What Does It Mean To Be An Incorporated Company

Ever found yourself scrolling through your feed, maybe sipping on your oat milk latte (or maybe just a good old-fashioned cuppa), and stumbled across mentions of "incorporated companies" or "LLCs"? It’s one of those terms that sounds super official, maybe even a little intimidating, right? Like something reserved for power suits and corner offices. But what does it actually mean, beyond the legalese and the fancy letterhead? Let’s break it down, no jargon overload, just good vibes and a clear understanding of what it means when a business decides to go, well, incorporated.

Think of it this way: imagine you're starting a small business, maybe selling your amazing handmade candles online or offering your killer graphic design skills to the world. You’re the whole shebang – the creator, the marketer, the accountant (even if that just means stashing receipts in a shoebox). But as your little venture grows, maybe you start thinking about how to protect yourself, how to make it look more… grown-up. That's where the idea of incorporation pops up, like a cool new filter for your business’s personality.

At its heart, becoming an incorporated company is like giving your business its own legal personality. It’s like your business suddenly gets its own passport and can sign its own contracts, own its own assets, and even be sued (yikes, but also, good protection!). It’s a fundamental shift from being a sole proprietorship or a partnership, where you are essentially the business, and the business is you. With incorporation, there’s a separation. A clear dividing line.

The Big Separation: You vs. The Business

This separation is probably the most crucial aspect of being an incorporated company. For example, if you run a sole proprietorship and your business racks up a mountain of debt, or someone sues you for a mishap (imagine a rogue delivery drone incident with your artisanal dog treats!), your personal assets – your house, your car, your vintage vinyl collection – are on the line. It’s all fair game.

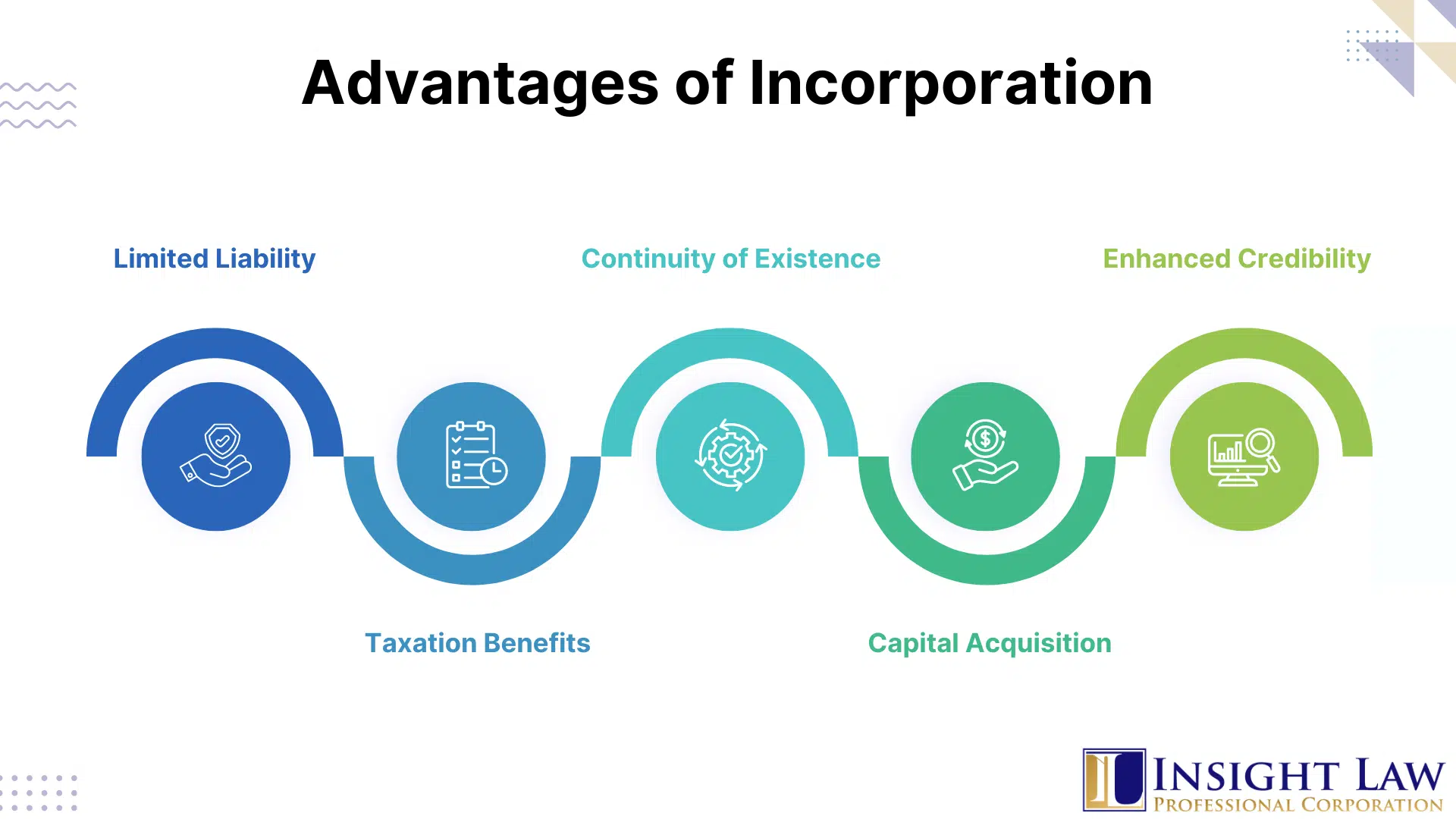

But when your business is incorporated, it’s the company that’s liable. This is known as limited liability. So, if the same debt or lawsuit happens to your incorporated business, it's usually the company's assets that are at risk, not yours personally. It’s like putting up a protective shield around your personal life. Pretty neat, right?

This concept of limited liability is a huge deal, especially for startups or businesses with a higher risk profile. It allows entrepreneurs to take calculated risks without the constant dread of losing everything they own. It’s the kind of protection that might encourage someone to launch that innovative tech startup or that eco-friendly fashion line they’ve been dreaming about.

Different Flavors of Incorporation

Now, "incorporated company" is a bit of a catch-all term. There are actually a few different structures that fall under this umbrella, each with its own quirks and benefits. The most common ones you'll hear about are:

- C Corporation (C-corp): This is the classic, big-kid corporation. It's often the choice for larger businesses that plan to go public or raise significant capital. The main thing to know about C-corps is that they face double taxation. The company pays taxes on its profits, and then shareholders pay taxes again on the dividends they receive. Think of it as paying tax twice on the same pot of money.

- S Corporation (S-corp): An S-corp is a special tax election that allows profits and losses to be passed through directly to the owners' personal income without being subject to corporate tax rates. This avoids the double taxation of C-corps. It's often a sweet spot for smaller to medium-sized businesses that want the protection of incorporation but want to avoid that extra tax layer.

- Limited Liability Company (LLC): This is a super popular option for many small businesses. It blends the limited liability of a corporation with the pass-through taxation of a sole proprietorship or partnership. It's often seen as simpler to set up and run than a traditional corporation, making it a favorite for freelancers, consultants, and smaller ventures. Think of it as the "best of both worlds" option for many.

The choice between these often depends on the business’s size, its growth aspirations, tax implications, and the founders' comfort level with administrative complexity. It’s like choosing the right outfit for the occasion – you want something that fits well and makes you feel confident.

Why Would a Business Even Bother?

So, beyond the legal protection, what’s the big draw? Why do so many businesses choose to go through the process of incorporating?

One of the main reasons is credibility and professionalism. When you tell someone you're an incorporated company, it often lends a certain gravitas. It suggests you're serious, established, and have gone through the proper channels. This can be crucial when you’re trying to secure funding, land big clients, or even attract talented employees. It’s like upgrading from a handwritten sign to a sleek, professionally designed logo – it just looks and feels more legit.

Think about it: if you’re a small business owner looking to partner with another company, or a bank considering a business loan, seeing that a business is incorporated can signal a level of structure and accountability that’s reassuring. It’s less about a hunch and more about a formal framework.

Another big plus is easier fundraising. Investors, especially venture capitalists and angel investors, often prefer or even require companies to be incorporated (usually as a C-corp) before they’ll put their money in. This is because it makes ownership stakes clear and manageable. They want to know exactly what they’re buying into, and incorporation provides that clarity. It’s like how a director needs a clear script to produce a movie; investors need a clear ownership structure to invest.

There are also tax advantages to consider. While we touched on double taxation for C-corps, other structures can offer deductions and benefits that aren't available to sole proprietors. For instance, incorporated businesses can often deduct certain business expenses, like health insurance premiums for employees (including the owner-employee!), which can lead to significant tax savings. It’s like finding hidden discounts on your favorite online store, but for your business finances.

The Nitty-Gritty: What's Involved?

Alright, so it sounds good, but what’s the actual process? It’s not exactly a walk in the park, but it's definitely manageable. It generally involves:

- Choosing a name: This needs to be unique and not already in use by another registered business in your state or country. Think of it like picking a username that’s available on your favorite social media platform – no duplicates allowed!

- Filing articles of incorporation: This is the official document you file with the relevant government agency (usually the Secretary of State in the US). It includes information like the company’s name, purpose, the number of shares it can issue, and the name and address of its registered agent (the official point of contact for legal documents).

- Appointing a board of directors: For corporations, you need a board to oversee the company’s major decisions.

- Creating bylaws: These are the internal rules that govern how the company operates, like how meetings will be conducted and how directors are elected.

- Issuing stock: This is how ownership is divided among shareholders.

The exact steps and requirements can vary by location. Some states are known for being more business-friendly with simpler processes. It often involves fees, so it’s wise to budget for that. Many entrepreneurs choose to work with a lawyer or a specialized service to help navigate this process smoothly, ensuring all the i’s are dotted and t’s are crossed.

When Does it Make Sense to Incorporate?

So, when is the right time to consider making the leap? It’s not a one-size-fits-all answer, but here are some indicators:

- When your business is growing and generating consistent revenue. If you’re just starting out with a side hustle that brings in a few bucks here and there, the administrative overhead might not be worth it yet. But once you’re seeing regular income and potential for expansion, incorporation starts to look attractive.

- When you’re taking on significant personal risk. If your business involves potential liabilities (think product liability, professional services with high stakes, or even just high-value assets), limited liability protection becomes a major benefit.

- When you plan to seek external funding. As mentioned, investors often favor incorporated entities. If you have ambitious growth plans that require outside capital, getting incorporated early can streamline that process.

- When you want to build a more formal, enduring business structure. Incorporation is like laying down stronger foundations for a building. It creates a more stable and sustainable entity that can outlast its founders.

It’s a bit like deciding when to upgrade your phone. If your current one still makes calls and sends texts, you might hold off. But if you’re missing out on essential apps, struggling with battery life, or want better features for your photography hobby, it’s time for an upgrade. For businesses, incorporation is often that significant upgrade.

The Cultural Cachet of "Incorporated"

There's a certain cultural cachet that comes with being an "incorporated company." It’s a term that’s deeply embedded in our understanding of business and success. Think of iconic brands you know – Apple Inc., Google (Alphabet Inc.), Microsoft Corporation. These names immediately evoke a sense of scale, innovation, and global reach, all of which are often associated with being incorporated.

In pop culture, the image of the "corporate titan" or the "startup founder" often implies an incorporated entity. While many successful businesses start out smaller, the journey to becoming a recognized, impactful company frequently involves taking on that corporate structure. It’s a narrative we see in movies, TV shows, and business biographies – the transition from a garage startup to a publicly traded giant.

It’s also about the perception of stability. When you’re an incorporated company, you’re not just a solo act; you’re a team, a structure, a recognized player in the economic landscape. This perception can influence everything from customer trust to employee morale. People want to work for and buy from businesses they perceive as stable and well-managed.

A fun little fact: the term "incorporate" itself comes from the Latin word "incorporare," meaning "to form into one body." It’s quite fitting, as incorporation essentially creates a single, unified legal entity out of various individuals and assets.

A Final Thought on the Everyday

So, what does it mean to be an incorporated company? It means your business has stepped up, gained its own legal footing, and established a clear boundary between its operations and your personal life. It’s about taking your venture to the next level, unlocking new possibilities, and building something with greater resilience and potential.

And you know what? This concept of "incorporation," of creating a distinct entity for a specific purpose, isn't just for big businesses. We do it in our own lives all the time, in smaller, less formal ways. Think about how you might manage your personal finances separately from shared household bills, or how you set boundaries between your work life and your downtime. Even deciding to join a book club or a sports team is, in a way, creating a small, temporary "incorporated" group with shared goals and rules.

Ultimately, being an incorporated company is about structure, protection, and growth. It’s the business world’s way of saying, "We’re serious, we're organized, and we're here to stay." And that’s a pretty powerful statement, whether you're a global tech giant or a one-person operation dreaming of the big leagues.