Should You Buy Whole Life? Pros, Cons, And Better Alternatives

Hey there, living your best life? We're talking about those big decisions that can feel as complex as assembling IKEA furniture without the instructions. Today, we're diving into the world of whole life insurance. Is it the financial equivalent of a perfectly brewed cup of coffee, warming and reliable? Or is it more like a fancy gadget you bought on impulse that you're not quite sure how to use? Let's break it down, chill vibes only.

You've probably heard the term "whole life insurance" tossed around. It sounds... well, whole. Like it covers everything. And in a way, it does. It's a type of permanent life insurance, meaning it’s designed to stay with you for your entire life, as long as you keep paying the premiums. Unlike term life insurance, which is like renting an apartment (it expires after a set term), whole life is more like owning a home. It’s yours for the long haul.

The Allure of "Forever" Coverage

So, what’s the big deal? The primary perk of whole life is its guaranteed death benefit. This means your beneficiaries are guaranteed to receive a payout, no matter when you pass away. Think of it as a financial safety net that’s always in place, a comforting thought in our unpredictable world. It’s like having a best friend who always promises to have your back, no matter what life throws at them.

But wait, there's more! Whole life insurance policies also build cash value over time. This isn't just some abstract concept; it's actual money that grows on a tax-deferred basis. You can potentially borrow against this cash value or even withdraw it if you’re in a pinch. It’s like a secret piggy bank that gets fatter with age, ready to help you out in a financial bind. It’s the kind of thing that makes financial planners nod sagely, like they’ve just discovered the meaning of life… or at least the meaning of their job.

This cash value grows at a guaranteed rate, which adds another layer of predictability. No stock market rollercoasters here, folks. It’s a steady, reliable climb. Some policies even pay dividends, which are essentially a share of the insurance company’s profits. These dividends can be used to further increase your cash value, pay down premiums, or even be taken as cash. It’s like finding a forgotten $20 bill in your winter coat – a pleasant surprise!

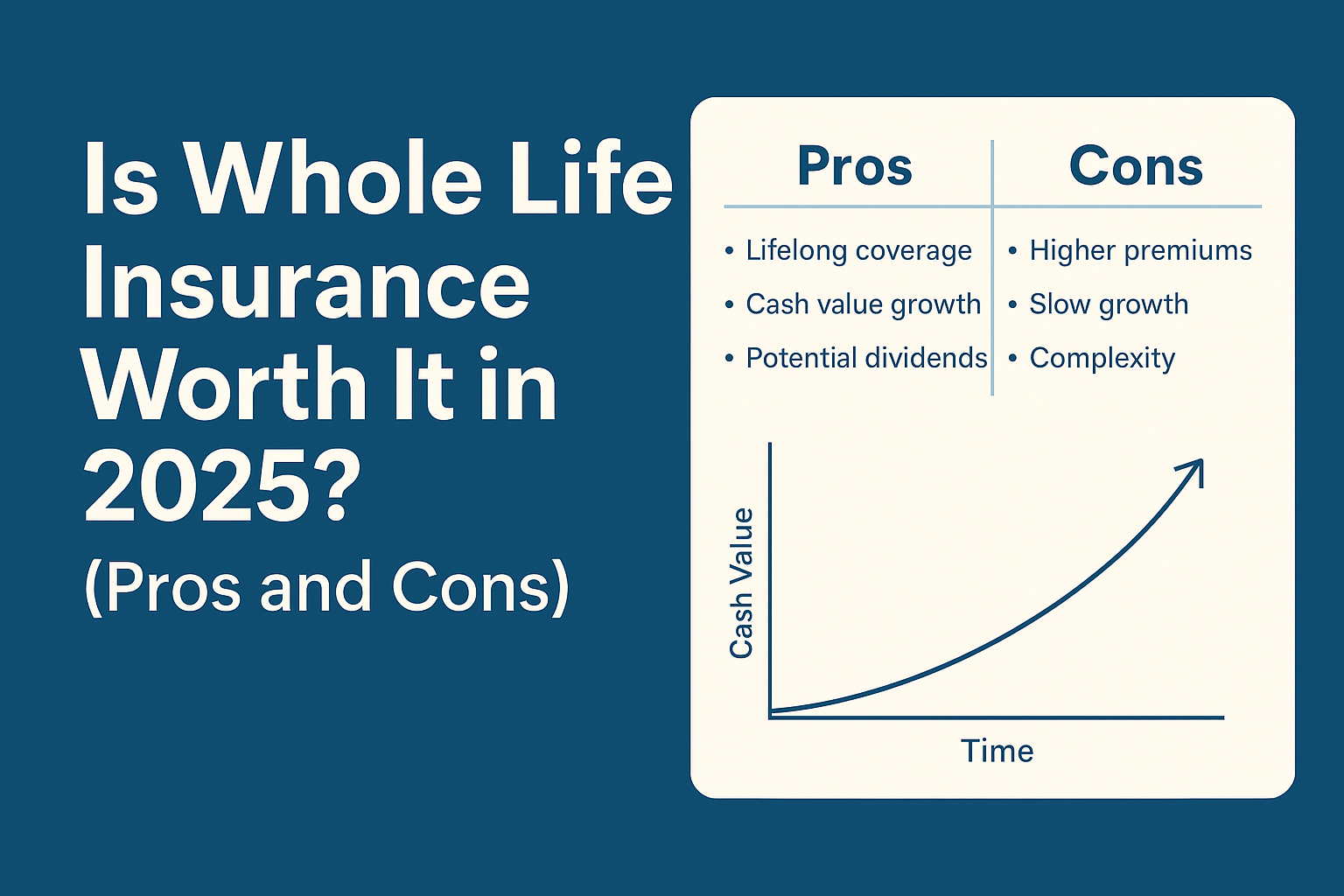

Let's Talk "Pros": The Good Stuff

Let's round up the advantages, shall we?

- Lifelong Coverage: As we mentioned, it's there for you, always. Peace of mind, check!

- Guaranteed Death Benefit: Your loved ones are protected. No ifs, ands, or buts.

- Cash Value Growth: A growing nest egg that’s sheltered from taxes. Think of it as a retirement bonus that keeps on giving.

- Predictable Premiums: For most whole life policies, your premium payments remain the same throughout your life. No nasty surprises in your mail.

- Potential Dividends: Extra earnings that can boost your policy’s value. It’s like getting a little extra sprinkle on your ice cream.

The predictability factor is huge. In a world where interest rates fluctuate and stock markets can give you whiplash, having a financial product that’s stable can be incredibly appealing. It’s the financial equivalent of a comfy pair of slippers – reliable and always there for you.

And Now, The "Cons": The Not-So-Good Stuff

Alright, let's bring it back down to earth. While whole life sounds pretty sweet, it’s not all sunshine and rainbows. The biggest hurdle for most people? The price tag. Whole life insurance premiums are significantly higher than those for term life insurance. We’re talking potentially several times more expensive for the same death benefit amount. It’s like comparing the cost of a fancy espresso latte to a good old-fashioned drip coffee. Both get the job done, but one comes with a much heftier price.

This higher cost means you might be paying for coverage you don't necessarily need for your entire life. If you're young and healthy, the chances of you needing your life insurance payout in your early years are relatively low. You might be better off investing that extra premium money elsewhere, where it could potentially grow at a higher rate.

The cash value growth, while guaranteed, is often slower than what you could potentially achieve with market investments. The insurance company takes a chunk for administrative costs and fees, so your returns might not be as impressive as you’d hope. It’s like getting a recipe for a delicious cake, but the baker decides to keep a slice of the ingredients before they even start baking. You still get cake, but it’s not quite as big as you imagined.

Furthermore, if you surrender the policy early, you might not get back all the premiums you’ve paid. There can be surrender charges, which essentially penalize you for cashing out. It's like breaking a lease – you might owe a fee. This makes it less flexible if your financial situation changes dramatically.

Think of it this way: while term life is a contract for a specific period, whole life is a lifelong commitment. And like any long-term commitment, it’s worth considering if it truly aligns with your long-term goals and financial picture. It's not a one-size-fits-all kind of deal, and forcing it can feel like wearing shoes that are two sizes too small – painful and impractical.

Here are some of the downsides to keep in mind:

- High Premiums: Often much more expensive than term life insurance.

- Lower Potential Returns: Cash value growth can be slower than market investments.

- Less Flexibility: Surrendering early can result in losses.

- Complexity: Understanding all the riders and options can be a headache.

- "Over-Insuring": You might end up paying for coverage you won't need.

Are There Better Alternatives? Let's Explore!

Okay, so maybe whole life isn't singing your song. That's totally fine! The good news is, there are plenty of other financial instruments out there that might be a better fit for your lifestyle. Think of it like choosing your soundtrack for a road trip – you want something that matches your vibe.

Term Life Insurance: The Smart, Simple Choice

For many people, especially those who are younger and healthier, term life insurance is the reigning champion. It’s straightforward: you pay premiums for a set period (e.g., 10, 20, or 30 years), and if you pass away during that term, your beneficiaries receive the death benefit. Once the term is up, the coverage ends.

The beauty of term life is its affordability. You can get a substantial death benefit for a fraction of the cost of whole life. This frees up your other income to be invested in potentially higher-growth assets. It’s like getting a great deal on a concert ticket, leaving you with more cash for merch and snacks. You get the protection you need, when you need it most, without the long-term commitment or the higher price tag.

A fun fact? Term life insurance was popularized in the early 20th century, making life insurance more accessible to the average person. Before that, it was often seen as a luxury for the wealthy.

Investing the Difference: The DIY Approach

Here's a strategy that's gained a lot of traction: buy term life insurance for the protection you need, and then invest the difference in premiums you would have paid for whole life. This could be in low-cost index funds, ETFs, or even your company's 401(k).

The idea is that over the long term, your investments could potentially grow more than the cash value in a whole life policy. You have more control over your investments and can choose options that align with your risk tolerance and financial goals. It’s like being the chef of your own financial meal, choosing exactly which ingredients go into it.

This strategy requires a bit more discipline, as you have to actively manage your investments. But for those who are comfortable with it, it can be a powerful way to build wealth while still having adequate life insurance coverage.

Hybrid Policies: A Blend of Both Worlds

For those who like a bit of everything, there are also hybrid policies that combine features of both term and permanent life insurance. These can offer some cash value growth and a degree of lifelong coverage, but often with more flexibility and lower premiums than traditional whole life.

Think of them as the "everything bagel" of insurance – a little bit of everything you might want. They’re not as simple as term life, but they can be a good middle ground for some folks. It’s worth exploring these if you’re feeling a bit indecisive.

Making the Choice: What's Your Vibe?

So, should you buy whole life insurance? The answer, as with most things in life, is: it depends. Whole life insurance can be a valuable tool for certain individuals with very specific financial goals, such as estate planning or for those who have maxed out all other tax-advantaged retirement savings vehicles and are seeking guaranteed, lifelong coverage with a cash value component.

It’s often best suited for individuals with high net worth who are looking for a predictable way to leave a legacy or for those who have specific long-term care needs that a cash value component might address. It's the kind of product that might be recommended by a financial advisor when other boxes are already ticked.

However, for the majority of people, especially those looking for affordable protection during their working years, term life insurance is likely a more practical and financially savvy choice. It provides the essential death benefit without the high cost and complexity of whole life.

The key is to understand your own financial situation, your goals, and your risk tolerance. Don’t just buy something because it sounds fancy or because someone told you to. Do your research, ask questions, and consider consulting with a fee-only financial advisor who can offer unbiased advice.

Think about it like this: you wouldn't buy a sports car if you live in a town with terrible roads and your commute is just a few blocks. You'd choose something practical and reliable. Similarly, choose the insurance that fits your life, not the other way around.

A Little Reflection to Wrap It Up

As you navigate these financial waters, remember that insurance is just one piece of the puzzle. It’s about building a secure and fulfilling life, whatever that looks like for you. Whether it's the dependable rhythm of term life premiums, the steady build of your investment portfolio, or the peace of mind knowing your loved ones are cared for, it all contributes to your overall well-being.

Ultimately, the best financial decisions are the ones that align with your values and allow you to live your life with less stress and more joy. So, take a deep breath, sip your favorite beverage, and make the choice that feels right for your unique journey. Because at the end of the day, your life is your masterpiece, and you get to decide how to paint it.