What Does Charged Off Mean On Your Credit Report: Complete Guide & Key Details

Okay, so picture this: you're happily scrolling through your bank statement, maybe eyeing up that weekend getaway you've been dreaming about, and then BAM! You spot it. A little red flag on your credit report that makes your stomach do a weird little flip. You know, that one that says "Charged Off." My friend Sarah, bless her heart, had a similar moment. She was applying for a mortgage, feeling all confident, and her loan officer just casually dropped, "Oh, and there's a charged-off account here." Sarah went from zero to panic in about ten seconds flat. Her first thought? "Did I accidentally join a cult and forget to pay dues?" (Spoiler alert: no.)

It’s not exactly a phrase that rolls off the tongue with a happy little tune, is it? "Charged Off." Sounds a bit…final. Like something got zapped with lightning. And honestly, for your credit score, it pretty much does. But before you start stockpiling ramen noodles and building a bunker, let's break down what this whole "charged off" thing actually means, because it's not the end of the world, just a really inconvenient detour.

So, What Exactly is "Charged Off"? Let's Decode This Credit Monster

Alright, deep breaths. A charged-off account on your credit report means that the original creditor (think your credit card company, a personal loan provider, or even a medical biller) has decided that they've officially given up on collecting the debt from you. Yeah, you read that right. They've basically written it off as a loss on their books.

This doesn't mean the debt is gone. Oh no, it's still very much a thing. It just means the original company has stopped actively trying to get their money back directly from you. Instead, they’ve probably sold it to a debt collector or a debt collection agency. Think of it like this: your original lender said, "You know what? This is taking too much time and effort. Let's just sell this headache to someone else for pennies on the dollar."

When Does This "Charging Off" Business Happen?

So, how do you get to this point where a company just throws in the towel? Well, it usually happens after you've been seriously delinquent on your payments for a while. We're talking about being 120 to 180 days (or more!) late on your payments.

Each lender has their own internal policies, but the general idea is that they'll try to contact you, send you reminders, maybe even offer hardship programs. But if you're consistently missing payments and they can't get a hold of you or reach an agreement, they'll eventually declare it a charge-off. It's their way of saying, "Okay, we're done here. This isn't making us any money right now."

It's not like they just wake up one morning and decide, "Let's charge off Brenda's account today for fun!" This is a business decision born out of frustration and the realization that they’re unlikely to recover the full amount. And it usually happens after multiple attempts to recover the funds.

The Big Question: How Does a Charge-Off Affect Your Credit Score?

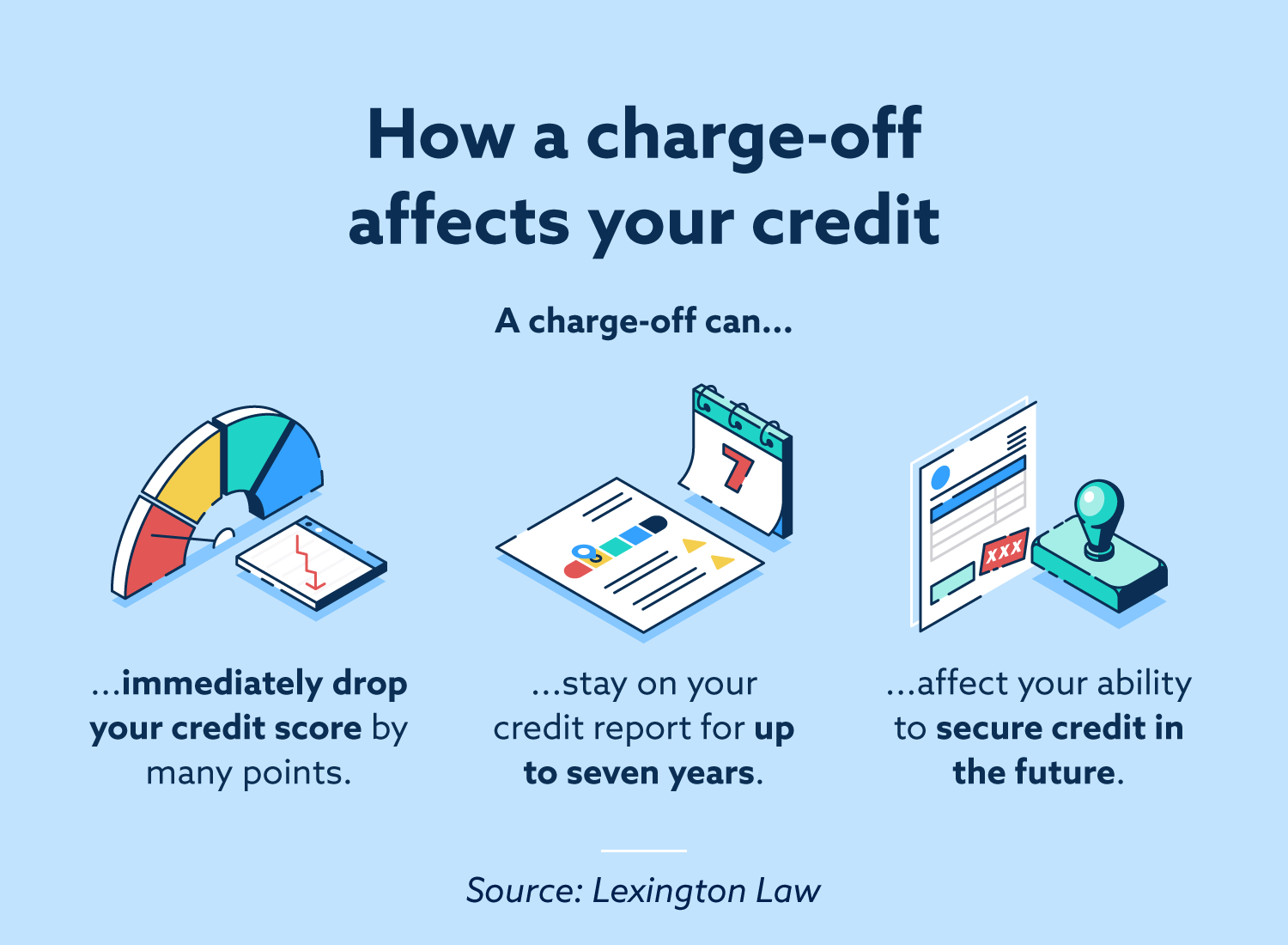

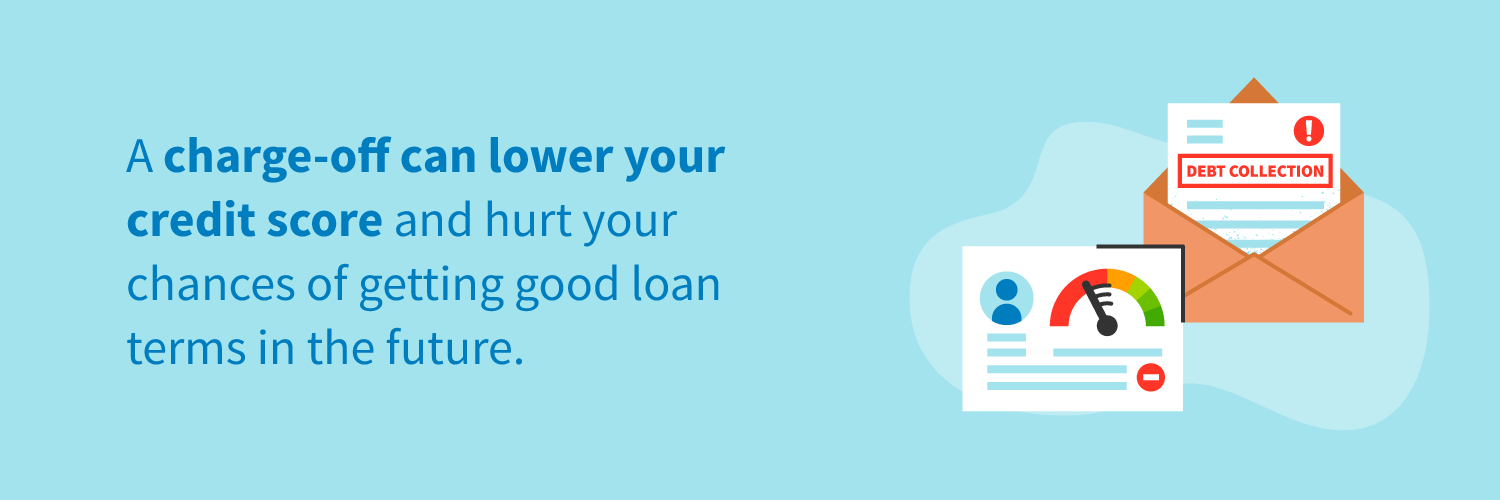

Here’s where things get a little more…ouch. A charged-off account is a major negative mark on your credit report. Like, a really, really big one. It tells future lenders that you’ve had significant trouble managing your debt in the past.

Your credit score is essentially a snapshot of your financial reliability. When a lender sees a charge-off, they interpret it as a sign of high risk. This can lead to:

- Significantly lower credit scores: We're talking a potentially massive drop, often 100 points or more. This can take years to recover from.

- Difficulty getting approved for new credit: Forget that new credit card or car loan for a while. Lenders are going to be hesitant to extend you credit when they see this red flag.

- Higher interest rates: If you do manage to get approved for credit, expect to pay a lot more in interest because you'll be seen as a riskier borrower.

- Challenges with renting apartments or getting utilities: Landlords and utility companies often check credit reports, and a charge-off can make them think twice about trusting you with their property or services.

It’s like showing up to a job interview with a resume that says, "I sometimes pay my bills." Not exactly the best first impression, right?

The "Charged Off" Status vs. Actual Debt Repayment

Now, this is where it gets a bit nuanced, and people often get confused. A charge-off is a status on your credit report. It's the creditor's internal accounting decision. But it doesn't erase the fact that you still owe the money.

That debt doesn't just magically disappear. It’s likely been sold to a third-party debt collector. And guess what? They are going to want their money. They have the legal right to try and collect that debt from you, even if it’s years old (though there are statutes of limitations on lawsuits, which we’ll get to).

The Post-Charge-Off Life: What Happens Next?

So, your account is officially charged off. What’s the daily life of a charged-off debt like? Well, it's usually pretty active, at least for a while.

Debt Collectors Get Involved

As I mentioned, your original creditor likely sold your debt to a debt collection agency. These guys are their own breed. Their business is recovering debts, and they buy these debts for a fraction of the original amount, so even collecting a portion can be profitable for them.

You can expect phone calls, letters, and emails from them. They'll be persistent. They're legally allowed to contact you to try and collect the debt. It's important to know your rights when dealing with debt collectors, though. They can't harass you, threaten you, or lie to you. If they do, document everything!

Statute of Limitations: The Time Limit on Legal Action

This is a crucial detail. Every state has a statute of limitations for how long a creditor or debt collector can sue you to collect a debt. This varies by state and by the type of debt, but it's typically between 3 and 6 years. This is NOT the same as how long the charge-off stays on your credit report.

Once the statute of limitations expires, a debt collector can no longer take you to court to force you to pay. However, they can still try to collect from you voluntarily. And if you make a payment or acknowledge the debt in writing after the statute of limitations has passed, it can sometimes restart the clock!

This is why it's super important to know your state's laws regarding debt collection and statutes of limitations. Don't just ignore everything without understanding the implications. You don't want to accidentally revive an old debt by making a small payment!

How Long Does a Charge-Off Stay on Your Credit Report?

This is another common question that gets a lot of people worried. A charge-off will typically stay on your credit report for seven years from the date of the original delinquency that led to the charge-off.

So, even if you pay off a charged-off debt today, it doesn't immediately vanish from your credit report. It remains a negative mark for the full seven-year period. However, once you pay it off, it should be updated on your credit report to show as "paid charge-off" or "settled charge-off," which is significantly better than an unpaid one.

Can You Remove a Charged-Off Account From Your Credit Report?

This is the million-dollar question, and the answer is…it's complicated.

Paying Off the Debt

The most straightforward way to deal with a charged-off account is to pay it off. While it won't make it disappear from your report for seven years, it will change the status to "paid." This is infinitely better than an "unpaid" charge-off. Lenders will see that you eventually took responsibility, even if it was late.

You might even be able to negotiate a settlement with the debt collector. They bought the debt for pennies on the dollar, so they might be willing to accept a lump sum payment that's less than the full amount owed. This is called a "settlement." If you settle, it will be reported as "settled for less than full amount," which is still negative, but again, better than unpaid.

Disputing Inaccuracies

Here's where you might have a fighting chance of getting a charge-off removed before the seven years are up: if there's an error on your credit report.

Did the creditor report it incorrectly? Was it reported too late? Is it not actually your debt? If you find any inaccuracies, you have the right to dispute them with the credit bureaus (Equifax, Experian, and TransUnion). The credit bureaus are legally required to investigate your claims.

If the creditor or debt collector cannot provide proof that the information is accurate and valid, the charge-off should be removed. This is a crucial part of maintaining the accuracy of your credit report, and it's your right to ensure it's correct. It's not guaranteed, but it's definitely worth exploring if you find any discrepancies.

"Pay for Delete" Agreements (Use with Caution!)

You might hear about something called a "pay for delete" agreement. This is where you offer to pay a debt collector a certain amount (often a settlement) in exchange for them agreeing to remove the entire tradeline (the charged-off account) from your credit report entirely.

This is a bit of a grey area. Legitimate debt collectors are not supposed to agree to this, as their obligation is to report accurate information. However, some smaller or less scrupulous collectors might agree to it. It’s often done verbally or through informal agreements, which can be risky.

My advice? Be extremely cautious with pay-for-delete. Get everything in writing before you send them a single dime. If it's not in writing, it's as good as saying it to the wind. And even if you get it in writing, there's a chance they won't uphold their end of the bargain. It's a gamble.

Strategies for Dealing with a Charged-Off Account

Okay, so you've got a charge-off. What's the game plan? Here are a few actionable steps:

- Get Your Credit Reports: First things first, pull your credit reports from all three major bureaus. You can get them for free at AnnualCreditReport.com. Review them carefully for any inaccuracies related to the charged-off account.

- Understand the Details: Note the date of the delinquency, the original creditor, the amount of the debt, and the name of the debt collector (if applicable).

- Research Your State's Statute of Limitations: Know how long the debt collector can legally sue you for. This is vital information.

- Contact the Debt Collector (Strategically): If you decide to try and settle or pay, do it in writing. Request validation of the debt first. This means asking them to prove they own the debt and that the amount is correct.

- Negotiate: Don't be afraid to negotiate a settlement. Start with a low offer and work your way up. Remember, they bought the debt for cheap.

- Prioritize Repayment (If Possible): While it won't vanish, paying off a charge-off is still a good move. It shows responsibility and improves your standing with future lenders more than an unpaid charge-off does.

- Dispute Errors: If you find any errors, dispute them immediately with the credit bureaus. Keep copies of all communication.

It’s a tough situation, no doubt about it. But knowledge is power. Understanding what a charge-off is, how it impacts you, and what your options are is the first step to regaining control of your financial future.

The Long Road to Recovery

A charged-off account is a serious setback, but it's not a life sentence. It takes time, discipline, and smart financial habits to rebuild your credit after such an event.

Focus on making all your other current bills on time, every time. Build a positive payment history going forward. Consider a secured credit card to help rebuild credit. Avoid taking on new debt if you can. Be patient. Rebuilding credit is a marathon, not a sprint.

So, while Sarah’s initial panic was understandable, the good news is that by understanding what "charged off" means and taking proactive steps, she was able to navigate the situation. It wasn't fun, and it definitely impacted her mortgage approval timeline, but it wasn't the end of the world. It was just a really, really expensive lesson.

Remember, you're not alone in this. Millions of people deal with credit challenges. The key is to learn from them and use that knowledge to make better decisions moving forward. And hey, at least now you know what that scary "charged off" phrase actually means!