What Is Difference Between Standing Order And Direct Debit

Ever found yourself staring at your bank statement, a little bewildered by the magical disappearances of cash? You’re not alone. It’s like a tiny gnome sneaks in at night and just… poof… takes some money for rent. And sometimes, the mystery deepens with two very similar sounding culprits: Standing Orders and Direct Debits. They both sound like helpful little helpers, right? Like tiny, efficient robots making sure your bills are paid on time. But oh, my friends, the difference is like the difference between a polite waiter taking your order and a surprisingly enthusiastic toddler deciding what you’re having for dinner.

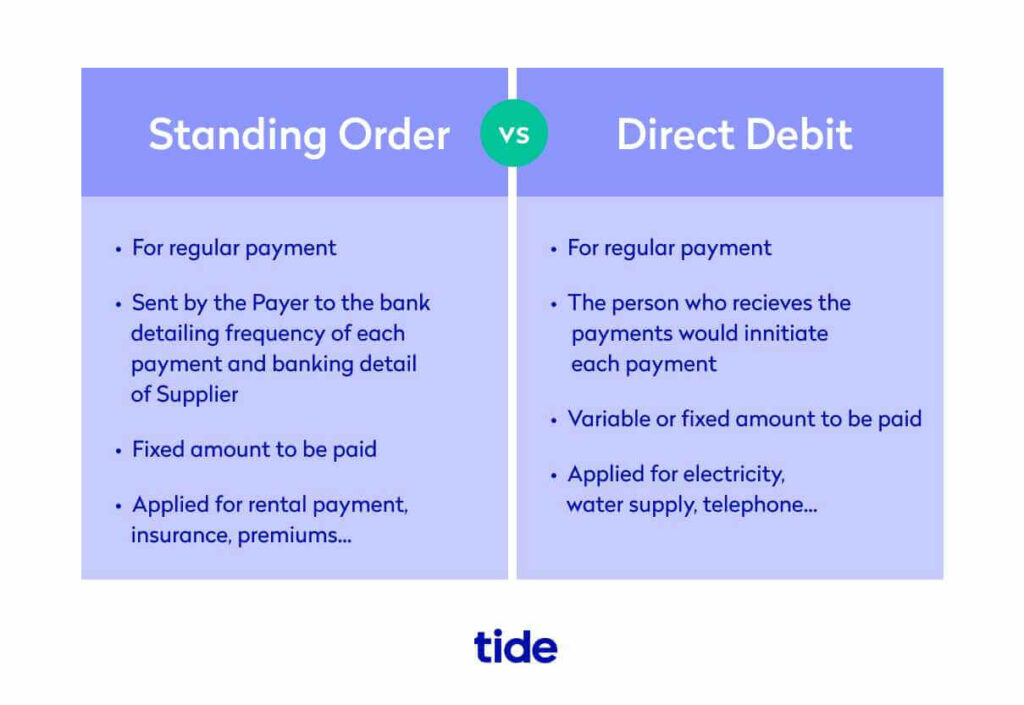

Let’s dive into this thrilling world of automated payments, shall we? Imagine you’re planning a regular treat for yourself. Maybe it’s that fancy coffee subscription that arrives every month. Or perhaps you’re sending a little bit of cash to your favourite charity every Tuesday. For these kinds of regular, predictable payments, you’d use a Standing Order. Think of it as you, the boss, telling your bank, “Hey, buddy, send exactly £20 to ‘Awesome Coffee Co.’ on the 1st of every month. No questions asked.”

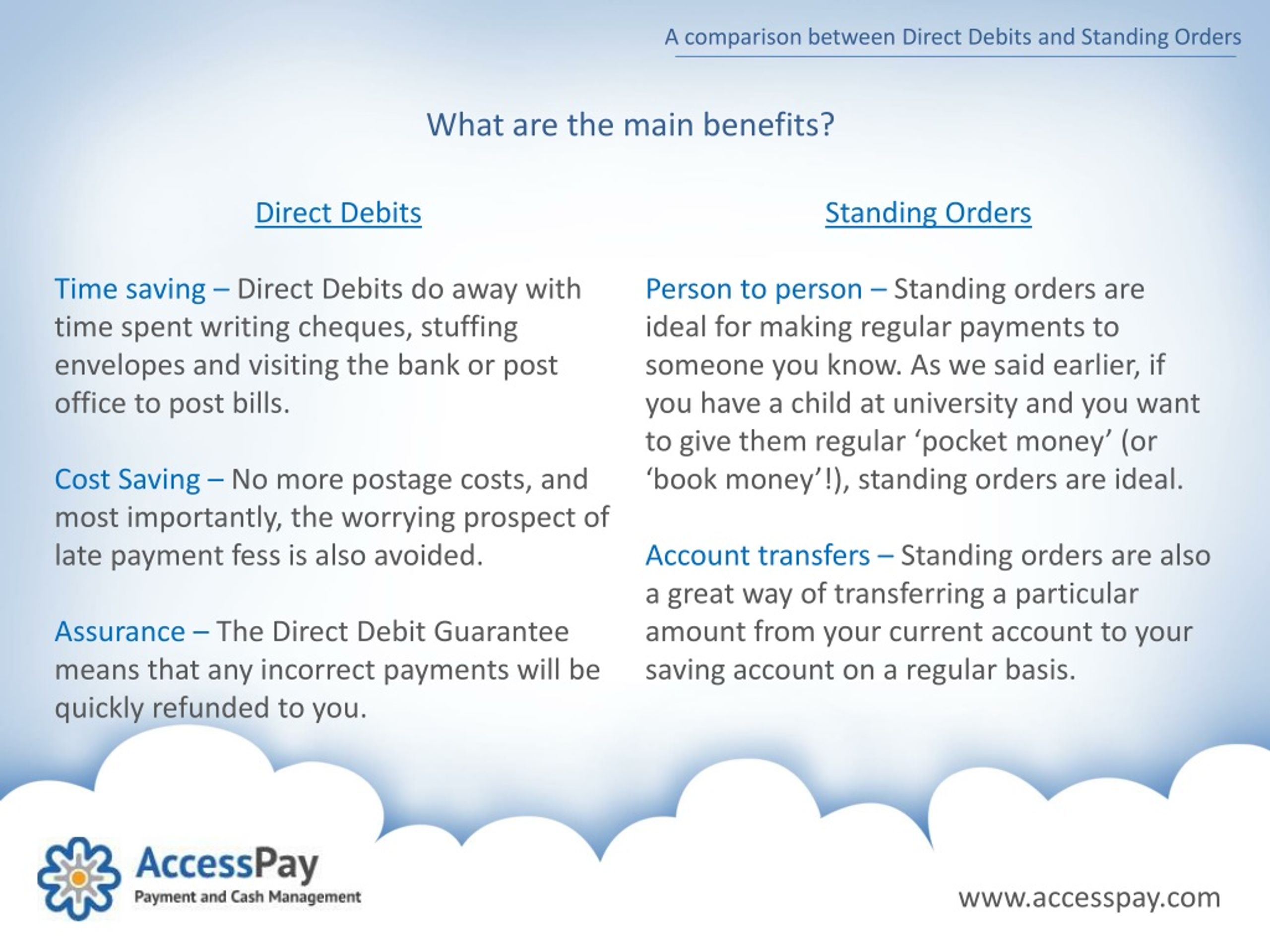

It’s like setting an alarm. You know it's going to go off at the same time, and it’s going to do the same thing. The amount is fixed. The date is fixed. It’s all very organized and, dare I say, a little bit… boring? But in a good way! It’s the reliable friend who always shows up on time with a predictable, albeit small, gift. You’re in complete control. You tell it what to do, and it does it. No surprises. Just pure, unadulterated, automatic payment goodness.

Now, where does the fun (and slight terror) come in? Enter the Direct Debit. This is where things get a bit more… dynamic. A Direct Debit is more like you giving permission to someone else to take money from your account. Who? Well, it’s usually the companies you owe money to. Your electricity provider, your phone company, your gym, that subscription box that sends you exotic socks every month (you know the one). You sign up for their service, and they ask, “Hey, can we just… you know… take the money we owe you directly from your account?” And you, in your infinite wisdom (or perhaps just a moment of bill-paying fatigue), say, “Sure, why not!”

The key difference here is that with a Direct Debit, the amount can change. This is where our toddler analogy comes in. Your electricity bill is rarely the same every month, is it? One month it’s mild, and the next it’s freezing, and suddenly your heating bill looks like the national debt. The company that provides your electricity is authorized to pull whatever amount is due from your account. You give them the green light, and they decide when and how much to take (within the agreed terms, of course!).

It’s like having a trusted (or sometimes untrusted) friend with a key to your wallet. They’re supposed to only take what’s owed, but sometimes they might accidentally grab an extra tenner because they’re feeling peckish. The beauty of the Direct Debit is that it’s super convenient for those variable bills. You don’t have to remember to log in and pay your phone bill every month. It just happens. And there are safeguards! You can cancel a Direct Debit at any time, and if an incorrect amount is taken, you have a right to get it back. So, it's not quite as wild as handing over your wallet to a toddler, but it's certainly more exciting than a Standing Order.

Think of it this way: You set up a Standing Order to send your mum £50 every month for her birthday. It's a lovely gesture, predictable and always the same amount. That’s a Standing Order. Now, imagine you’ve agreed to pay your Netflix subscription. The price might go up next year, or maybe they'll have a special offer. They’ll just take the correct amount each month. That’s a Direct Debit.

So, to sum up this epic financial saga: * Standing Order: You are the boss. Fixed amount, fixed date. Like a robot servant you control. Very sensible. * Direct Debit: You give permission. Amount can vary. Like a friendly (or sometimes overzealous) business partner. More flexible, a bit more… ooh, what’s this charge?

My unpopular opinion? Direct Debits are like the exhilarating rollercoaster of bill payments. They keep you on your toes, and sometimes make you gasp (usually at the amount!). Standing Orders are like a perfectly brewed cup of tea. Reliable, comforting, and utterly predictable. Both have their place, of course. But if you ask me, a little bit of automated excitement now and then makes managing your money just a tiny bit more interesting. Just keep an eye on those statements, folks. That gnome might be using your card for his midnight snack runs.