Student Finance I'm Not Going To Year In Industry

Let’s be honest, the phrase “student finance” can send a shiver down even the most enthusiastic undergraduate's spine. It conjures images of spreadsheets, complex acronyms, and the existential dread of future debt. But what if I told you that navigating student finance doesn't have to be a soul-crushing ordeal? What if it could actually be… well, manageable? Especially if, like me, you're not planning on taking a "year in industry" and are instead powering through your degree in a more traditional, four-year sprint (or maybe a slightly more leisurely seven-year marathon, no judgment here).

Forget the glossy brochures promising glamorous internships and hefty salaries. My path is a little different. It's more about getting that degree, soaking up the university experience, and then figuring out the career side of things. And for that, student finance is our trusty sidekick, not the villain of our academic story. It’s about understanding the system, making it work for you, and avoiding unnecessary stress. Think of it as your personal finance fairy godmother, albeit one with a slightly bureaucratic wand.

The Great Unpacking: What's Actually In The Student Finance Pot?

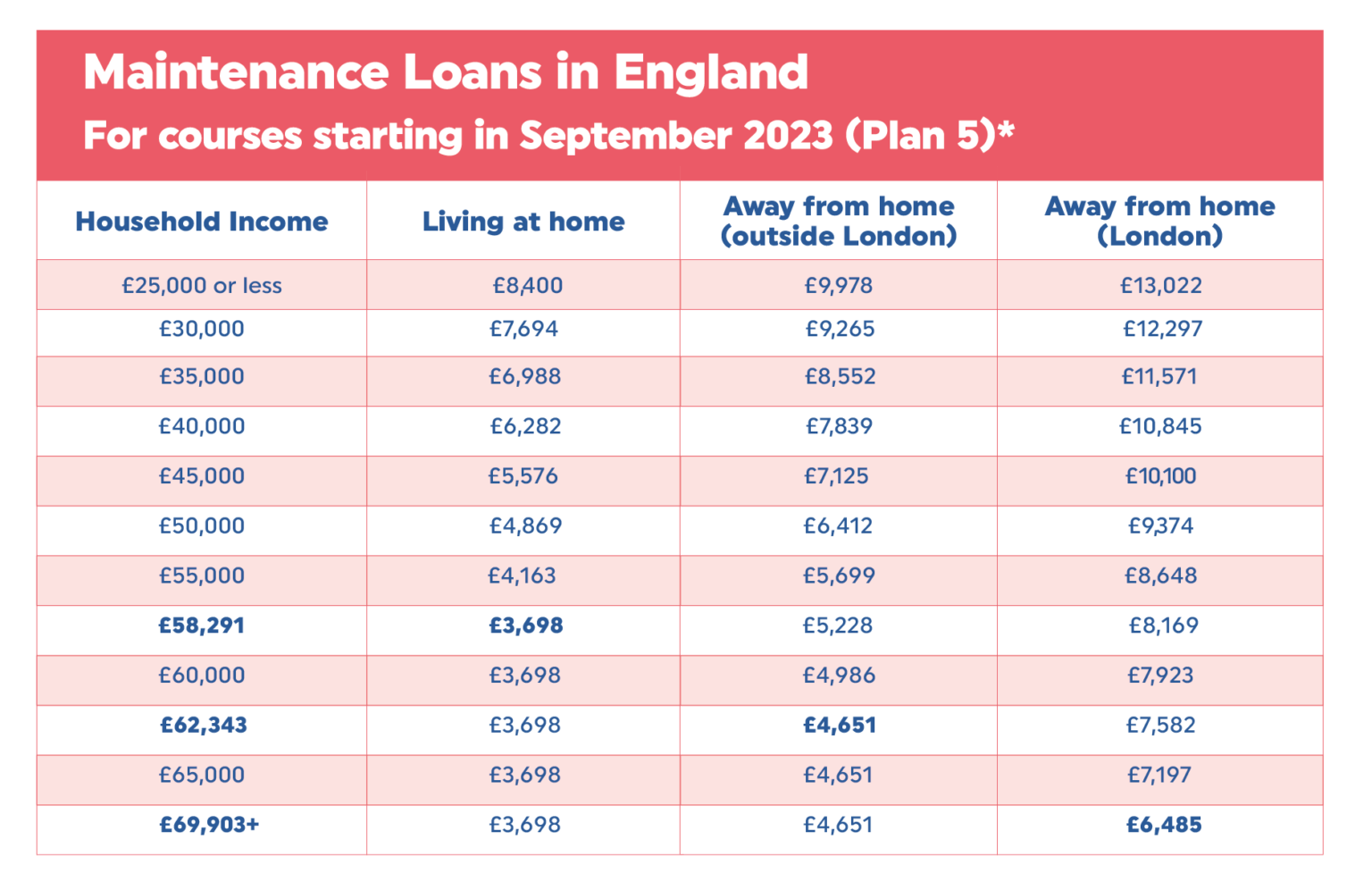

So, what are we actually talking about when we say "student finance"? For most UK students, it boils down to two main things: the tuition fee loan and the maintenance loan. It sounds simple enough, but there's a bit more nuance to it than meets the eye. These aren't just free handouts, obviously, but they are designed to help you focus on your studies without your bank account screaming in protest. The tuition fee loan covers the cost of your course, and it’s paid directly to your university. Pretty straightforward. The maintenance loan, however, is for your living costs – think rent, food, that occasional splurge on artisanal coffee, and, let's be real, the emergency taxi home after a particularly memorable Freshers' Week.

The amount of maintenance loan you get is based on your household income. This is where things can get a little bit tricky, and sometimes a bit unfair. The government assesses your family's income to determine how much support you'll receive. If your parents are rolling in it, you might get less. If they're living on beans on toast themselves, you'll likely get the maximum. It's all part of the grand, sometimes baffling, system. But hey, knowledge is power, and understanding this is the first step to maximizing your financial flow.

The "Not Going Into Industry" Advantage (Sort Of)

Now, for those of us who are skipping the year in industry – and there are many of us! – the financial landscape can look a tad different. A year in industry often means you’re earning a salary for that year, which can significantly reduce your reliance on loans. It’s a trade-off, right? You gain work experience, potentially a better graduate job offer, but you might also have a slightly smaller loan pile. For those of us forging a more direct path through our degrees, it means we’re likely relying on those student loans for the full duration of our studies. This isn't necessarily a bad thing; it's just a different route. It means we need to be extra savvy about how we manage our funds from day one.

Think of it like this: a year in industry is like a well-placed pit stop in a long race. We’re not stopping for that pit stop; we’re just going to keep our engine running smoothly and efficiently for the whole marathon. It requires a different kind of strategic planning, focusing on sustained financial health rather than a temporary boost. It’s about building good habits that will last long after graduation. And honestly, there's a certain pride in knowing you've navigated your studies without that extra year of earning potential. It’s a testament to resilience and smart budgeting.

Budgeting: Your New Best Friend (Even If You Don't Want It To Be)

Okay, I know, I know. "Budgeting" sounds about as exciting as watching paint dry. But hear me out. It's the secret weapon in the student finance arsenal. Without a budget, that maintenance loan can evaporate faster than a free pizza at a student union event. The key is to be realistic. Track your spending for a month. Every single coffee, every impulse eBay purchase, every night out. You'll be amazed at where your money is actually going. Use apps like Monzo or Revolut, or even a good old-fashioned spreadsheet. It’s not about deprivation; it’s about understanding and control.

Let's break it down. Your loan arrives, and it feels like a lottery win. Resist the urge to book that spontaneous trip to Ibiza. Instead, divide your loan into monthly chunks. That's your rent, your bills, your food, your social life. Allocate a set amount for "fun money" – the guilt-free spending. The rest goes towards the essentials. It’s about conscious spending, not extreme austerity. You can have a social life and still be financially responsible. It’s about making choices, like opting for a potluck with friends instead of a pricey restaurant, or finding those amazing student discounts. Think of it as a game: can you make your money stretch further and still have a good time? The answer is usually yes, with a little planning.

The "Hidden Costs" of Student Life

Beyond the big hitters like rent and food, student life comes with its own unique set of expenses. Textbooks, for example. Some can cost an arm and a leg. Look for second-hand copies, borrow from the library, or even see if your university has a digital resource library. Then there are society memberships, sports club fees, and the ever-present need for new stationery. These might seem small individually, but they add up. Factor them into your budget. Seriously, that £5 a week for coffee? That’s £20 a month. That’s a good chunk of your phone bill right there. Small sacrifices can make a big difference.

And let's not forget the social aspect. Student life is all about experiences, and often, those experiences involve spending money. But there are always ways to do it on a budget. Look for free events on campus, student nights at local pubs with cheaper drinks, or even organize your own themed nights in with friends. Think "Netflix and chill" with a homemade pizza, rather than a pricey cinema trip. It's about prioritizing what brings you the most joy. Maybe that's one big event a month, or several smaller, more affordable outings. The key is to have a plan, so you're not scrambling for cash when your friends suggest something fun.

Interest Rates: The Silent (But Not So Silent) Killer

Now, let's talk about interest. This is where student loans get a bit more intimidating. The interest rate on student loans can fluctuate, and it accrues from the moment you take out the loan. This is a crucial point that often gets overlooked. While you don’t have to start paying anything back until you’re earning a certain amount, that interest is ticking away. For those of us not aiming for a super high-flying, immediate graduate salary, understanding these rates and how they affect your total repayment is important. It’s not about panicking, but about being informed.

The government has different plans for how you repay your student loan, and the interest rate is tied to RPI (Retail Price Index). This means it can go up and down. While you're a student and for a period after, the interest rate is effectively the inflation rate plus a small amount. Once you leave university and start earning above the repayment threshold, the interest rate is usually RPI plus 3%. So, if inflation is high, your loan grows faster. It's a bit like a slow-moving snowball rolling down a hill. The longer you take to repay, the more you'll potentially end up paying in interest. This is where making voluntary overpayments, even small ones, can really make a difference in the long run. It’s like giving that snowball a gentle push uphill.

Making Your Loan Work Smarter, Not Harder

So, how do you make this loan work for you, not against you? Firstly, apply for the maximum maintenance loan you're eligible for. It’s there for a reason. Don't be shy! Once you have it, be disciplined. Stick to your budget. Secondly, if you do end up with any leftover funds at the end of a term, consider putting it into a savings account. Even a small amount of interest earned can offset some of the loan interest. It's a bit of financial alchemy. Thirdly, when you do start earning, aim to make voluntary repayments as soon as you can afford to. Even £20 a month can chip away at the principal and reduce the total interest you pay over time. It might not feel like much, but small, consistent efforts compound.

Think about it like a game of Tetris. You’re trying to fit all your financial needs into the available blocks. Sometimes, you get a whole row clear, and you have a bit of breathing room. That's when you can make those strategic overpayments. It’s not about depriving yourself of all joy; it’s about making smart moves that benefit your future self. And remember, the repayment threshold is quite high, so for many graduates, the payments are manageable. The goal isn't to be debt-free overnight, but to manage the debt responsibly.

Beyond Loans: Scholarships, Bursaries, and The Magic of Free Money

Now, let's talk about the real magic: free money! Scholarships and bursaries are often overlooked by students who think they're only for the academically gifted or the exceptionally talented. But that's simply not true. Universities and external organizations offer a wide range of financial support based on all sorts of criteria – your course, your background, your extracurricular achievements, even your postcode. It's about doing your research and putting in the applications. Don't let the fear of rejection stop you. The worst they can say is no!

Look at your university's website for their specific scholarship and bursary schemes. Often, they'll have dedicated teams to help you navigate the application process. Beyond university, there are countless trusts and charities that offer financial aid. Websites like "Scholarship Hub" or "Student Ladder" can be goldmines. Even if you don't think you qualify, apply anyway. You might be surprised. The effort you put into finding and applying for these awards can genuinely save you thousands of pounds and significantly reduce your reliance on loans. It’s like finding hidden Easter eggs in your academic journey!

The "Student Discount" Superpower

Let’s not underestimate the power of the student discount. It’s not just for pizza or movie tickets. Many retailers, from clothing brands to tech stores, offer student discounts. Always ask! Carry your student ID with pride, because it’s your golden ticket to savings. Signing up for student discount websites and apps can keep you updated on the latest deals. Think of it as a constant passive income stream – you’re just saving money instead of earning it directly.

Even if a place doesn't advertise a student discount, it's often worth politely asking. You might be surprised. And if they say no, you haven't lost anything! It's all part of being a savvy student. Embrace the discount culture; it's designed to help you navigate the cost of living while you're still studying and not yet earning a full-time salary. This isn't about being cheap; it's about being smart with your limited funds and making them go further, allowing you to enjoy more of your student experience without breaking the bank.

Reframing The Narrative: Student Finance as an Investment

Ultimately, student finance, even the loans, is an investment. It’s an investment in your future, in your education, and in the opportunities that a degree can unlock. The fact that you're not taking a year in industry doesn't make your financial journey any less valid or important. It just means you're approaching it with a different strategy. It requires diligence, a bit of foresight, and a willingness to be actively involved in your financial well-being.

When you think about it, that loan is a temporary bridge to a more rewarding career and a more informed life. It’s a tool, not a trap. And by understanding it, budgeting effectively, and exploring all the free money avenues, you can ensure that this bridge is as smooth and stress-free as possible. So, ditch the dread, embrace the practicality, and remember that you’ve got this. Your degree is within reach, and so is a manageable financial future. It’s all about making informed choices, one manageable step at a time.

Every time I see that notification from my banking app telling me my student loan has landed, I don't see a mountain of debt. I see the rent paid for another month, the groceries stocked, and maybe, just maybe, that ticket to see my favourite band. It’s not just about the abstract concept of student finance; it's about the tangible reality of affording the life I want to live now, while I build towards the life I want to live later. It’s about the small wins, the conscious choices, and the quiet confidence that comes from knowing you’re in control, even when the numbers look a little daunting. And that, my friends, is a feeling worth more than any interest rate.