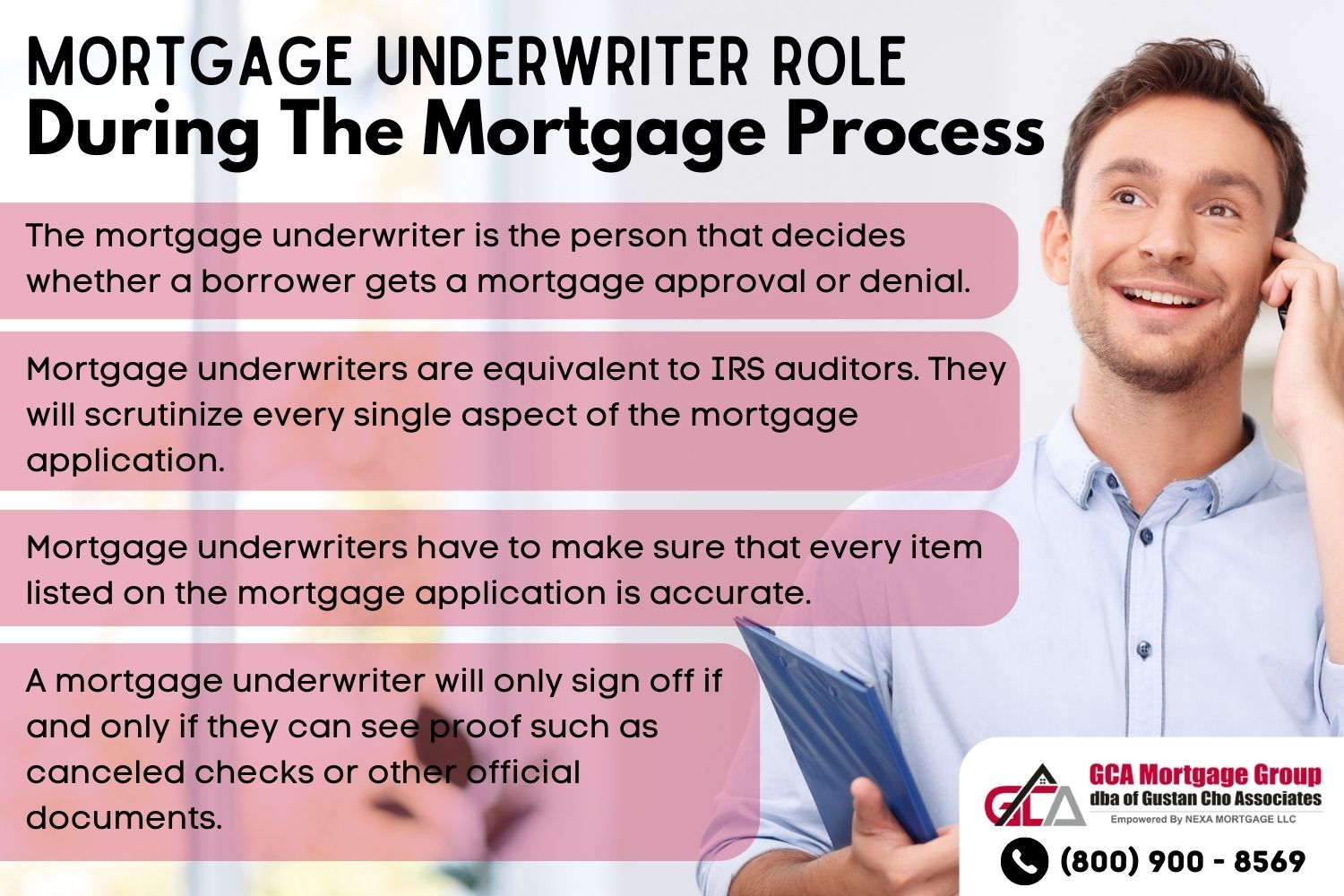

What Does An Underwriter Do In Mortgage Loans

Okay, so you're thinking about buying a house. Exciting stuff! You've probably heard the word "underwriter" tossed around. It sounds a bit mysterious, right? Like some sort of mortgage detective or maybe a super-spy for your loan. But honestly, it's way more interesting (and a little less James Bond) than you might think. Let's spill the tea on what these folks actually do.

Imagine this: You've found your dream pad. The offer's accepted. Woohoo! Now comes the loan application. You're handing over all your financial info. It’s like showing your diary to a stranger. But don't sweat it, because that’s where our hero, the underwriter, steps in. Their main gig? To decide if giving you a boatload of money for a house is a good idea for the bank.

The Gatekeepers of Your Dream Home

Think of them as the bouncers at the coolest club in town: your dream home. They're not just letting anyone waltz in. They've got a checklist. A very important checklist.

So, what's on that list? It’s all about risk. Banks want their money back, plus a little extra for their trouble. An underwriter’s job is to figure out if you're likely to pay them back. It's not about judging you, it's about being super careful with other people's money. Think of them as your financial guardian angel, but one who carries a spreadsheet instead of a halo.

The Deets, Darling!

Let’s dive into the nitty-gritty. They’re looking at a bunch of things:

Your Credit Score: This is like your financial report card. A good score says, "Hey, I’m responsible! I pay my bills on time!" A not-so-great score might raise a tiny eyebrow. Underwriters love a spotless credit history. It’s like finding a perfectly preserved ancient artifact – pure gold!

Your Income and Employment Stability: Do you have a steady paycheck? Are you likely to keep that job? They’re not trying to pry into your water cooler gossip, but they want to see a consistent flow of cash. Think of it as a financial Rorschach test. What do they see in your employment history? Stability? A wild career rollercoaster? They're looking for the former.

Your Debt-to-Income Ratio (DTI): This is a fancy way of saying, "How much money do you owe compared to how much you make?" If you’ve got a mountain of credit card debt and student loans, it might be a bit dicey. They want to make sure you’re not overextended. It’s like looking at a plate: is there enough room for more food (your mortgage payment) after all the other stuff is on it?

The Property Itself: Yep, they’re even checking out the house! Is it worth what you’re paying? What’s the neighborhood like? Is it in a flood zone or a known earthquake area? They get appraisals done to make sure the house is a solid investment. It’s like they’re saying, "Okay, this house looks good on paper, but will it actually stand up to a strong gust of wind?" Sometimes, they might even spot a weird quirk about the property that makes them go, "Hmm, that’s… interesting."

Your Down Payment: How much skin do you have in the game? A bigger down payment usually means you’re more invested and less of a risk. It’s like saying, "I'm really serious about this, folks!"

The Underwriter's Secret Arsenal

These folks are like financial detectives. They pore over tons of documents. Your pay stubs, bank statements, tax returns – all of it. They’re looking for any red flags. Did you have a sudden, unexplained deposit of cash? Did you recently make some huge, extravagant purchases? They’re not trying to be buzzkills, but they need to understand the whole picture.

Sometimes, they might ask for more information. Don't be surprised if they want clarification on something. It’s not personal; it’s their job to be absolutely sure. Think of it as them double-checking your homework. They want to make sure they haven't missed any doodles in the margins that could be important!

A Day in the Life (Probably)

So, what does a typical day look like for an underwriter? Probably a lot of screen time. They’re reviewing applications, crunching numbers, and cross-referencing information. It’s a meticulous process. Imagine sorting through a giant puzzle, but every piece is a financial document, and the picture is your ability to buy a house.

They might have to deal with some tricky situations. Maybe someone has a slightly wonky credit history but a super solid job and a huge down payment. The underwriter has to weigh all these factors. It’s like being a chef who has to balance all the flavors in a dish. Too much salt? Not enough spice? They’re trying to get it just right.

And here’s a fun little tidbit: sometimes, underwriting can feel like a bit of a guessing game. While there are strict rules, there’s also a degree of judgment involved. They’re human, after all! They might see something unusual and have to decide if it’s a genuine risk or just a quirky life event. Maybe you had a one-time, massive vet bill because your goldfish swallowed a pearl. An underwriter might need to understand that story!

The "Why Is This Fun?" Part

Okay, so it’s not exactly a rave, but there’s a certain thrill to it, right? Underwriters are the unsung heroes who make homeownership possible for so many. They’re the final hurdle, the last stamp of approval.

Think of it like this: they're the gatekeepers of your financial future. They hold the keys to unlocking your dream home. And while their job is serious, the outcome is pure joy for you. Imagine them putting that final "approved" stamp on your loan. It’s a moment of victory!

Plus, it’s fascinating to think about all the different scenarios they encounter. Every loan application is a unique story. Some are straightforward, like a perfectly baked cookie. Others are more complex, like a multi-layered cake with unexpected fillings. They have to be adaptable and smart.

And let's be honest, who doesn't love a good puzzle? Underwriters are essentially solving complex financial puzzles every single day. They’re piecing together bits of information to form a clear picture. It’s a mental workout that has a huge real-world impact. They’re the reason many people get to paint their own front doors and have a backyard for barbecues.

So, the next time you hear the word "underwriter," don't picture someone in a stuffy suit frowning at spreadsheets. Picture a sharp, detail-oriented professional who’s playing a crucial role in one of the biggest decisions of your life. They’re the quiet backbone of the mortgage process, ensuring that dreams are built on solid financial ground. And really, isn't that kind of cool?