Is Public Liability Insurance The Same As Employers Liability

Imagine you’re hosting the most epic backyard barbecue. Ribs are sizzling, the music is bumping, and your best friend, Dave, is showing off his questionable dance moves. Suddenly, he trips over a rogue garden gnome and does a spectacular, albeit painful, face-plant into the prize-winning petunias. Ouch!

Now, in this hilarious (for everyone else, probably not Dave) scenario, something important has happened. Someone got hurt, and it happened because they were at your place, at your invitation, even if your invitation was just a casual “come on over!” This is where the magic of Public Liability Insurance swoops in, like a superhero in a sensible suit.

Think of Public Liability Insurance as your friendly neighbourhood guardian angel. It’s there to catch you when things go unexpectedly awry, not for your own personal boo-boos, but when a member of the public – your guest, a delivery person, a curious neighbour peeking over the fence – gets injured or their property gets damaged because of your business or your activities.

So, if Dave’s petunia-pocalypse caused significant damage to your prize-winning blooms (which, let’s be honest, are probably more valuable than Dave’s dignity at that moment), or if he suffered a serious injury that required a trip to the ER for a gnome-related incident, Public Liability Insurance is the safety net that says, “Don’t worry about it, we’ve got this!” It’s about protecting you from potentially hefty bills that could arise from these unforeseen accidents.

"It’s the insurance equivalent of saying, 'Oops, my bad!' when something unintended happens to someone else on your turf."

Now, let’s switch gears a little. Imagine you’re not just hosting a BBQ, but you’ve opened a bustling little bakery. The aroma of freshly baked croissants fills the air, and customers are lining up for your famous sourdough. You’ve hired a team of enthusiastic bakers, all eager to whip up culinary delights.

Among your fantastic team is Brenda, who’s been with you since day one. Brenda, bless her heart, is a master baker but sometimes gets a little too enthusiastic with her dough-kneading. One busy morning, while wrestling with a particularly stubborn batch of brioche, she strains her wrist.

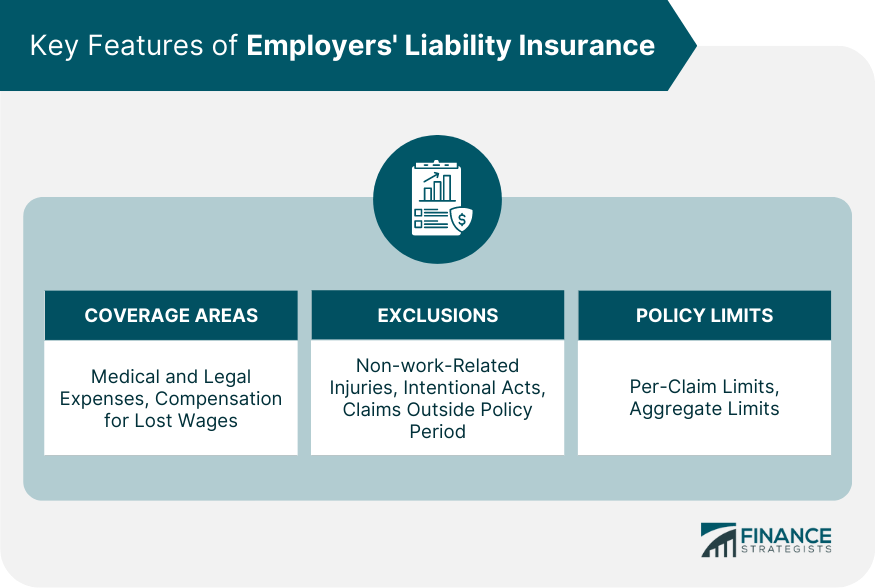

This is where we enter the realm of Employers Liability Insurance. This isn't about your customers or random passersby; it's specifically for your employees. If one of your team members, like Brenda, gets injured or becomes ill because of the work they do for you, this insurance has their back.

Employers Liability Insurance is the loyal sidekick to your business, looking out for the welfare of the wonderful people who help you make your dreams a reality. It’s designed to cover costs associated with workplace injuries or illnesses that aren't covered by the government’s workers’ compensation schemes, or when those schemes aren't sufficient.

So, when Brenda’s wrist needs some TLC, and perhaps some physiotherapy, Employers Liability Insurance is the one that says, “We’re here to help Brenda get back to kneading that brioche with minimal discomfort!” It’s about ensuring your team is looked after when they’re on the clock, doing their best work for you.

The key difference, the truly “aha!” moment, is who is being protected. With Public Liability Insurance, you're thinking about the people who are not directly employed by you but interact with your business or are present on your premises. This includes everyone from your customers to a plumber fixing a leaky faucet in your shop.

Think of it as the “oops, sorry!” insurance for the outside world. Did a customer slip on a wet floor that wasn't properly signposted? Public Liability. Did a falling sign from your shop front startle a pedestrian and cause them to drop their expensive phone? Public Liability. It's all about safeguarding your business from claims made by the general public.

On the other hand, Employers Liability Insurance is your “we care about our crew” insurance. It’s strictly for the people who are on your payroll, the ones who show up every day to help you build your business. It’s for when their work environment, or the tasks they perform, leads to an injury or a health problem.

Did an employee injure themselves lifting heavy stock? Employers Liability. Did an employee develop a respiratory issue from prolonged exposure to certain materials in your workshop? Employers Liability. It's your commitment to your team’s well-being, translated into financial protection.

It’s easy to see how the names can sound similar. Both deal with liability, with something going wrong. But the who is the crucial differentiator. It’s like the difference between your favourite comfy slippers (your employees, whom you cherish and protect) and the unexpected guest who tracks mud into your pristine living room (the public, who might encounter issues on your property).

Let’s revisit our BBQ scenario. If Dave, after his gnome encounter, decides to sue you for pain, suffering, and the emotional trauma of seeing his face in the petunias, your Public Liability Insurance would be your knight in shining armour. It would help cover the legal fees and any compensation you might be liable for.

But if your employee, Gary, who was helping you flip burgers, burned his hand on the grill because the safety guard was faulty, that’s where Employers Liability Insurance steps in. Gary’s well-being is paramount, and this insurance ensures his medical expenses and any lost wages are addressed.

So, while both are vital pieces of the business puzzle, they serve distinct purposes. One protects you from claims by the outside world, and the other protects you and your business when your own team needs support due to work-related incidents.

Think of it this way: Public Liability is your business’s social butterfly wings, protecting it from unexpected bumps and bruises when interacting with the wider world. It’s about being a good neighbour and a responsible business owner to everyone who crosses your path, even unintentionally.

And Employers Liability? That’s your business’s strong, protective shield for its beloved crew. It’s the promise that when your team gives their all, you’ve got their back in case of an accident or illness directly related to their job. It’s the heartwarming assurance that your people matter, and their safety and health are a priority.

They’re not interchangeable, but they are both incredibly important for different reasons. One is for the general public, the other is for your cherished employees. Both contribute to a safer, more secure, and ultimately, happier business environment for everyone involved.

So, the next time you hear about these types of insurance, you’ll know they’re not just confusing jargon. They’re practical, essential tools that help keep businesses thriving while looking after both their neighbours and their nearest and dearest team members. They’re the unsung heroes of a smooth-running operation, ensuring that even when a gnome gets involved, everyone’s covered!