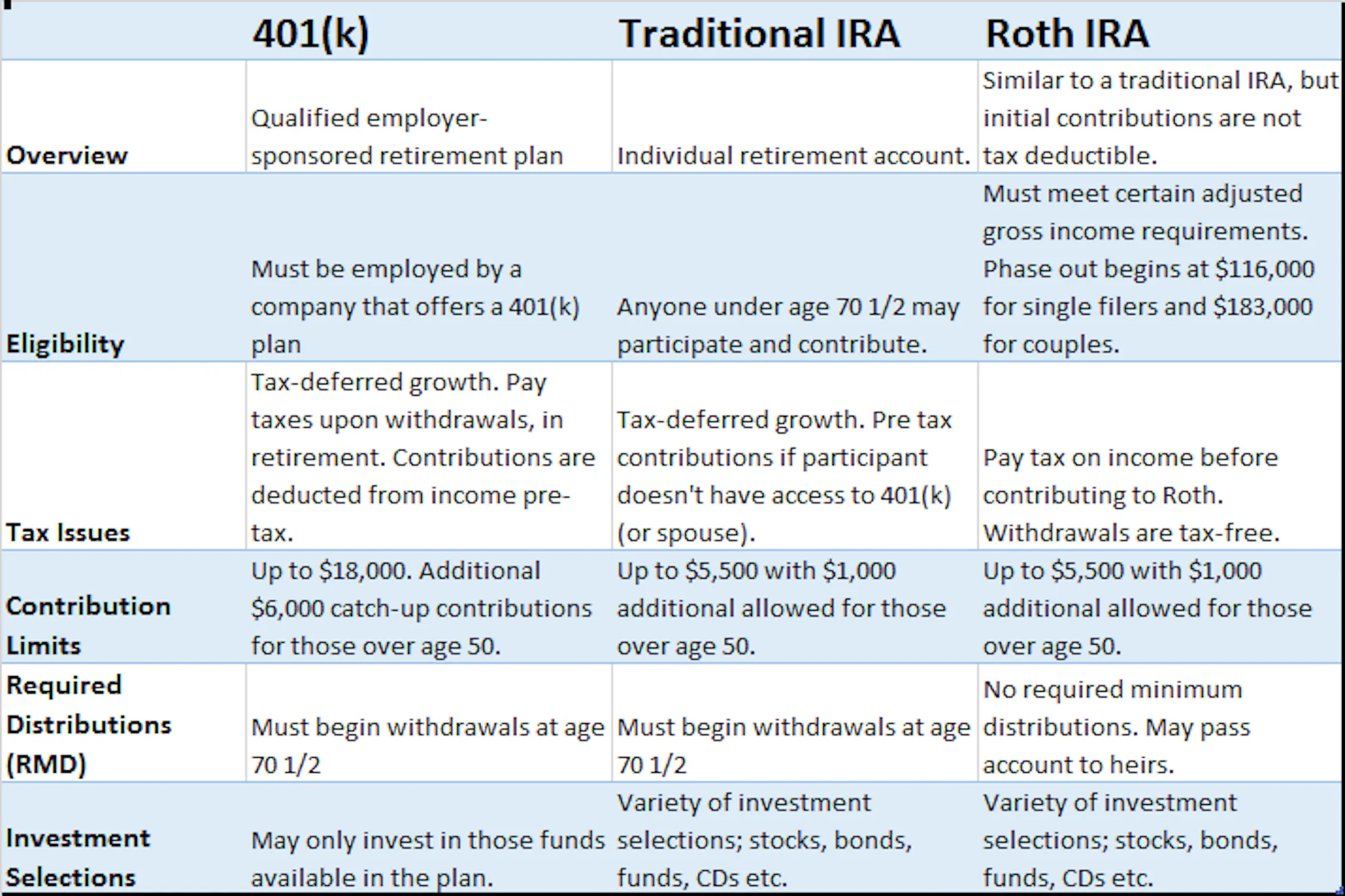

Think of your 401(k) as your employer’s gift to you. It's a retirement savings plan offered through your job. You and your employer can both contribute money to it. This is often where the magic happens, especially if your employer offers a matching contribution. Imagine you put a dollar into your 401(k), and your boss throws in another 50 cents or even a full dollar. That's like finding a twenty-dollar bill in your old jacket – a delightful surprise that boosts your savings significantly!

A key feature of the 401(k) is that it’s employer-sponsored. This means your employer has a vested interest in making sure it runs smoothly. They often choose the investment options available within the plan, and they have a fiduciary duty to act in your best interest. While not foolproof, this often provides a layer of oversight.

One of the most compelling reasons people love 401(k)s is the pre-tax contributions. This means the money you put in comes out of your paycheck before taxes are calculated. So, right now, your taxable income is lower, which can mean a smaller tax bill this year. It’s like getting a little tax break today, so you have more cash in hand. Your money then grows tax-deferred, meaning you don’t pay taxes on any earnings until you withdraw it in retirement. This allows your money to compound and grow faster, like a snowball rolling down a hill, picking up more snow as it goes!

However, with a 401(k), you're typically limited to the investment options your employer provides. Think of it like a buffet: you have a selection of dishes, but you can't go to the grocery store and pick out your own ingredients. This can be great if your employer has curated a solid selection, but if not, your choices might be a bit restricted.

The Versatile IRA: Your Personal Savings Powerhouse

Now, let’s talk about the IRA, which stands for Individual Retirement Arrangement (or Account). This is something you open on your own, independent of your employer. It’s your personal financial playground!

There are two main flavors of IRAs: the Traditional IRA and the Roth IRA. This is where it gets really interesting. The Traditional IRA works similarly to a 401(k) in that contributions might be tax-deductible now, and your money grows tax-deferred. But, just like with the 401(k), you’ll pay taxes on withdrawals in retirement.

The Roth IRA, on the other hand, is a bit of a rockstar for some. You contribute money that you've already paid taxes on. The incredible benefit here is that your money grows tax-free, and qualified withdrawals in retirement are also tax-free! Imagine this: you put in $100 today, and it grows to $1,000 by retirement. If it's in a Roth IRA, that entire $1,000 can be withdrawn without owing a single penny in taxes. It's like finding a secret treasure chest that’s all yours to keep, no questions asked!

The real beauty of an IRA, especially a Roth, is the flexibility and control. You get to choose your investments from virtually anything available on the market – stocks, bonds, mutual funds, ETFs – you name it! It’s like having a personal chef who can cook whatever you want, whenever you want it. You can tailor your investment strategy precisely to your risk tolerance and goals. This control can be a huge advantage, allowing you to potentially chase higher returns or focus on more conservative options.

So, Which is "Safer"? Let's Untangle This

When people ask if one is "safer" than the other, they usually mean a few things:

- Protection from market downturns: Both IRAs and 401(k)s are susceptible to market fluctuations. If the stock market takes a nosedive, your investments in either account will likely decrease in value. So, in this sense, they are equally "risky" because they are subject to the same economic forces. The safety here comes from diversification (not putting all your eggs in one basket) and having a long-term perspective.

- Protection from creditors: Generally, both 401(k)s and IRAs are protected from creditors. This means if you were to face bankruptcy or lawsuits, your retirement savings in these accounts are usually shielded. This provides a significant sense of security for both.

- Control and potential for growth: This is where the IRA shines for many. The broader investment choices in an IRA can offer the potential for greater growth if you make smart investment decisions. However, with greater potential for growth comes greater potential for mistakes. The 401(k) might have a more curated, and perhaps simpler, selection, which can be less overwhelming for some.

- Tax advantages: This is a big one, and it depends on your personal circumstances. If you believe you'll be in a higher tax bracket in retirement, a Roth IRA's tax-free withdrawals are incredibly valuable. If you think you'll be in a lower tax bracket, the up-front tax deductions of a Traditional IRA or 401(k) might be more appealing.

Think of it like choosing between a well-built, reliable car provided by your company (the 401(k)) versus buying your own dream car that you can customize to perfection (the IRA). The company car might be easier to manage and come with some perks, but your dream car offers ultimate freedom and the potential for an amazing ride, provided you know how to drive and maintain it!

Why Should You Even Care?

Because your future self deserves a pat on the back! Seriously, saving for retirement isn't just about numbers on a screen; it's about freedom. It's about being able to enjoy your golden years without the constant worry of making ends meet. It’s about having the ability to say "yes" to spontaneous adventures, to spend quality time with loved ones, or to simply relax and enjoy the fruits of your labor.

Both IRAs and 401(k)s are powerful tools. The "safest" option often comes down to which one best fits your individual financial situation, your comfort level with investing, and your future tax expectations. Many people benefit from having both – a 401(k) through work (especially if there’s a match!) and an IRA for additional savings and investment flexibility. It’s like having a balanced diet: you get the essential nutrients from your main course (401k) and the added vitamins and minerals from your side dishes (IRA).

Don’t let the jargon intimidate you. Start with understanding the basics, and then take small steps. If your employer offers a 401(k) match, absolutely take advantage of it – it’s free money! If you have extra cash, consider opening an IRA. The most important thing is to start saving and to stay informed. Your future self will thank you for it, probably with a big, warm hug and maybe even a perfectly brewed cup of coffee!