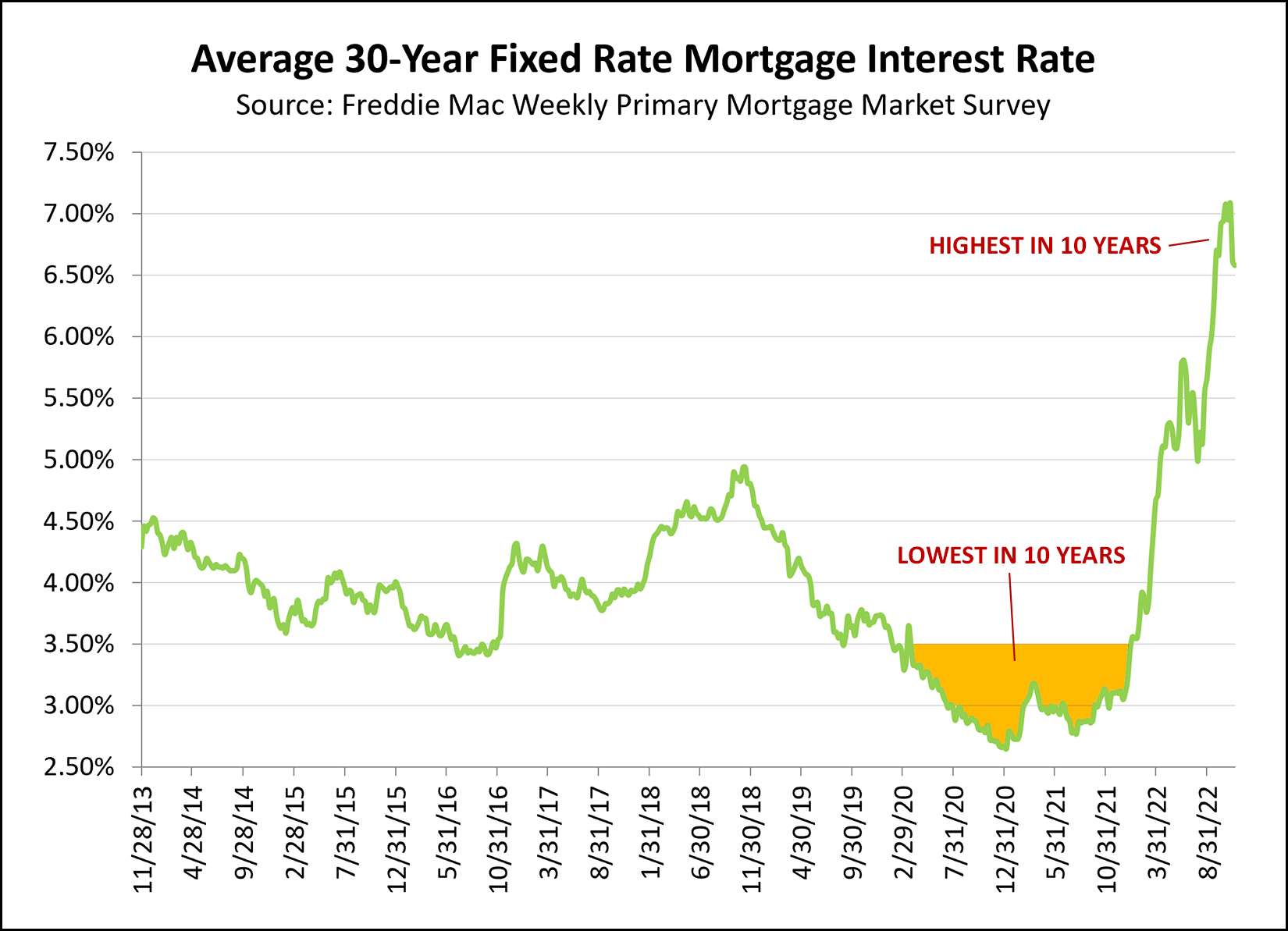

Mortgage Rates Lowest Ever

Hey there, homebodies and dreamers! Ever feel like the universe is just handing out freebies lately? Well, buckle up, because we’re diving headfirst into a topic that’s been making waves faster than a summer beach party: mortgage rates are hitting historic lows! Yep, you heard it right. If you’ve been casually browsing Zillow during your Netflix binges, or secretly picturing that perfect backyard for your future dog, now might just be your moment.

Think of it like finding a surprise discount code for your life's biggest purchase. It’s not just a little "ooh, nice," it’s a genuine, game-changing, "heck yeah!" situation. For years, we’ve seen these numbers inching up and down, a bit like the fluctuating popularity of avocado toast (though arguably, a bit more impactful on our long-term finances).

The "Wow, That's Low!" Factor

So, what are we even talking about when we say "lowest ever"? We’re talking numbers that would make your grandparents, who probably bought their first homes for less than your current car, raise an eyebrow. These rates mean that the cost of borrowing money to buy a home has never been more affordable in recent memory. It’s like the housing market decided to throw a massive sale, and everyone’s invited.

Why does this matter so much? Well, it directly impacts your monthly mortgage payment. A lower interest rate means a smaller chunk of your hard-earned cash goes towards interest over the life of your loan, and more goes towards actually owning that sweet piece of real estate. Over 15 or 30 years, this can add up to tens, even hundreds, of thousands of dollars saved. That’s enough for a couple of epic vacations, a serious home renovation project, or even a comfy retirement nest egg. See? We told you it was a big deal!

A Little History Lesson (The Fun Kind!)

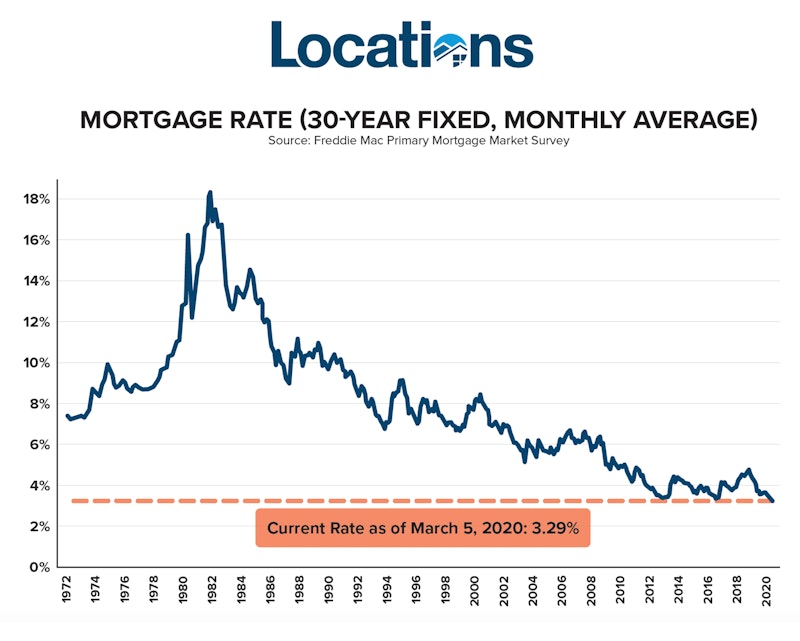

To really appreciate this moment, let’s take a quick peek back. Back in the 1970s and 80s, mortgage rates could be in the double digits, easily soaring above 10%, 12%, or even higher. Imagine that! Your monthly payment would be a whole different ballgame. It’s like comparing the price of a cassette tape to the price of a streaming subscription – a complete evolution.

Now, we’re looking at rates that are a fraction of those historic highs. It’s a testament to economic shifts, central bank policies, and a whole lot of global financial wizardry that’s a bit too complex for a casual article (and frankly, for most of us to fully grasp after a long day). But the result is what’s important: a golden opportunity for homebuyers.

So, Who Benefits Most?

Honestly? Pretty much everyone looking to buy.

First-time homebuyers, this is your moment to shine! Entering the market with lower borrowing costs can make that initial leap feel a lot less daunting. It can help you get your foot in the door sooner and start building equity.

Existing homeowners looking to refinance are also in a prime position. If you bought your home when rates were higher, refinancing into a lower rate can significantly reduce your monthly payments or allow you to pay down your mortgage faster. Think of it as an upgrade for your financial situation. It’s like switching from a dial-up internet connection to lightning-fast fiber optic – pure bliss!

Even those who have been on the fence, perhaps waiting for the "perfect time," might find that "perfect time" is right now. The market is dynamic, and opportunities like this don’t last forever.

Making the Most of Low Rates: Practical Tips

Alright, enough with the abstract economic talk. Let’s get down to the nitty-gritty: what can you do with this information?

1. Get Pre-Approved (Like, Yesterday!)

This is step one, the absolute non-negotiable. Before you even start seriously scrolling through listings, get pre-approved for a mortgage. This tells you exactly how much you can borrow and at what potential rate. It also shows sellers you’re a serious contender, which is always a plus in a competitive market. Think of it as getting your "go" signal from the universe of homeownership.

Pro tip: Shop around! Don't just go with the first lender you talk to. Compare rates and fees from at least three different lenders (banks, credit unions, mortgage brokers). A small difference in rate can make a big difference over time.

2. Understand the Different Loan Types

You've got options! The most common are fixed-rate mortgages (where your interest rate stays the same for the entire loan term) and adjustable-rate mortgages (ARMs), where the rate is fixed for an initial period and then can fluctuate.

With rates so low, a fixed-rate mortgage is incredibly attractive. It offers stability and predictability. You know exactly what your principal and interest payment will be month after month, year after year. No surprises, just steady progress towards owning your home. It’s the financial equivalent of your favorite comfort food – reliable and always hits the spot.

ARMs can be tempting if you plan to sell or refinance before the initial fixed period ends, but they come with the risk of future rate increases. Given the current low environment, locking in a low fixed rate is often the safer and more appealing bet for long-term peace of mind.

3. Consider the Loan Term

Are you a 15-year mortgage kind of person or a 30-year mortgage enthusiast? A 15-year mortgage typically comes with a lower interest rate than a 30-year mortgage. Your monthly payments will be higher, but you’ll pay off your home much faster and save a substantial amount on interest over the life of the loan. It’s like choosing the express lane to homeownership!

A 30-year mortgage, on the other hand, offers lower monthly payments, freeing up cash flow for other financial goals or simply making homeownership more accessible. With the current low rates, even a 30-year loan can be incredibly affordable.

The choice depends on your financial situation and comfort level. Want to be mortgage-free in half the time and save a fortune? Go for 15. Need more breathing room in your monthly budget? 30 might be your jam. It's all about what fits your lifestyle.

4. Don't Forget the Other Costs

Low interest rates are fantastic, but remember that buying a home involves more than just the mortgage. You’ll have closing costs (appraisal fees, title insurance, lender fees, etc.), property taxes, homeowner's insurance, and potentially HOA fees. Make sure you factor all of these into your budget. It’s like planning a road trip – the gas is a major cost, but you still need to budget for snacks, lodging, and maybe a cheesy souvenir!

5. Boost Your Credit Score

If your credit score isn't quite where you'd like it, now is the perfect time to give it a little TLC. A higher credit score can unlock even better interest rates, saving you even more money. Pay down credit card balances, avoid opening new lines of credit unnecessarily, and ensure you’re paying all your bills on time. It’s amazing what a few months of good financial habits can do!

Fun Facts and Cultural Connections

Did you know that the concept of a mortgage has been around for centuries? Ancient Babylonians had loan contracts for land! Of course, they didn’t have the fancy apps or online portals we do today. Imagine trying to negotiate a mortgage with a clay tablet!

The term "mortgage" itself comes from Old French, meaning "dead pledge." It referred to the pledge given to the lender that would die or be extinguished once the debt was paid off. Pretty dramatic, right?

And let's not forget the cultural impact of homeownership! Think of all the iconic movie scenes set in dream homes, the aspirational imagery in magazines, and the simple joy of having your own space to decorate, entertain, and just… be. From the suburban idylls of the 50s to the urban lofts of today, the idea of having a "place of your own" is deeply ingrained in our culture.

The "What If" Factor

You might be thinking, "What if rates go up again soon?" That's a valid concern. Predicting interest rates is a bit like predicting the weather – you can make educated guesses, but there are always surprises. However, the consensus among many experts is that while rates may eventually tick up, they are likely to remain historically low for a considerable period. This window of opportunity is real, and it’s worth exploring.

The Federal Reserve plays a huge role in setting the benchmark interest rates that influence mortgage rates. They’ve been keeping rates low to stimulate the economy, and while that can't last forever, the impact is significant while it does. It’s like when your favorite artist releases a surprise album – you enjoy it while it’s here!

A Moment of Reflection

In the grand scheme of life, a mortgage is just a tool. It's a way to facilitate a significant life goal: creating a home. And right now, that tool is more affordable than it has been in generations.

So, as you sip your morning coffee, or scroll through your social media feed, take a moment to consider what low mortgage rates could mean for you. It’s not just about numbers on a screen; it’s about the possibility of a backyard BBQ with friends, a quiet reading nook by the window, a space to grow your family, or simply the peace of mind that comes with building your own equity.

This isn't just financial news; it's an invitation. An invitation to potentially secure your future, to invest in yourself, and to make that dream home a tangible reality. So, why not explore it? After all, opportunities like these are rare, and like that perfectly ripe avocado, they’re best enjoyed when they’re at their peak.