Tax Penalty For Early Roth Ira Withdrawal

Hey there, money explorers! Ever wondered about those super-powered savings accounts called Roth IRAs? They're like a secret treasure chest for your future. But sometimes, life throws us a curveball, and we might need to tap into that treasure early. That's where things get a little… spicy!

Think of your Roth IRA as a magical money plant. You nurture it, and it grows tax-free for retirement. It's pretty awesome, right? But if you go digging up those roots before the plant is fully mature, well, the garden gnomes (aka the tax folks) might not be too pleased.

So, let's chat about the "early withdrawal penalty" for a Roth IRA. It sounds a bit like a stern librarian telling you to shush, but it's more about understanding the rules of the game. It's not a total disaster, but it's definitely something to be aware of!

The most exciting part? It's not always a black-and-white "gotcha!" situation. There are actually some sneaky, yet totally legit, ways to get your hands on your Roth IRA money without the sky falling down. It’s like finding a secret passage in a castle!

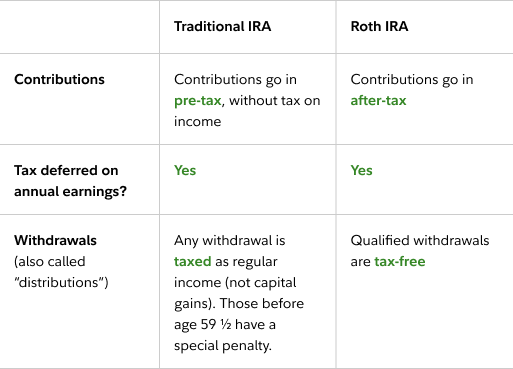

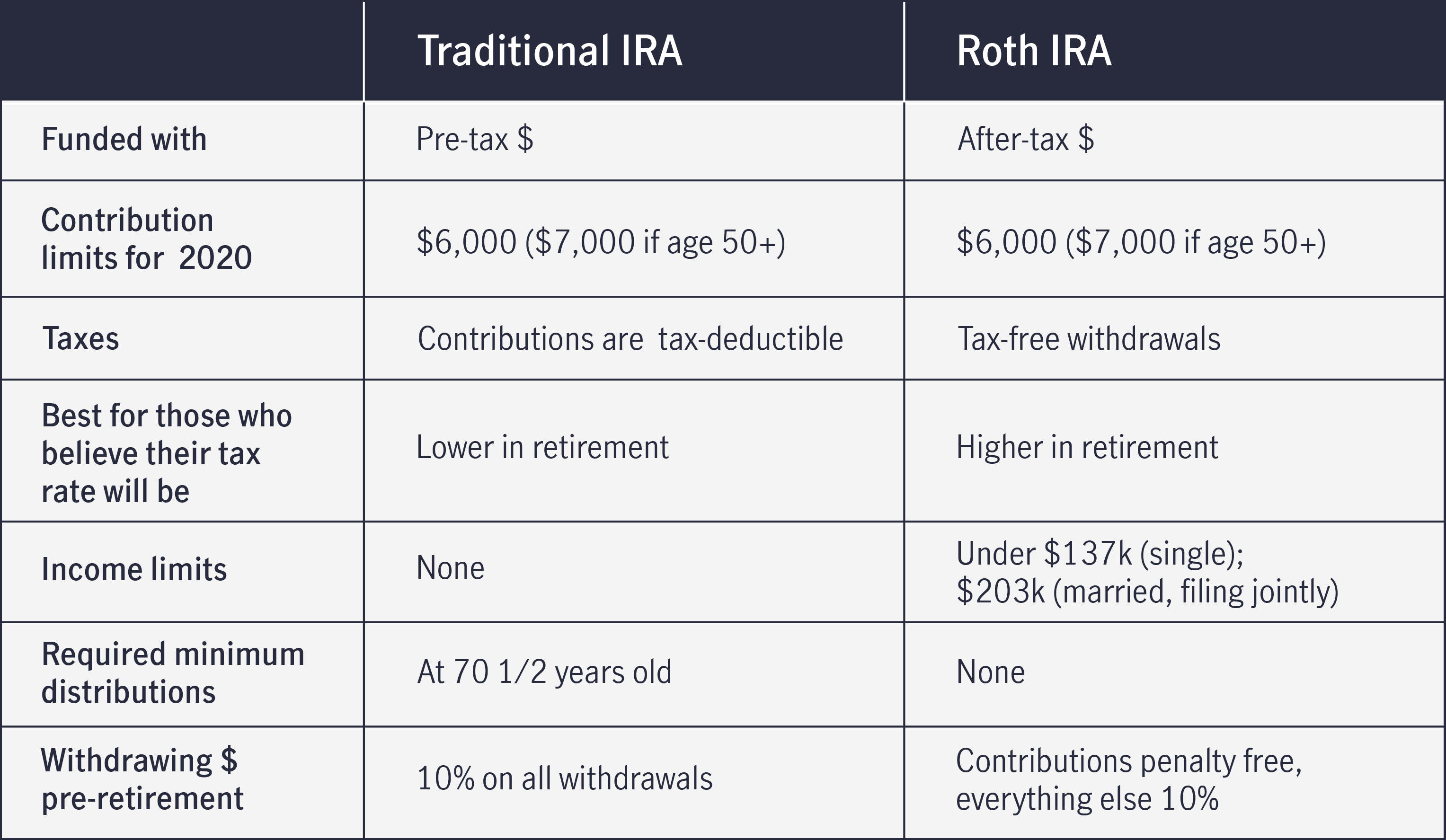

First off, let's talk about contributions. These are the dollars you initially put into your Roth IRA. The super cool news is that you can almost always take out your contributions, tax-free and penalty-free, whenever you darn well please. It's like a built-in emergency fund!

Imagine this: you've been diligently saving in your Roth IRA. Life happens, and suddenly you need cash for, say, a down payment on a house or an unexpected medical bill. You can usually just reach in and grab those contribution dollars. Ta-da! No fuss, no muss. It’s like a magic trick that saves the day.

Now, this is where it gets a little more nuanced, like deciphering an ancient map. The earnings – that's the magical growth your money has achieved – are a different story. Taking out earnings early can sometimes come with a little price tag.

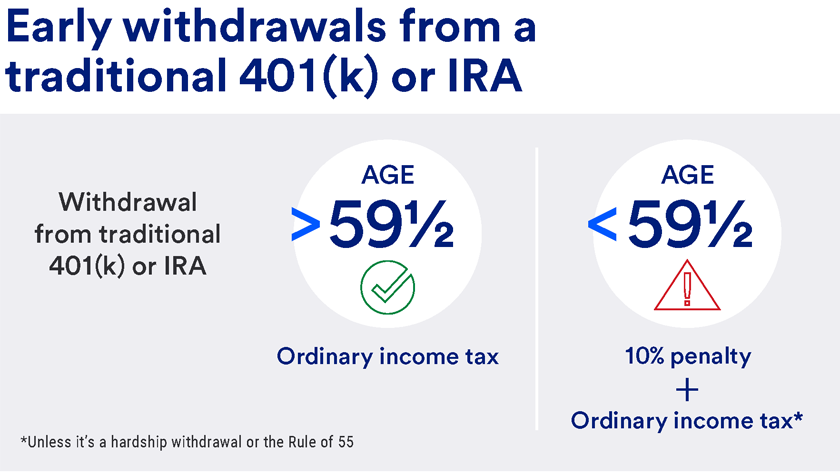

The standard rule of thumb is that if you're under age 59 ½ and withdraw your Roth IRA earnings before the account has been open for at least five years, you might face a 10% penalty. Plus, you'll likely owe regular income tax on those earnings. Bummer, right? It’s like finding out the dragon guarding the treasure also wants a bite of your gold.

But wait, don't close the book just yet! This is where the plot thickens, and the adventure truly begins. The IRS, bless their bureaucratic hearts, has included some epic "get out of jail free" cards, or as they call them, qualified distributions.

One of the most celebrated exceptions is for a first-time home purchase. If you need to buy your very own humble abode, you can withdraw up to $10,000 of your Roth IRA earnings penalty-free. Yes, you read that right! That's a substantial chunk of change to help you unlock your dream home. It's like the fairy godmother of retirement accounts!

Another thrilling possibility is using your Roth IRA for qualified higher education expenses. This can cover tuition, fees, books, and even room and board for yourself, your spouse, children, or grandchildren. So, if you're looking to boost your brainpower or help a loved one get smarter, your Roth IRA can be a secret scholarship fund.

Then there are the more somber, but still important, exceptions. If you become permanently disabled, the 10% penalty on earnings often goes out the window. It's a compassionate clause for those facing serious life challenges. The universe sometimes offers a gentle hand when things get tough.

And, in the unfortunate event of the account holder's death, beneficiaries can often inherit the Roth IRA and withdraw the funds without penalty. The money can then be used to cover final expenses or support loved ones. It's a way to ensure your hard-earned savings can still provide for your family.

There are also other less common but still valid reasons, like using the funds for a $500 qualified disaster relief payment or for certain unreimbursed medical expenses exceeding a percentage of your Adjusted Gross Income (AGI). It’s like a series of bonus rounds in a video game, each unlocking a new perk.

The key to unlocking these exceptions often lies in understanding the five-year rule. As mentioned, your Roth IRA needs to be open for five years, starting from January 1st of the first tax year you made a contribution, before you can withdraw earnings penalty-free for most non-qualified reasons. This rule is like the guardian of the treasure chest – you need to show it you've been a loyal keeper for a good while.

So, why is this whole "early withdrawal penalty" thing so fascinating? It's the inherent tension! We love the idea of a secure future, but life is unpredictable. The Roth IRA's flexibility, with its specific rules and exceptions, makes it a dynamic financial tool. It’s not just a savings account; it’s a strategic ally.

It’s the thrill of knowing there are ways to navigate unexpected financial waters without sinking your entire ship. It's about empowerment and having options. It’s like having a Swiss Army knife for your money!

Think of it as a puzzle. You’ve got your contributions, your earnings, the five-year clock, and a whole host of qualifying events. Putting all those pieces together to see how you can access your money without the dreaded penalty is incredibly satisfying. It’s like solving a riddle left by a wise old sage.

And the best part? You get to be the detective! Learning these rules and understanding how they apply to your unique situation makes you a more informed and confident financial navigator. It's a journey of discovery, and the rewards are not just monetary, but also in peace of mind.

So, instead of shying away from the idea of early Roth IRA withdrawals, get curious! Dive into the details. Understand your contributions from your earnings. Get familiar with the five-year rule. And most importantly, know about the amazing exceptions like home purchases and education.

It’s not about trying to cheat the system. It’s about understanding the ingenious design of the Roth IRA and how it can truly work for you, not just in retirement, but in life's unexpected moments too. It’s a testament to smart financial planning that offers both long-term security and short-term adaptability.

So, go on, be a financial adventurer! Explore the ins and outs of your Roth IRA. You might be surprised at the hidden pathways and secret bonuses you uncover. Happy saving, and happy navigating!