What Do Mortgage Lenders Look At On Bank Statements

So, you're dreaming of that little patch of heaven? Maybe a cozy starter home, a bigger place for your growing family, or even a sweet vacation spot to escape the daily grind. That's fantastic! And chances are, you're going to need a mortgage to make it happen. Now, when you walk into a mortgage lender's office (or, more likely these days, navigate their website), it can feel a bit like stepping into a doctor's waiting room – a little nerve-wracking, and you're not quite sure what they'll discover. One of the biggest things they'll want to peek at? Your bank statements.

Now, before you start picturing them squinting at every single coffee run and impulse Amazon purchase, let's take a deep breath and demystify this. Think of your bank statement as your financial diary. It’s a record of your money’s journey, and lenders want to understand your story. They're not judging your avocado toast habit, but they are looking for signs that you're a responsible borrower who can handle those monthly payments.

What Exactly Are They Looking For?

Imagine you're hiring a babysitter. You wouldn't just ask if they think they can handle your energetic toddlers. You'd probably want to see a little more – maybe some references, a quick chat about their experience, and a general sense of their reliability. Mortgage lenders do something similar with your bank statements. They're essentially looking for a few key things:

1. Consistent Income: The Steady Beat of Your Financial Life

This is a biggie. Lenders want to see that you have a reliable source of income coming in, and that it's generally consistent. Think of it like a favorite song on repeat – you know it's going to play, and it’s always there. They'll look at your pay stubs, of course, but your bank statements help paint a fuller picture.

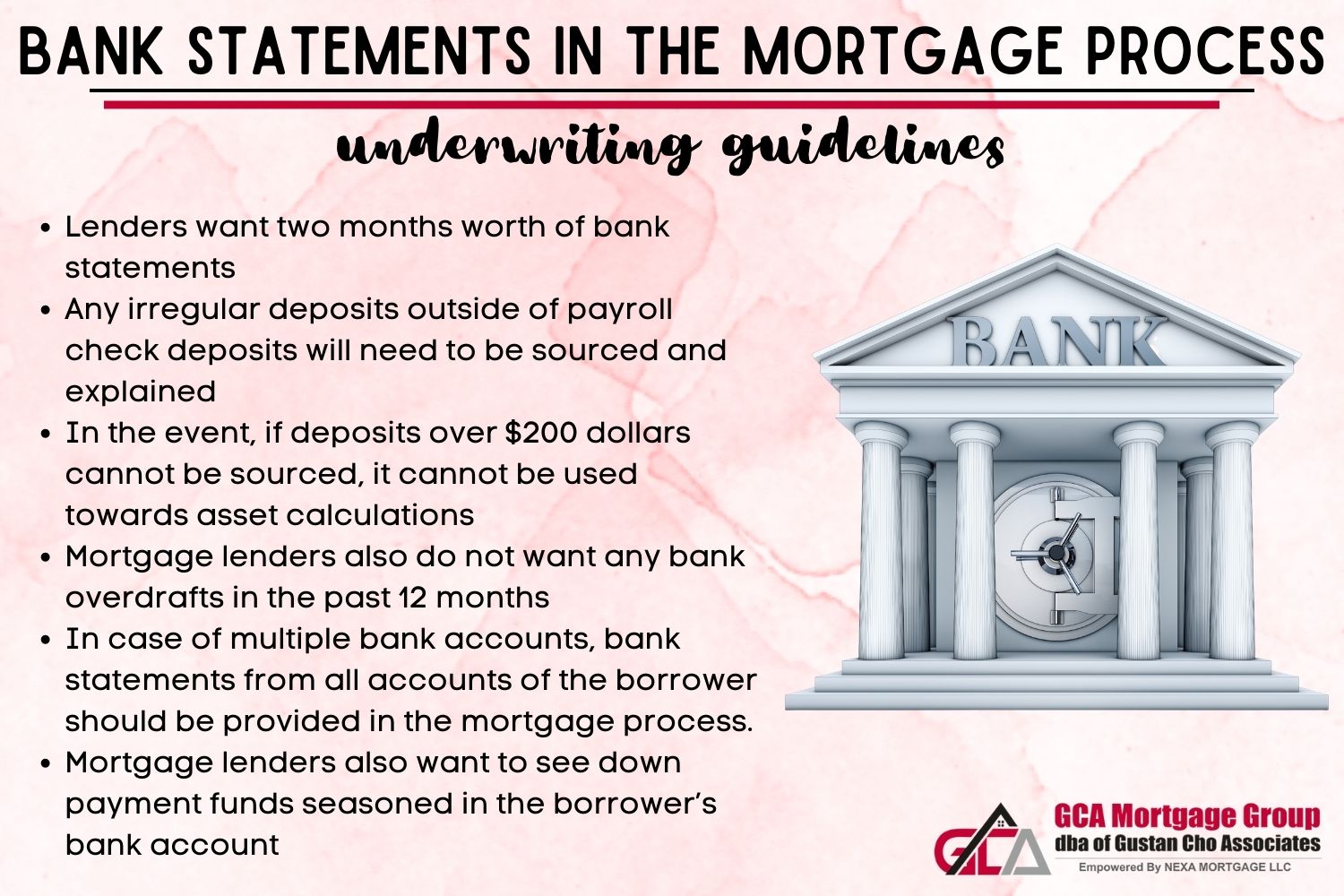

If you get paid weekly or bi-weekly, they'll want to see that pattern. If you're self-employed, they’ll be looking for those irregular but recurring deposits from clients. What they don't want to see is a wild rollercoaster of income. For instance, imagine you have a month where you get a huge bonus, and then the next month is crickets. That can raise a red flag. Lenders like predictability. It helps them assess your ability to make mortgage payments month after month, year after year.

Let's say you're a freelance graphic designer. Your bank statement might show a deposit from "Client A Designs" one month, and then a different amount from "Local Biz Marketing" the next. That's perfectly normal for a freelancer! Lenders understand that. What they'd be concerned about is a month with a massive $10,000 deposit, followed by two months with absolutely nothing. That’s the kind of irregularity that makes them pause and think, "Hmm, how will they manage the mortgage when income is so unpredictable?"

2. Your Spending Habits: Are You Living Within Your Means?

This is where those daily transactions come into play. Lenders are looking at how you manage your money. Are you living paycheck to paycheck, or do you have a bit of breathing room? They’re not going to judge your Netflix subscription or your weekly pizza night, but they are interested in patterns.

Think of it like this: If you're packing a picnic for a long hike, you want to make sure you have enough sandwiches and water, right? You wouldn't want to discover halfway up the mountain that you only packed one tiny granola bar. Lenders are checking if you have enough "food" (money) to last the "hike" (your mortgage term).

They'll be looking at things like:

- Regular Bills: Do you consistently pay your rent, car payments, and credit card bills on time? This shows responsibility.

- Large, Unusual Transactions: A sudden, massive withdrawal could be concerning. Did you buy a new car without a loan? Did you suddenly cash out a significant investment? They’ll want to understand these.

- Overdrafts: Consistently bouncing checks or going into overdraft is a big no-no. It signals that you’re living on the edge financially.

- "Unusual" Deposits: While they want to see consistent income, they also want to understand where sudden influxes of cash come from. Gifts? A loan from a friend? They’ll want to know the source, especially if it’s a large sum.

Imagine seeing a deposit of $5,000 with a note that says "Grandma's Birthday Gift." That's usually fine, but lenders might ask for a gift letter to confirm it’s not a loan you need to repay. On the flip side, if there’s a massive withdrawal, they might ask, "Hey, what happened to all that money?" They’re just trying to ensure you haven’t depleted your savings for something that might put your future mortgage payments at risk.

3. Your Savings: The Rainy Day Fund

Everyone has those unexpected expenses. Your car breaks down, your washing machine decides to take a permanent vacation, or you have a medical emergency. Having a savings account is like having an umbrella for a rainy day – it’s there to protect you when things go sideways. Lenders love to see that you have a healthy savings balance.

It shows you're planning for the future and have a buffer. They'll look at how much you’re consistently saving over time. It's not about having a million dollars stashed away, but about demonstrating a pattern of putting money aside. This is often referred to as your "reserves."

Think of it as a chef prepping for a busy dinner service. They have all their ingredients ready, their stations organized, and a bit of extra in the pantry just in case. Lenders want to see that you have your financial pantry stocked, so to speak. A few months’ worth of mortgage payments in savings is often a very good sign.

Let’s say your bank statement shows you’re consistently transferring $300 from your checking to your savings account each month. That’s excellent! It shows discipline and foresight. If, however, your savings account is always hovering at zero, it might make a lender a little hesitant. They want to know that if the unexpected pops up, you won't be completely derailed.

Why Should You Care?

This might all sound a bit tedious, but understanding what lenders look for on your bank statements is incredibly empowering. It's not about them being nosy; it’s about them assessing risk. And by understanding their perspective, you can put yourself in the best possible position to get approved for the mortgage you need.

Think of it like preparing for a job interview. You research the company, you practice your answers, and you make sure your resume is polished. Doing the same with your finances before approaching a mortgage lender is just smart planning. It can mean the difference between a smooth, straightforward process and a mountain of questions and potential rejections.

Here’s why it’s worth paying attention:

- Better Loan Terms: When you demonstrate good financial habits, lenders are more likely to offer you better interest rates and more favorable loan terms. This can save you tens of thousands of dollars over the life of your mortgage. That's more money for dream vacations, home renovations, or just plain enjoying life!

- Faster Approval: Having your financial ducks in a row means you can provide clear and concise information. This speeds up the approval process, getting you closer to that dream home faster. No one wants to be stuck in limbo!

- Less Stress: Knowing you’re presenting yourself well financially reduces a lot of the anxiety associated with applying for a mortgage. It’s like going into an exam knowing you’ve studied – you’ll feel more confident and less stressed.

A Little Prep Goes a Long Way

So, what can you do? It’s simpler than you might think!

- Review Your Statements: Take a look at your bank statements from the last few months. See the patterns? Are there any red flags you can address now?

- Avoid Big, Unusual Transactions (If Possible): If you can, try to spread out large purchases or avoid making them right before or during the mortgage application process.

- Keep Records: If you have significant gifts or unusual income sources, be prepared to explain them and provide documentation.

- Build Your Savings: Even small, consistent contributions to your savings account can make a big difference.

Ultimately, mortgage lenders want to see that you’re a reliable person who can manage their money responsibly. Your bank statements are simply a snapshot of that journey. By understanding what they're looking for and taking a few proactive steps, you can navigate the mortgage process with confidence and get one step closer to making your homeownership dreams a reality. Happy saving, and happy dreaming!