What Is The Average Cost Of Motorcycle Insurance? Explained Simply

Alright, gather 'round, fellow two-wheel enthusiasts and the perpetually curious! Let's talk about something that can feel as mysterious as why your bike inexplicably dies right before your favorite biker bar: motorcycle insurance costs. Now, before you envision a dragon guarding a pile of gold that you have to bribe with your hard-earned cash, let's break this down. Think of me as your slightly-too-caffeinated friend at the local coffee shop, armed with a latte and some surprisingly useful (and hopefully not too boring) facts.

So, you're wondering, "What's the damage? What's this magical 'average cost' I keep hearing about?" Well, buckle up, buttercup, because it's not a simple, one-size-fits-all answer. It's more like asking, "What's the average cost of a smile?" It depends on who's smiling, why they're smiling, and if they just found a twenty-dollar bill in their old jacket. But to give you a ballpark figure, and I mean a very wide, sprawling, maybe even slightly-off-target ballpark, we're often looking at something in the realm of $700 to $1,500 per year. Yeah, I know, some of you are already doing mental gymnastics to fit that into your budget, while others are thinking, "That's it? I was expecting it to cost more than my firstborn child's college tuition!"

But here's the juicy gossip, the real tea: that "average" is about as useful as a screen door on a submarine. It's a starting point, a whisper in the wind. What actually affects your premium is like a superhero team, each with their own powers to either boost or shrink that number. And let me tell you, some of these powers can be downright brutal, while others are more like a gentle breeze.

The Usual Suspects: Who's Playing a Role in Your Premium?

First up, let's talk about the bike itself. Is your ride a sleek, screaming sportbike that looks like it was designed by a caffeinated ninja and can do 0 to 60 faster than you can say "speeding ticket"? Or is it a more relaxed cruiser, a trusty steed that purrs along like a contented kitten after a good meal? The type, make, model, and even the year of your motorcycle are like the secret ingredients in your insurance recipe. A $25,000 superbike is going to cost a lot more to insure than a vintage scooter that tops out at a brisk 30 mph. Think about it: if your bike is a lightning bolt of pure speed, the chances of it meeting an untimely (and expensive) end are, shall we say, elevated. Plus, those fancy parts are probably worth more than my entire wardrobe.

Then there's your riding history. This is where your past actions come back to haunt you, or bless you. If you've been a responsible rider for years, with a clean record as a freshly wiped windshield, you're likely to get a pat on the back (and a lower premium). But if your history looks like a rally car course with a few too many donuts and unexpected detours, well, the insurance companies might start sweating a little. They've seen it all, folks. They know if you're a "once in a blue moon" rider or someone who treats their bike like a permanent extension of their soul. And let's be honest, if you've got more tickets than a lottery winner, they're going to factor that in. They're not in the business of funding your joyrides to the "danger zone."

Your age and experience are also huge players. Think of it this way: a brand-new driver, no matter how many hours they spent playing Gran Turismo, is going to be seen as a higher risk than a seasoned rider who remembers when helmets were optional (and probably a terrible idea). Younger riders, bless their enthusiastic hearts, tend to have higher premiums. It's not personal; it's just statistical. They haven't had enough time to accumulate that wisdom that comes from surviving a few close calls and learning from them. So, if you're young and a bit of a thrill-seeker, expect to pay a bit more. It's like the universe's way of saying, "Be careful, sprout!"

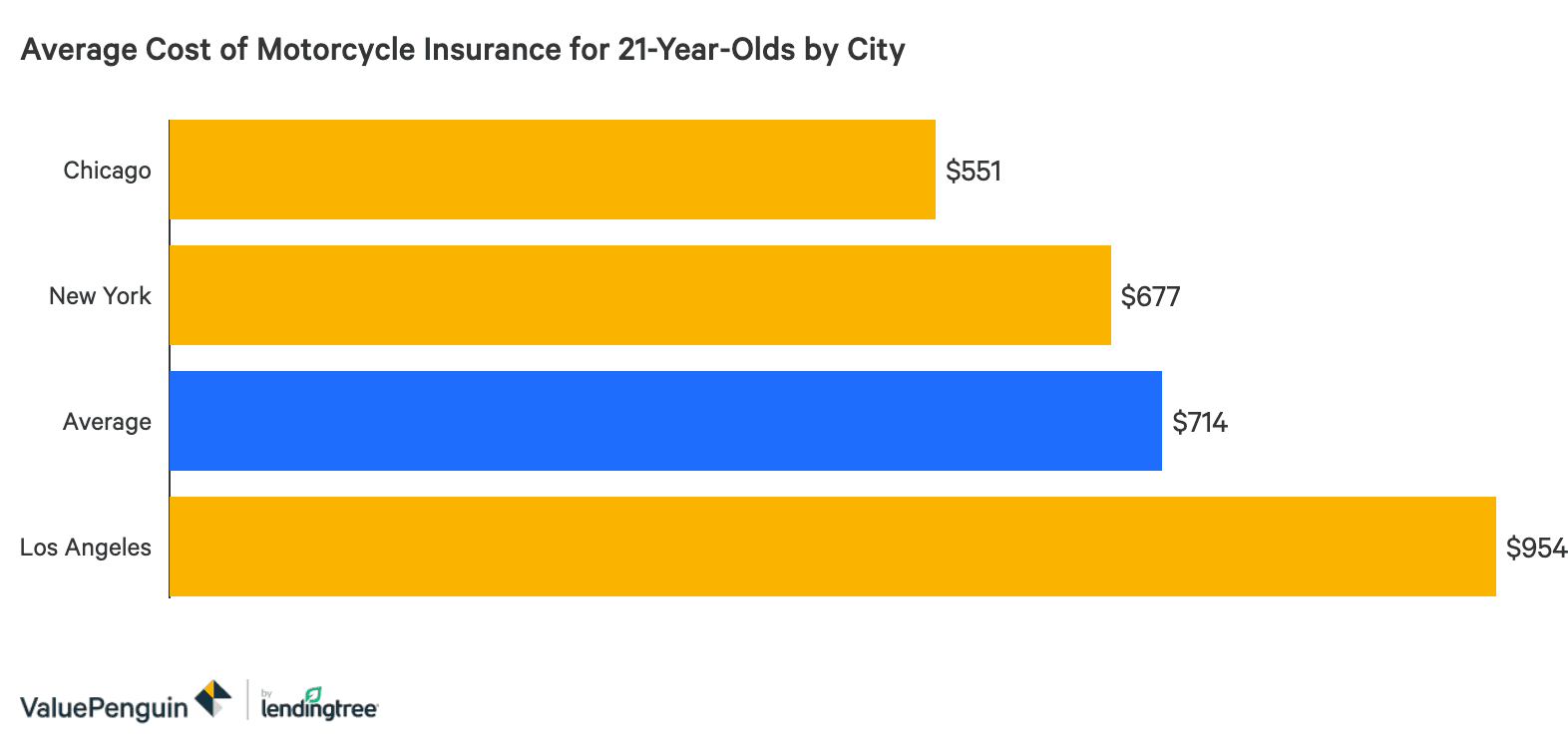

Where you live can also be a biggie. This one’s a bit of a head-scratcher sometimes, but it makes sense. If you live in a bustling metropolis with traffic that makes rush hour in Tokyo look like a Sunday stroll in the park, your insurance might be higher. More cars, more chaos, more opportunities for fender-benders (or, in this case, saddlebag-scrapes). Conversely, if you're out in the serene countryside, where the biggest obstacle is a rogue squirrel, your rates might be a bit more chill. Plus, let's not forget about theft rates. Some areas are unfortunately more prone to bike theft than others, and insurance companies don't like it when their precious bikes go walkabout.

The Nitty-Gritty: What Exactly Are You Insuring Against?

Now, let's get down to the nitty-gritty of what you're actually paying for. Motorcycle insurance isn't just one big, amorphous blob of coverage. It's a smorgasbord of options, and you get to pick what you want. This is where the cost can really swing, like a pendulum in a haunted house.

The Big Kahunas of Coverage:

- Liability Coverage: This is your "oops, my bad" insurance. If you cause an accident, this covers the damage to other people and their property. It's basically your get-out-of-jail-free card for when you accidentally channel your inner daredevil and make someone else's car look like a crumpled piece of tin foil. This is usually the cheapest part, but it's absolutely essential. Think of it as your peace of mind money.

- Collision Coverage: This is for when your bike meets something it shouldn't, like a parked car, a rogue pothole the size of a small crater, or your own spectacular lack of coordination. It covers the damage to your bike, even if you were at fault. This is where things start to get a bit pricier, especially for newer or more expensive bikes.

- Comprehensive Coverage: This is your "everything else" insurance. Think of it as the insurance that protects you from the truly bizarre. Stolen bike? Covered. Vandalism? Covered. A meteor strike (okay, maybe not a meteor strike, but you get the idea)? Covered. Falling tree branches? Yep. It's for all the things that aren't a direct collision. This also adds to your premium, but it's a good idea for protecting your investment.

- Uninsured/Underinsured Motorist Coverage: This is your superhero cape for when you encounter riders or drivers who are either completely uninsured or don't have enough insurance to cover the mess they've made. It protects you and your passengers if you're hit by one of these unfortunate souls. It’s like a shield against the irresponsibility of others.

- Medical Payments Coverage: This helps pay for medical expenses for you and your passengers, regardless of who's at fault. It’s a good one to have, especially if you’re prone to gravity-induced acrobatics.

The more of these coverages you choose, and the higher the coverage limits, the more you'll be shelling out. It's a trade-off between risk and reward, or in this case, risk and peace of mind. Do you want the absolute bare minimum, or do you want to sleep soundly knowing that if the worst happens, you're not going to have to sell your kidney to pay for it?

The Secret Sauce: How to Potentially Save Some Dough

Now, for the good news! You're not entirely at the mercy of the insurance gods. There are ways to potentially shave some of those numbers down. Think of yourself as a savvy shopper, always looking for a deal.

- Bundle Up: If you've got your car, your home, or even your pet llama insured with the same company, you might get a discount. It’s like getting a loyalty card for your insurance providers.

- Rider Education Courses: Completing a motorcycle safety course can be a real money-saver. Insurance companies love seeing that you're committed to being a safe rider. It's like getting extra credit for being smart!

- Good Student Discounts (If Applicable): If you're a younger rider and still in school, believe it or not, good grades can sometimes earn you a discount. So, hit the books, aspiring stunt rider!

- Low Mileage Discounts: If you only ride your bike on sunny weekends and for the occasional pilgrimage to your favorite burger joint, you might qualify for a discount. They’re not insuring you for your daily commute through a blizzard.

- Anti-Theft Devices: If your bike is equipped with an alarm system or a good old-fashioned sturdy lock, let them know! It shows you're taking precautions, and they might reward you for it.

- Shop Around: This is the golden rule, folks. Don't just go with the first quote you get. Get quotes from multiple insurance companies. Prices can vary wildly, and you might be leaving money on the table. It's like comparing prices at different dealerships before buying a bike.

So, there you have it. The average cost of motorcycle insurance is a bit of a moving target, influenced by a whole host of factors, from the roar of your engine to your impeccable (or not-so-impeccable) driving record. It's not a fixed price, but rather a personalized quote that reflects your individual risk profile. But by understanding what goes into it and being a proactive consumer, you can hopefully navigate the world of motorcycle insurance without feeling like you're being taken for a ride. Now go forth, ride safe, and may your premiums be ever in your favor!