Should I Pay Off My Student Loans All At Once: Complete Guide & Key Details

Hey there, fellow debt warrior! So, you're staring down those student loans, huh? Big life decision time! One of the big questions buzzing around your brain is probably: "Should I just blitz these bad boys and pay them off all at once?" It's a tempting thought, isn't it? Imagine that sweet, sweet freedom! But before you go liquidating your prized beanie baby collection (just kidding... mostly), let's dive into this whole "paying off student loans all at once" thing.

We're gonna break it down like a cheap cookie at a toddler's birthday party. No jargon, no confusing spreadsheets, just a friendly chat about what it means, if it's even possible, and if it's actually a smart move for your wallet and your sanity. Think of me as your friendly neighborhood finance whisperer, armed with coffee and a whole lot of empathy. We'll explore the nitty-gritty, the pros, the cons, and help you figure out if going all-in is your financial superhero origin story or a recipe for ramen noodles for the next decade.

Let's get this party started, shall we? Grab your favorite beverage – mine's currently a slightly-too-sweet iced latte that's probably costing me the equivalent of a small country’s GDP – and let's untangle this student loan beast together.

The Big Question: "Should I Pay Off My Student Loans All At Once?"

Okay, so you've got this lump sum of cash burning a hole in your pocket. Maybe it's a sweet inheritance, a killer bonus at work, or you've been a financial ninja for years, squirreling away every spare penny like a chipmunk preparing for a nuclear winter. Whatever the reason, you're contemplating: should I just yeet the entire loan balance at my lender and be done with it?

It sounds glorious, doesn't it? No more monthly payments, no more interest accruing, just a big, fat, zero staring back at you where your student loan balance used to be. It’s like that feeling you get when you finally finish a ridiculously long book series – pure, unadulterated relief. But hold your horses, cowboy/cowgirl! While the idea is undeniably attractive, it's not as simple as a quick flick of the wrist.

There are a few crucial things we need to unpack before you go making any hasty decisions. We’re talking about your financial health, your future goals, and whether this "all at once" strategy is actually a good idea or just a shiny, tempting distraction. Let's peel back the layers, shall we?

What "Paying Off All At Once" Actually Means

First things first, let's clarify what we're even talking about. "Paying off all at once" usually means using a significant chunk of savings, a windfall, or even tapping into investments to eliminate your entire student loan balance in one go. This isn't about making extra payments here and there; it's about wiping the slate clean, kaput, finito!

So, if you've got, say, $30,000 in student loans, and you suddenly come into $30,000 (or more!), you could theoretically send that entire amount to your loan servicer. Boom! Done. No more calls from Sallie Mae (or whoever your loan fairy godmother is).

It's like the ultimate mic drop in the world of debt. But like any mic drop, you gotta make sure you're not dropping it on your own foot. We need to consider the surrounding landscape of your finances before we go all rockstar on this debt.

The "Why" Behind the All-At-Once Dream (The Upsides!)

Let's be honest, the allure of paying off student loans all at once is strong. There are some seriously compelling reasons why people even consider this. Let's dive into the sunshine and rainbows, shall we?

1. Say Goodbye to Interest!

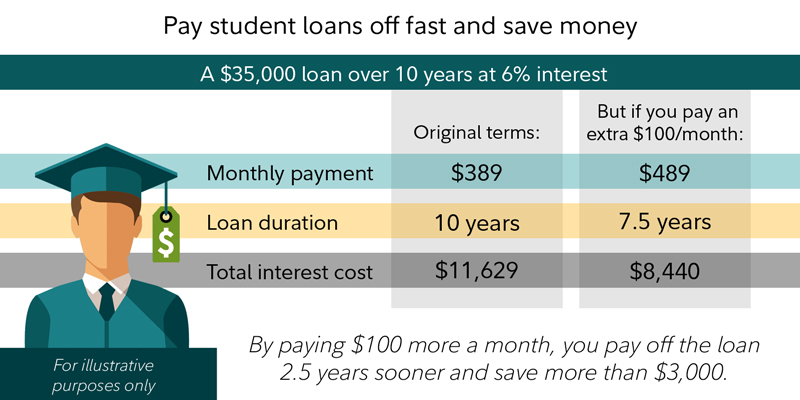

This is probably the biggest and most attractive benefit. Student loan interest, especially over the long haul, can add up to a seriously impressive (and often infuriating) sum. By paying off your loans in one go, you eliminate all future interest payments. Think of all the money you're saving! That's like finding a twenty-dollar bill in a coat pocket you haven't worn since last winter, but times a thousand. It’s a financial win!

Imagine your loan balance: $30,000 at 5% interest over 10 years. Over those 10 years, you'd pay approximately $8,100 in interest. That’s a whole lot of extra cash just for the privilege of borrowing! By paying it off now, that $8,100 stays in your pocket. Hello, fancy vacations or a down payment on a house!

2. The Ultimate Peace of Mind

Let's talk about the mental game. Student loan debt can feel like a constant weight on your shoulders. Knowing you have this obligation hanging over you can be stressful, even if you're making your payments on time. Paying it off completely can bring an unparalleled sense of freedom and peace of mind. No more monthly reminders, no more checking your balance with a slightly anxious sigh. It's like decluttering your financial life – pure bliss!

This mental freedom is HUGE. It can free up your brain space to focus on other things, like growing your career, enjoying your hobbies, or just sleeping soundly at night without that little voice whispering about loan payments. It’s a psychological superpower, if you ask me.

3. Boost Your Debt-to-Income Ratio (Hello, Future Loans!)

This is a bit more technical, but super important if you're thinking about major life events like buying a house or a car. Your debt-to-income ratio (DTI) is a crucial factor lenders look at. When you eliminate your student loans, your DTI plummets. This can make it much easier to qualify for other loans in the future and potentially even get you better interest rates.

So, if you've been dreaming of homeownership, paying off those student loans in one fell swoop could be the golden ticket to making that dream a reality sooner rather than later. It's like giving your credit score a superhero cape.

4. Simplicity is Bliss

Let's face it, managing loans can be a headache. You've got your servicer, your statements, your payment dates... it's a whole administrative circus. Paying off your loans all at once eliminates this administrative burden entirely. No more tracking payments, no more worrying about missing a due date. It's one less thing to juggle in your busy life. Simple, clean, and oh-so-satisfying.

Think of it as decluttering your digital life. All those apps, all those logins, all those notifications... gone! Just the sweet, sweet simplicity of financial liberation.

The Flip Side of the Coin: When "All At Once" Might NOT Be the Best Idea (The Downsides!)

Now, before you go emptying your entire savings account like a wild prospector striking gold, we need to pump the brakes and look at the potential pitfalls. Because, like that tempting slice of cake after a huge meal, sometimes the best-looking option isn't the healthiest one.

1. Depleting Your Emergency Fund (The BIGGEST Risk!)

This is the number one reason why paying off student loans all at once can be a risky move for many. Your emergency fund is your financial safety net. It's your cushion for unexpected job loss, medical emergencies, car breakdowns (which always seem to happen at the worst possible moment, don't they?), or any other life curveball. If you use all your savings to pay off loans, you're left financially vulnerable.

Imagine this: you pay off your loans, feel amazing, and then BAM! You lose your job the next month. Without an emergency fund, you're in a really tough spot, scrambling to cover rent, food, and all those other bills. It's like bravely sailing into a storm without a life raft. Not ideal.

A general rule of thumb is to have 3-6 months of living expenses saved. If paying off your loans would wipe this out, it's a major red flag. Your future self will thank you for having that safety net.

2. Missing Out on Investment Opportunities

Let's talk about your money's potential to make more money. If you have a significant amount of cash just sitting there, it could potentially be earning more through investments than you're paying in student loan interest. Especially if your student loan interest rates are relatively low.

For example, if your loans have a 4% interest rate, but you could potentially invest that money and earn an average of 7% in the stock market over the long term, you're actually losing out on potential gains by paying off the loan early. It's like choosing to eat a plain cracker when there's a whole buffet of delicious food waiting for you.

This is where the concept of the "opportunity cost" comes into play. You're sacrificing the potential for higher returns elsewhere by tying up that money in a debt that might have a lower rate than your potential investment returns.

3. The "What Ifs" of Life

Life is unpredictable. You might have plans for a down payment on a house, starting a business, or even just a really epic vacation. If you tie up all your liquid cash in student loans, those other financial goals might have to be put on hold. It's a trade-off, and you need to decide if the trade is worth it for you.

Sometimes, having that cash readily available for a unique opportunity is more valuable than being completely debt-free. It's like having a secret stash of superpower ingredients for whatever life throws at you.

4. Cash Flow Crunch

Even if you can pay off your loans all at once, doing so might leave you with very little cash for your day-to-day expenses. If you're not careful, you could find yourself living paycheck to paycheck, which can be just as stressful as having debt, if not more so.

This is especially true if your income isn't super stable or if you have other significant financial obligations. You want to ensure you have enough breathing room for your regular bills and unexpected small expenses.

Key Details to Consider Before You Make the Leap

So, you've weighed the pros and cons. You're still thinking about that all-at-once payment, but you want to make sure you're doing it the smart way. Excellent! Let's dig into the nitty-gritty details that will help you make an informed decision.

1. Know Your Interest Rates

This is paramount, folks! Compare your student loan interest rates to potential investment returns and even savings account rates.

- High Interest Rates (5%+): If your loans have high interest rates, paying them off all at once becomes a much more attractive option, as the interest savings will be significant. It's like taking candy from a baby (a very expensive baby, that is).

- Low Interest Rates (Below 4-5%): If your rates are on the lower side, you might be better off making minimum payments and investing the difference, as you could potentially earn more through investments.

Don't forget to look at the types of loans you have. Federal loans often have fixed rates, while private loans can vary. Knowing this will help you make the best choice.

2. Assess Your Full Financial Picture

This is where you put on your financial detective hat. Take a serious look at your entire financial situation. This includes:

- Your Emergency Fund: Do you have at least 3-6 months of living expenses saved? If not, prioritize building this up before paying off debt.

- Other Debts: Do you have high-interest credit card debt? It generally makes more sense to tackle that before student loans.

- Your Income Stability: Is your job secure? Do you have a side hustle? The more stable your income, the more comfortable you might be with a smaller emergency fund.

- Your Future Goals: Are you planning to buy a house soon? Save for a wedding? Travel the world? How will paying off student loans impact these plans?

It's like planning a heist – you need to know all the variables before you make your move.

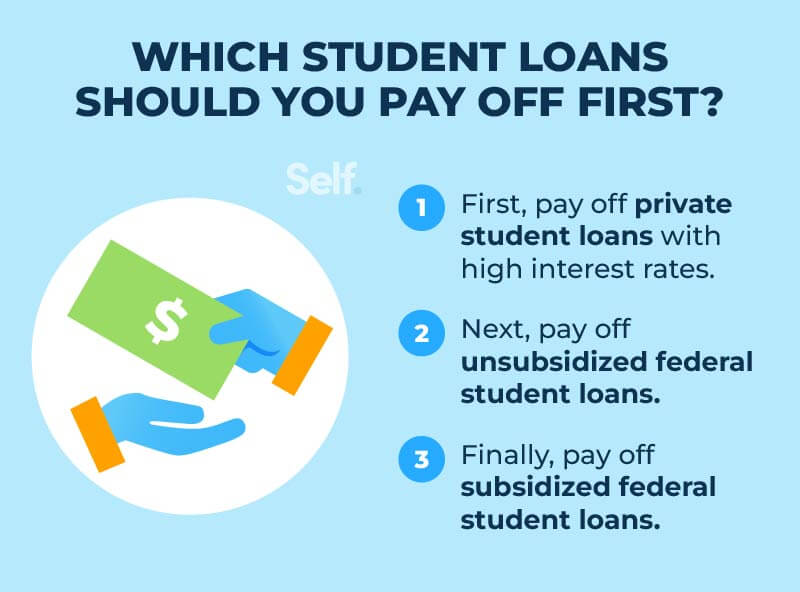

3. Understand Your Loan Types

Are these federal loans or private loans? This matters!

- Federal Loans: These often come with more flexible repayment options, deferment, and forbearance, which can be lifesavers if you hit a rough patch. If you pay them off all at once, you lose access to these protections.

- Private Loans: These can be less flexible and might have stricter terms. If you have high-interest private loans, paying them off might be a higher priority.

Also, check if you have any loan forgiveness programs you're working towards (like Public Service Loan Forgiveness). If so, paying them off early might be a terrible idea! You'd be forfeiting potential forgiveness, which could be worth tens of thousands of dollars.

4. Explore Alternatives to "All At Once"

Even if you have the lump sum, it doesn't have to be all or nothing. Consider these strategies:

- Targeted Extra Payments: Instead of paying it all off, you could make a large extra payment, significantly reducing your balance and saving on interest, without completely draining your savings.

- Prioritize High-Interest Loans: If you have multiple loans, use your lump sum to aggressively pay down the one with the highest interest rate first (the "debt avalanche" method).

- Automate Extra Payments: Set up automatic extra payments from your bank account so you're consistently chipping away at your debt without thinking about it.

It's about finding the sweet spot that balances debt reduction with financial security and future goals.

The Verdict: Should You Go All-In?

So, after all this talk, the million-dollar question remains: should you pay off your student loans all at once? The honest answer is: it depends. There’s no one-size-fits-all financial magic spell here.

If you have a substantial emergency fund, stable income, high-interest loans, and no immediate need for that lump sum for other critical goals (like a down payment), then paying off your student loans all at once could be a fantastic move. It can be incredibly empowering and save you a ton of money in the long run.

However, if paying them off would drain your emergency fund, leave you cash-strapped, or sacrifice other crucial financial goals, then it's probably not the best strategy for you right now. In that case, focus on building your safety net, making consistent extra payments, and exploring other debt-reduction strategies.

Think of it this way: financial health is like a marathon, not a sprint. Sometimes, the smartest move is to pace yourself, stay hydrated (with savings!), and make sure you have the right gear (a solid emergency fund) before you go for the gold medal (debt freedom).

Ultimately, the decision is yours. Weigh the benefits against the risks, consider your personal circumstances, and choose the path that makes you feel most confident and secure. No matter what you decide, the fact that you're actively thinking about your student loans and looking for the best way forward is a huge win in itself. You've got this!

And hey, once those loans are gone (or significantly reduced!), you'll feel an incredible sense of accomplishment. Imagine that feeling of liberation! It’s a fantastic stepping stone towards whatever financial dreams you have next. Keep crushing it!