Is Fixtures And Fittings An Asset Or Liabilities

Hey there, my awesome friend! Let's dive into something that sounds super business-y, but is actually way more fun and relatable than you might think. We're talking about fixtures and fittings. Yeah, I know, sounds like something from a dusty accounting textbook, right? But stick with me, because understanding these bad boys can actually be a game-changer, whether you're running a business, thinking about selling your house, or just trying to make sense of your own space.

So, what are these mysterious “fixtures and fittings”? Think of them as the things that are attached to your property. They're not like your comfy sofa that you can just whisk away when you move house. Nope, these are the things that are basically screwed, bolted, or plumbed into the very fabric of your building. It's like they've signed a long-term lease on your property!

Let’s break it down with some everyday examples. Imagine you walk into a cafe. You see the gleaming espresso machine, right? And the built-in shelves holding all those tempting pastries? Those are likely fixtures. They are generally considered part of the property itself. They're not just sitting there; they're permanently connected.

Now, what about the “fittings”? This is where it gets a little more nuanced, and honestly, sometimes it's a bit like a game of “Is it or isn’t it?” Fittings are often a bit more… well, fitting to the property, but they might not be quite as permanent as a fixture. Think about the light fittings hanging from the ceiling, or the fancy tap in your bathroom. These are attached, but you could theoretically remove them, even if it’s a bit of a faff.

The key difference, and this is where the accounting wizards (and your brain!) start to perk up, is about permanence. If you were to tip the building upside down (don't try this at home, folks!), would the item fall out? If it stays put, it’s probably a fixture. If it’s dangling precariously, it might be a fitting, or just a very ambitious decoration!

So, the Big Question: Asset or Liability?

This is where the magic happens, my friend! And the answer, like a good plot twist, is… it depends! Gasp! I know, I know, you wanted a simple yes or no. But the world of finance and property is rarely that straightforward. It's more like a beautifully complicated tapestry.

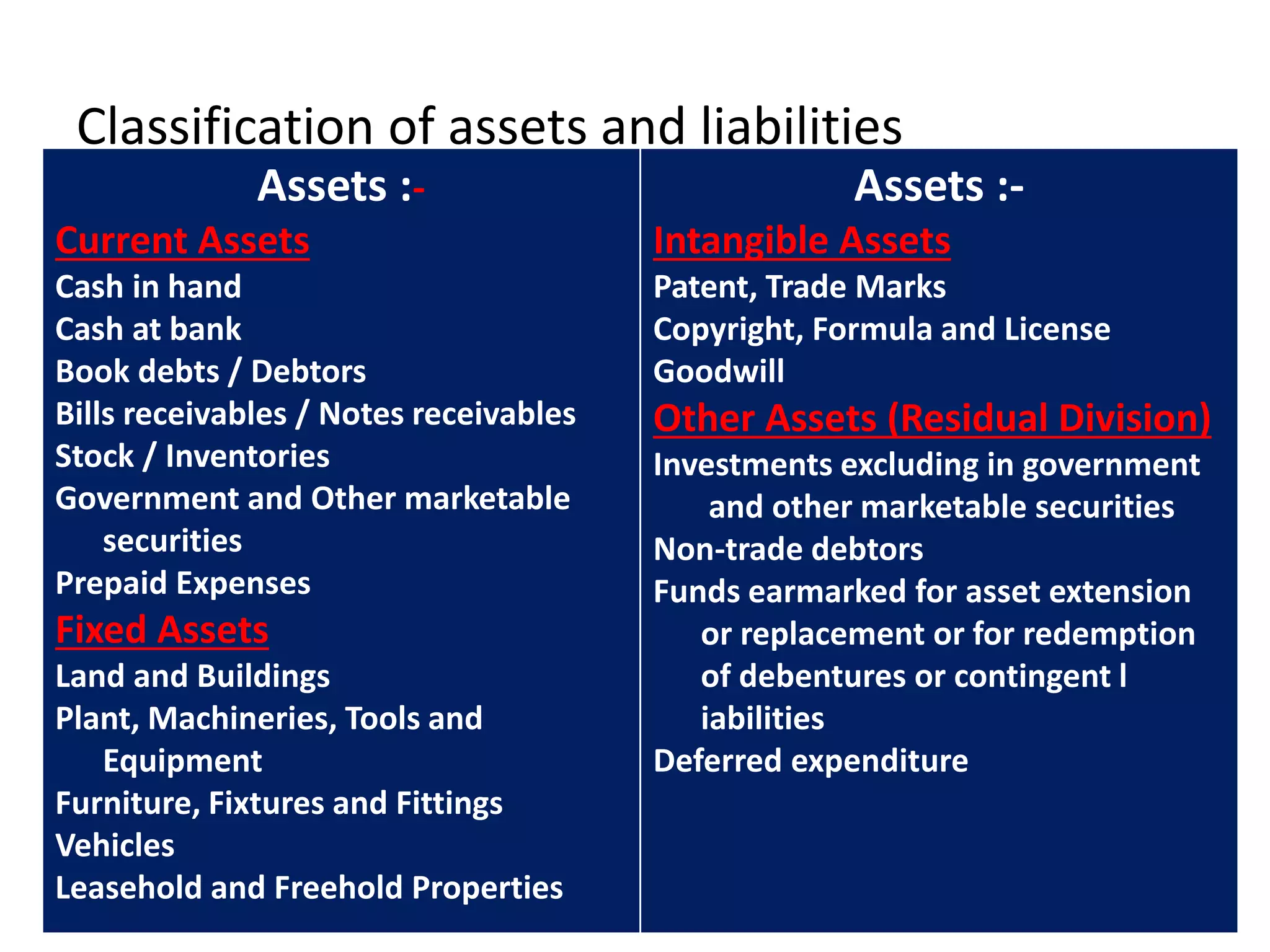

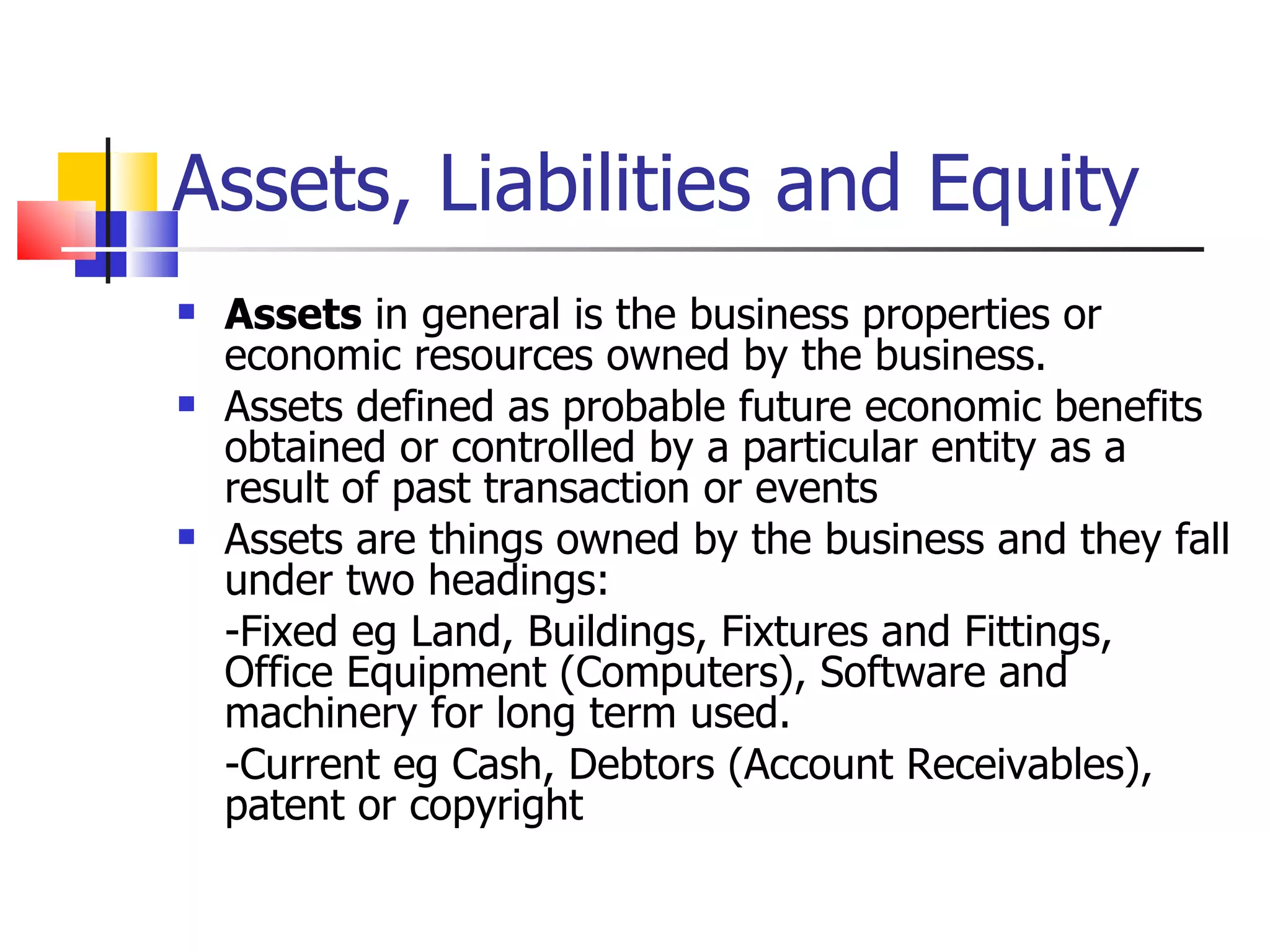

Let's start with the good stuff: assets. In accounting and business terms, an asset is something that has economic value and is expected to provide future benefits. Think of it as a money-maker, or at least something that holds value.

When fixtures and fittings are considered assets, it's usually because they contribute to the value and the earning potential of a business. Imagine a restaurant. Those fancy kitchen appliances? They're essential for cooking the food that brings in the dough! So, they're definitely an asset. The built-in seating? It makes the place comfortable and attractive for customers, so, yep, asset.

For a company, these items are recorded on their balance sheet. This is like a financial report card that shows what they own (assets) and what they owe (liabilities). When you have assets, it generally means your business is in a stronger financial position. They add to the book value of the company. It's like saying, "Look at all these cool, valuable things we have!"

And here's a little bonus: you can often get tax deductions for them! Businesses can depreciate these assets over time, which means they can reduce their taxable income. It's like a little thank you from the taxman for investing in your business infrastructure. Woohoo!

Think of a hotel. The beds, the wardrobes, the air conditioning units – these are all critical for providing a comfortable stay. They are major investments and definitely contribute to the hotel's ability to generate revenue. Therefore, they are undoubtedly assets.

Now, for the Not-So-Glamorous Side: Liabilities

Okay, so when do these seemingly innocent fixtures and fittings turn into the dreaded liabilities? A liability, in simple terms, is something you owe. It's a financial obligation that needs to be settled. Think of debts, loans, and bills.

This is where things get a bit more complex, and often, it’s about how you acquired these items or if they come with ongoing costs. If you bought a whole bunch of custom-built shelving for your office and financed it with a loan, the loan itself is a liability, even though the shelving is an asset. You've got the thing, but you also owe money for it.

Another scenario where fixtures and fittings can lean towards the liability side is if they require significant ongoing maintenance or repair costs. Imagine a really old, elaborate plumbing system in a commercial building. If it's constantly breaking down and costing a fortune to fix, those repair bills start to look a lot like a drain on your finances. The cost of upkeep can become a liability.

Or, think about a leased property. If the lease agreement states that you, as the tenant, are responsible for replacing all the built-in lighting fixtures at the end of your lease, then that future expense becomes a potential liability for you. It’s a cost you’re obligated to cover.

Sometimes, fixtures and fittings can also be considered liabilities if they are obsolete or no longer serve a useful purpose, but you're still stuck with them or have to pay to remove them. Imagine a specialized piece of industrial equipment that’s now completely out of date. It’s taking up space, and getting rid of it might cost you money. Not exactly a cash cow, is it?

This is especially relevant when you're looking at properties for sale. A beautiful, ornate chandelier might seem like a lovely addition, but if it's incredibly energy-inefficient and costs a fortune to run, its ongoing cost could be seen as a de facto liability. It’s not a debt, but it’s a significant financial burden.

The Grey Area: It's Complicated (But Fun!)

Now, let's get real. In many everyday situations, especially for homeowners, the "asset vs. liability" debate for fixtures and fittings isn't about balance sheets and tax returns. It's more about what adds value to your property and what might become a headache.

For example, a beautifully renovated kitchen with top-of-the-line integrated appliances is almost certainly an asset. It makes your home more desirable and can increase its resale value. It’s a major selling point!

On the flip side, that avocado-green bathtub from the 1970s? While it might have sentimental value for some, in terms of market value, it's probably not doing much for your property. In fact, a buyer might see it as a liability – something they'll have to pay to rip out and replace. It’s not a debt, but it’s a future expense they’ll factor in.

It's also about personal preference. What one person sees as a fantastic, high-end fixture, another might see as completely unnecessary and even a negative. It’s the classic “one man’s treasure is another man’s… well, something they want to get rid of” scenario!

Think about the difference between a sleek, modern, energy-efficient boiler and an ancient, clanking monstrosity. The boiler is a fixture, yes. But one is an asset that adds comfort and potentially saves money, while the other is a ticking time bomb that’s likely to be a costly liability when it inevitably gives up the ghost.

The Takeaway: It’s All About Value and Future Benefits

Ultimately, the distinction between an asset and a liability for fixtures and fittings boils down to one simple question: Does it add value or create a future financial benefit, or does it represent a future cost or obligation?

If your fixtures and fittings are contributing to your income, increasing the value of your property, or making your life significantly better and more efficient, then they are most definitely your assets. High fives all around!

If, however, they are costing you a fortune to maintain, are obsolete, or represent an upcoming expense you can’t avoid, then they might be leaning towards the liability side of the ledger. Time to reassess and maybe do some strategic upgrades!

And for those of us not running major corporations, it's simply about understanding what makes our homes and businesses better, more valuable, and more enjoyable places to be. It's about making smart choices that pay off in the long run, whether that's in dollars and cents, or in sheer happiness and comfort.

So, the next time you’re looking at a built-in wardrobe, a fancy light fixture, or even that sturdy old sink, take a moment to consider its journey. Is it a silent helper, adding value and charm? Or is it a potential drain, whispering tales of future expenses? Either way, understanding these details helps you navigate your space with a little more wisdom and a lot more confidence. Keep those assets shining bright, and tackle any potential liabilities with a smile, because you've got this! You're a pro at making things work, and that, my friend, is always a valuable asset!