My Credit Score Has Stalled

Hey there, my fellow credit score adventurers! So, you’re staring at your credit report, and it’s… well, let's just say it's not exactly doing the Macarena. It's more like it’s stuck in slow motion, a credit score equivalent of watching paint dry. Yep, we’ve all been there. That moment when you’re trying to get approved for something awesome – maybe a new apartment, a sweet car loan, or even just a better interest rate on your trusty credit card – and your score is giving you the cold shoulder. It’s like your score just decided to take a permanent vacation without sending a postcard.

You’ve been diligently paying bills on time, not maxing out your cards (most of the time, anyway – we’ve all had those emergency ice cream fund moments!), and generally being a good financial citizen. So why the heck is your credit score playing hard to get? It’s enough to make you want to throw your computer out the window, right? Don’t do that! Your computer probably didn’t do anything wrong. Your credit score, however, might be having a bit of a midlife crisis.

Let’s dive into this perplexing phenomenon, shall we? Think of your credit score as your financial report card. It’s a three-digit number that tells lenders how likely you are to repay borrowed money. And just like your actual report card in school, sometimes it just doesn't budge, even when you feel like you're acing the exam. It's like you're putting in all the effort, doing all the homework, and yet, that 'A' just isn't showing up. Frustrating, I know!

Why is My Credit Score Playing Hide-and-Seek?

So, what gives? Why is your credit score suddenly less exciting than a beige sock drawer? Several culprits could be playing a role. It’s not usually a single dramatic event, but more like a slow, creeping stagnation. Think of it as a garden that’s been watered and weeded, but it’s just not flowering as much as you’d hoped. You’re doing the right things, but maybe something’s missing.

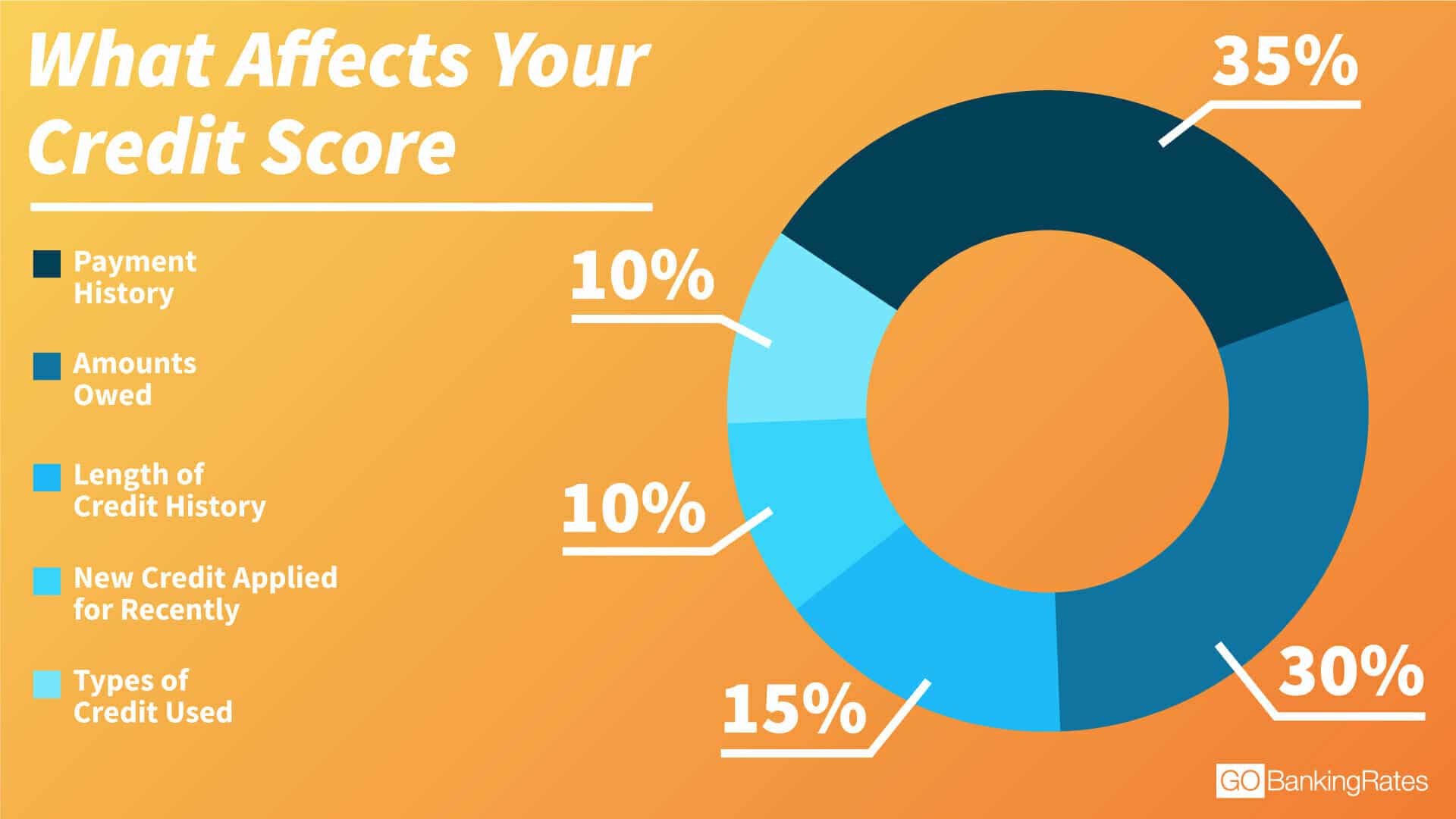

One of the most common reasons is simply a lack of recent activity. If you’re not using your credit cards much, or you haven’t applied for new credit in a while, your credit score might feel a bit… uninspired. Lenders like to see that you can manage credit responsibly over time. If there’s not much to see, they can’t really gauge your current financial habits. It’s like a chef who only cooks one dish for a decade – how can you judge their versatility? Your credit score needs a little variety to show off its skills!

Another sneaky reason is that your credit utilization ratio might be hovering around a certain percentage and not moving. This ratio is the amount of credit you’re using compared to your total available credit. Ideally, you want this to be below 30%, and even lower is better. If you’re consistently at, say, 25%, and you don’t see it dip or rise (within reason, of course!), your score might just be saying, “Meh, it’s fine.” It’s not necessarily bad, but it’s not exactly shouting from the rooftops either. It’s that perfectly adequate, but not spectacular, student who always gets a ‘B’ but never quite breaks into ‘A’ territory.

Then there’s the issue of thin credit files. If you’re new to credit, or you’ve only had a couple of accounts for a short time, your credit history might not be robust enough for the scoring models to get a really good read. They like a good story to tell! Imagine trying to write a novel with only three sentences. It’s just not going to be very compelling, is it? Your credit score needs a rich narrative to truly shine.

And sometimes, honestly, it's just the natural ebb and flow of credit scoring. Credit scores aren't static. They change based on your financial behaviors, and sometimes, they just plateau. It’s like hitting a fitness plateau – you’re working out, but the scale isn’t budging. You need to switch up your routine, right? Your credit score might be whispering, “I need a new gym membership!”

Okay, So My Score is Stuck. Now What?

Deep breaths, my friend. We’re not giving up on this little numerical buddy just yet! There are absolutely things you can do to give your credit score a gentle nudge, or maybe even a good old-fashioned pep talk. Think of yourself as the motivational coach for your creditworthiness.

First up, let’s talk about strategic credit usage. Remember that credit utilization thing? If yours is a bit high, aim to pay down your balances. If it’s really low, you might consider making a few small, intentional purchases on your credit card and then paying them off immediately. This shows lenders that you're actively using and managing your credit. It's like giving your score a little workout. Just don't go on a spontaneous shopping spree for a solid gold toaster! Keep it reasonable.

Another brilliant move? Open a new, responsible credit account. Now, I’m not saying run out and get ten new store cards for the discount (tempting, I know!). But a secured credit card, or a small retail card from a store you actually use, can be a great way to add to your credit mix and history. Just make sure you can handle the payments, obviously. This is like adding a new character to your credit report’s story, making it more interesting for the lenders. Plus, it can help lower your overall credit utilization if you have existing high balances on other cards.

Have you been meaning to check your credit report for errors? Now’s the time! Dispute any inaccuracies you find. Seriously, sometimes a little clerical error can be holding your score hostage. It’s like finding out your teacher accidentally marked your perfect essay as a ‘C’. You’d want that fixed, right? You can usually get free copies of your credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) once a year. Knowledge, as they say, is power. And in this case, it’s credit-improving power!

Consider becoming an authorized user on a trusted friend or family member's credit card. If they have a great credit history and low utilization, their good habits can sometimes rub off on your score. Think of it as a credit-boosting mentorship. Just make sure they’re actually responsible with their credit, otherwise, you might be inviting a financial gremlin into your credit report. Always choose your credit fairy godparent wisely!

The Long Game: Patience is a Credit Score Virtue

Let’s be real, building and maintaining a stellar credit score is a marathon, not a sprint. And sometimes, even when you're doing all the "right" things, the score just takes its sweet time to catch up. It’s like trying to grow a prize-winning pumpkin – you water it, you feed it, you give it sunshine, and eventually, it gets big. But it doesn't happen overnight.

So, if your score has stalled, try not to get discouraged. Keep up with your responsible financial habits. Pay your bills on time, keep your credit utilization low, and avoid unnecessary credit applications. These are the foundational elements of a good credit score, and they will, eventually, be rewarded. Your score is like a shy teenager – it might take a little time and encouragement to come out of its shell and show its true potential.

Think about the positive actions you're already taking. You're aware of your credit score, you're looking for ways to improve it, and you're not letting a temporary plateau derail your financial goals. That’s huge! Many people don't even pay attention to their credit until they're denied something, and by then, it can feel like a bigger mountain to climb. You're ahead of the game!

It's easy to get caught up in the numbers, but remember what a good credit score does for you: it opens doors. It can save you money on interest, make it easier to get the things you need and want, and generally give you more financial freedom. So, when your score feels stuck, picture that future where you're confidently signing for that new car or getting that dream apartment. That’s the goal, and you’re on the path!

The Bright Side: You've Got This!

So, my friend, if you’re feeling a little frustrated that your credit score has decided to take a nap, I hear you. It can be a bit of a head-scratcher. But here’s the really good news: you’re not powerless! You’re already doing a lot of the right things, and by being proactive and making a few strategic moves, you can absolutely get your score moving again. Think of this stalled score not as a failure, but as a little nudge to refine your approach. It’s a chance to become an even more savvy credit manager!

You’re learning, you’re growing, and you’re building a stronger financial future with every responsible decision you make. Even if it feels slow, progress is progress. So, give yourself a pat on the back for being so financially aware. Keep those payments coming in on time, keep an eye on your utilization, and maybe try one of those little credit-boosting tricks we talked about. Before you know it, your credit score will be doing the cha-cha, the salsa, or maybe even the electric slide!

And when it finally starts climbing, you’ll look back at this little stalled phase and chuckle. You'll know you persevered, you learned, and you conquered. Your credit score might have paused, but your financial journey is just getting more exciting. So go forth, be brave, be smart, and get ready to see that score smile back at you. You absolutely got this, and a brighter financial future awaits!