Iul Policy Guide: Cash Value, Death Benefit, And Common Pitfalls

Hey there, my friend! So, you've been hearing whispers about these things called IULs, right? Indexed Universal Life insurance. Sounds a bit fancy, like something a Wall Street wizard would chat about over a tiny espresso. But honestly, it's not as intimidating as it seems. Think of it like a Swiss Army knife for your life insurance – it does more than just one thing, which is pretty neat!

We're going to break down the cool parts – the cash value and the death benefit – and then, because nobody likes surprises (except maybe finding a twenty in an old coat pocket!), we'll chat about some of the common pitfalls to watch out for. No scary stuff, just helpful tips so you can navigate this without feeling like you're lost in a financial maze. Ready to dive in? Let's do this!

The Magic of Cash Value: Your IUL's Little Treasure Chest

Okay, so the first big thing about an IUL is this cash value. Imagine you're paying your premiums, right? A portion of that money doesn't just vanish into the ether like a magician's rabbit. Instead, it goes into this special account, your cash value. It's like a little savings account that lives inside your life insurance policy. Pretty cool, huh?

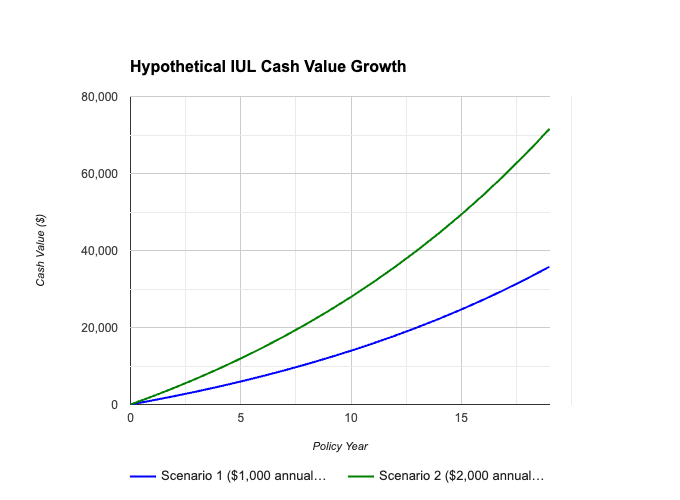

But here's where it gets really interesting. This cash value isn't just sitting there, collecting dust. It's indexed. What does that mean? Basically, its growth is tied to the performance of a stock market index, like the S&P 500. So, if the market does well, your cash value has the potential to grow. Think of it like your money going on a mini-vacation to the stock market and hopefully coming back with some extra souvenirs (aka, earnings!).

Now, before you start picturing yourself buying a private jet on your IUL gains, let's pump the brakes a tiny bit. There are usually caps and floors. A cap is like the maximum your cash value can earn in a year, even if the market goes bonkers. And a floor? That's the minimum your cash value will earn, often 0%. So, even if the market tanks and your neighbor's stocks are doing the cha-cha slide into oblivion, your cash value is protected from losing money due to market downturns. That's the "insurance" part kicking in – a safety net for your savings!

This cash value grows tax-deferred. That's a biggie! It means you don't pay taxes on the earnings each year. They just keep growing. You can only imagine how that stacks up over time. It's like that snowball rolling down a hill, getting bigger and bigger. (Just try not to imagine it rolling over your favorite flowerbed.)

What Can You Do With This Cash Value?

So, you've got this growing pot of gold. What now? Well, you have a few options. You can simply let it grow and grow, letting that tax-deferred magic work its charm. It becomes a nice little nest egg for the future.

But wait, there's more! You can also borrow against your cash value. This is a really neat feature. Think of it like taking a loan from yourself. You're not beholden to a bank's approval process or high-interest rates. You can use these loans for whatever you need – maybe a down payment on a house, starting a small business, or even just covering an unexpected emergency. Pretty flexible, right?

When you borrow, the loan is typically taken from the insurance company, and they'll charge you interest. However, the outstanding loan balance (and interest) will reduce the death benefit if you don't repay it. It’s important to understand the terms and conditions of these loans. It’s your money, but it’s still within the policy, and there are rules!

Another option is to withdraw from your cash value. You can take out funds directly. Again, there might be some tax implications depending on how much you withdraw and how old the policy is, but generally, withdrawing up to the amount you've paid in premiums isn't taxed. It’s always a good idea to chat with your financial advisor about the best way to access these funds without any nasty surprises. They're like your financial GPS!

The Star of the Show: The Death Benefit

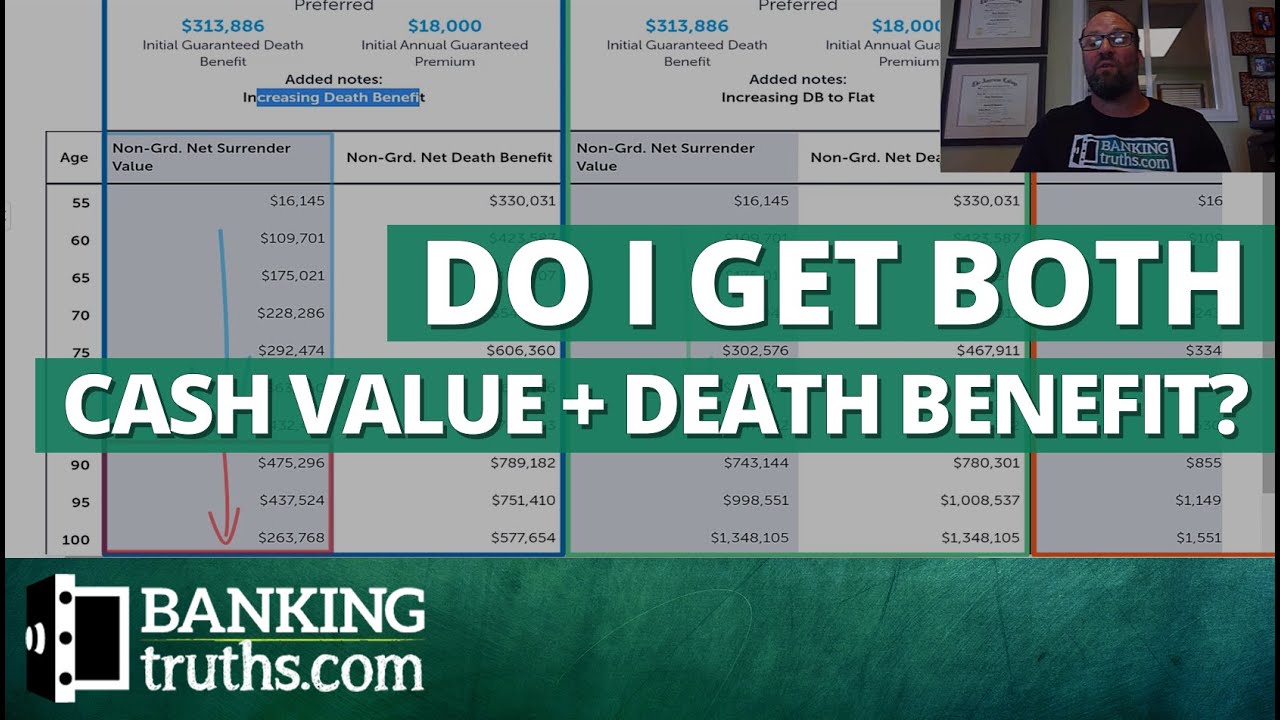

Now, let's talk about the other crucial part of any life insurance policy: the death benefit. This is the lump sum of money that your beneficiaries (your loved ones, the people you care about) receive if you, unfortunately, pass away while the policy is in force. It's the fundamental reason most people get life insurance in the first place.

With an IUL, the death benefit typically has two parts: the specified amount (the death benefit you initially chose) and the cash value. This means that your beneficiaries will receive the specified amount plus the accumulated cash value. How awesome is that? It’s like a double whammy of goodness for your loved ones when they need it most.

This can be a significant advantage, especially if you plan to hold the policy for a long time and your cash value grows substantially. It provides a larger financial cushion for your family, helping them cover immediate expenses, replace lost income, and maintain their lifestyle.

It's important to remember that the death benefit is generally received by your beneficiaries income tax-free. That’s a huge relief for them during what would already be an incredibly difficult time. No one wants their grieving family to be worried about taxes on the money meant to support them.

Flexibility is Key: Adjusting Your Death Benefit

One of the nifty things about Universal Life policies, including IULs, is that they often offer some flexibility with your death benefit. Depending on your policy and insurer, you might be able to increase or decrease your death benefit over time. Life changes, right? You might have more kids, your financial needs might evolve, or perhaps you’ve achieved some financial goals and no longer need as much coverage. This flexibility can be a lifesaver, ensuring your policy stays relevant to your life circumstances.

However, be aware that increasing your death benefit will likely mean higher premiums. And decreasing it might impact the long-term cash value growth or even the policy's guarantees. So, it's not a "set it and forget it" situation. Regular check-ins with your policy and advisor are key!

Navigating the Minefield: Common IUL Pitfalls

Alright, so we've covered the shiny bits. Now, let's be real. No financial product is perfect, and IULs are no exception. There are a few common traps that people can fall into if they're not paying attention. Think of this as your friendly heads-up, so you can sidestep any potential oopsies. Nobody wants to be the "whoopsie" person, right?

Pitfall #1: Overpaying Premiums (or Underpaying!)

This is a big one. IULs are designed to be flexible with premiums, which is great, but it also means you can mess it up if you're not careful. If you consistently pay less than the target premium, your policy might not build enough cash value to cover its internal costs, and it could lapse. A lapsed policy means your death benefit is gone, and you might owe taxes on the cash value you've accumulated.

On the flip side, sometimes people feel like they need to stuff as much money as possible into the policy, thinking "more is more!" While contributing more can be good, there are IRS limits on how much you can contribute to avoid being classified as a Modified Endowment Contract (MEC). If your policy becomes a MEC, it loses some of its tax advantages, especially regarding loans and withdrawals. It's a bit like trying to fit too many marshmallows into your mouth – it's just not going to end well.

The key is to pay enough to keep the policy in force and allow for growth, but not so much that you trigger MEC rules or go overboard. This is where your financial advisor is your superhero.

Pitfall #2: Underestimating Policy Costs and Fees

Insurance policies, especially the more complex ones like IULs, have costs. There are cost of insurance charges, which is the actual cost of insuring your life. Then there are administrative fees, underwriting fees, and sometimes even rider fees if you add extra benefits. These costs are often deducted from your cash value.

![Is Cash Value Part of the Death Benefit? [Infographic] | FIG Marketing](https://www.figmarketing.com/blog/wp-content/uploads/2021/05/BP-04.22.21-DeathBenefit-2.jpg)

In the early years of an IUL, these costs can be quite significant and can eat into your cash value growth. If your cash value isn't growing fast enough to offset these costs, your cash value might dwindle. It's like a leaky faucet – small drips can add up to a big problem over time. Make sure you understand what these fees are and how they impact your policy's performance. Don't be shy about asking for a full breakdown!

Pitfall #3: Relying Solely on Index Performance

Remember how we talked about the cash value being tied to an index? It sounds fantastic, but it's not a guaranteed path to riches. As we mentioned, there are caps, and sometimes the index might not perform as well as you'd hoped. Relying on the IUL as your only investment vehicle for retirement or long-term goals can be risky.

Think of the IUL's cash value growth as a component of your overall financial strategy, not the entire orchestra. It offers tax-deferred growth and some downside protection, which is valuable, but it might not provide the aggressive growth you'd get from other investment vehicles, and it's not a substitute for traditional retirement accounts like 401(k)s or IRAs, which often have higher contribution limits and different growth potentials.

Pitfall #4: Lack of Understanding and Poor Advice

This is the supervillain of all pitfalls! If you don't understand how your IUL works, or if you're getting advice from someone who doesn't truly understand it either, you're setting yourself up for trouble. IULs can be complex, with various crediting methods, loans, and surrender charges. Trying to navigate this without proper guidance is like trying to assemble IKEA furniture without the instructions – a recipe for frustration and possibly a wobbly bookcase.

Always seek advice from a qualified and trustworthy financial advisor who specializes in life insurance. Ask questions. Lots of them. The more you understand, the better decisions you can make. Don't be afraid to say, "Wait, can you explain that again?" Your future self will thank you!

Also, be wary of salespeople who make outlandish promises or try to pressure you into a sale. A good advisor will focus on your needs and explain the pros and cons transparently. Remember, it's your money and your future we're talking about!

Pitfall #5: Not Reviewing the Policy Periodically

Life happens, and so do changes in financial markets and insurance regulations. An IUL policy isn't a "set it and forget it" thing. You need to periodically review your policy with your advisor. This means checking how your cash value is performing, understanding any changes in fees, and ensuring that the death benefit still aligns with your current needs.

What was right for you five years ago might not be right for you today. Perhaps your income has increased, and you can afford to put more into the policy, or maybe your financial goals have shifted. Regular check-ins ensure your IUL remains a valuable tool in your financial arsenal, rather than becoming an outdated piece of paper.

Think of it like taking your car for its annual service. You want to make sure everything is running smoothly and catch any small issues before they become big, expensive problems. Your IUL deserves the same attention!

So, there you have it! The wonderful world of IULs, with its potential for growth and security, but also with its little quirks and corners to be aware of. It’s a powerful tool, but like any powerful tool, it needs to be understood and used wisely.

By understanding the cash value and death benefit, and by being mindful of these common pitfalls, you can make an informed decision about whether an IUL is the right fit for your financial journey. And if it is, you’ll be well-equipped to make it work for you, not against you.

Remember, the goal is to build a secure future, and sometimes, a well-understood IUL can be a fantastic part of that plan. So go forth, my friend, armed with knowledge and a smile, ready to explore your options with confidence. Here's to smart financial decisions and a brighter tomorrow!