What Is The Difference Between Interest Rate And Apr? Explained Simply

Alright, settle in, grab your latte, or maybe something a bit stronger if we're talking about this stuff. So, you’ve probably heard the terms "interest rate" and "APR" thrown around like confetti at a wedding you barely wanted to attend. They sound similar, right? Like they’re distant cousins who wear the same ridiculously patterned sweater. But trust me, when your wallet is on the line, understanding the difference is about as crucial as knowing your own social security number (or at least remembering where you parked your car). We’re diving deep, but don't worry, no actual diving goggles required. We’re keeping it light, breezy, and hopefully, hilariously informative.

Imagine you're borrowing a cup of sugar from your neighbor. That's kind of like the base loan. The interest rate is basically the little "thank you" you offer for that sugar. It's the percentage the lender charges you for the privilege of using their money. Simple enough, right? It’s the sticker price, the headline number you see on that shiny credit card offer or the mortgage advertisement. It’s like saying, "Hey, I’ll give you back the sugar, plus a tiny bit extra for your troubles."

But here’s where things get a little more interesting. Think of the APR, or Annual Percentage Rate. This guy is the overachiever. He’s the one who not only brings the sugar back but also offers to help with your garden, walk your dog, and maybe even do your taxes. The APR is the real cost of borrowing. It’s like the interest rate’s older, more responsible sibling who insists on showing you the entire bill, not just the part you’re looking at.

So, what’s lurking in this APR party that isn't in the plain old interest rate? A whole bunch of extra goodies! We’re talking fees, charges, and other little bits of financial confetti that the lender tacks on. Think of it like buying a fancy new gadget. The advertised price might be appealing, but then you get to checkout and BAM! There's the "processing fee," the "installation charge," and that suspiciously expensive "extended warranty" you didn't ask for but somehow ended up with.

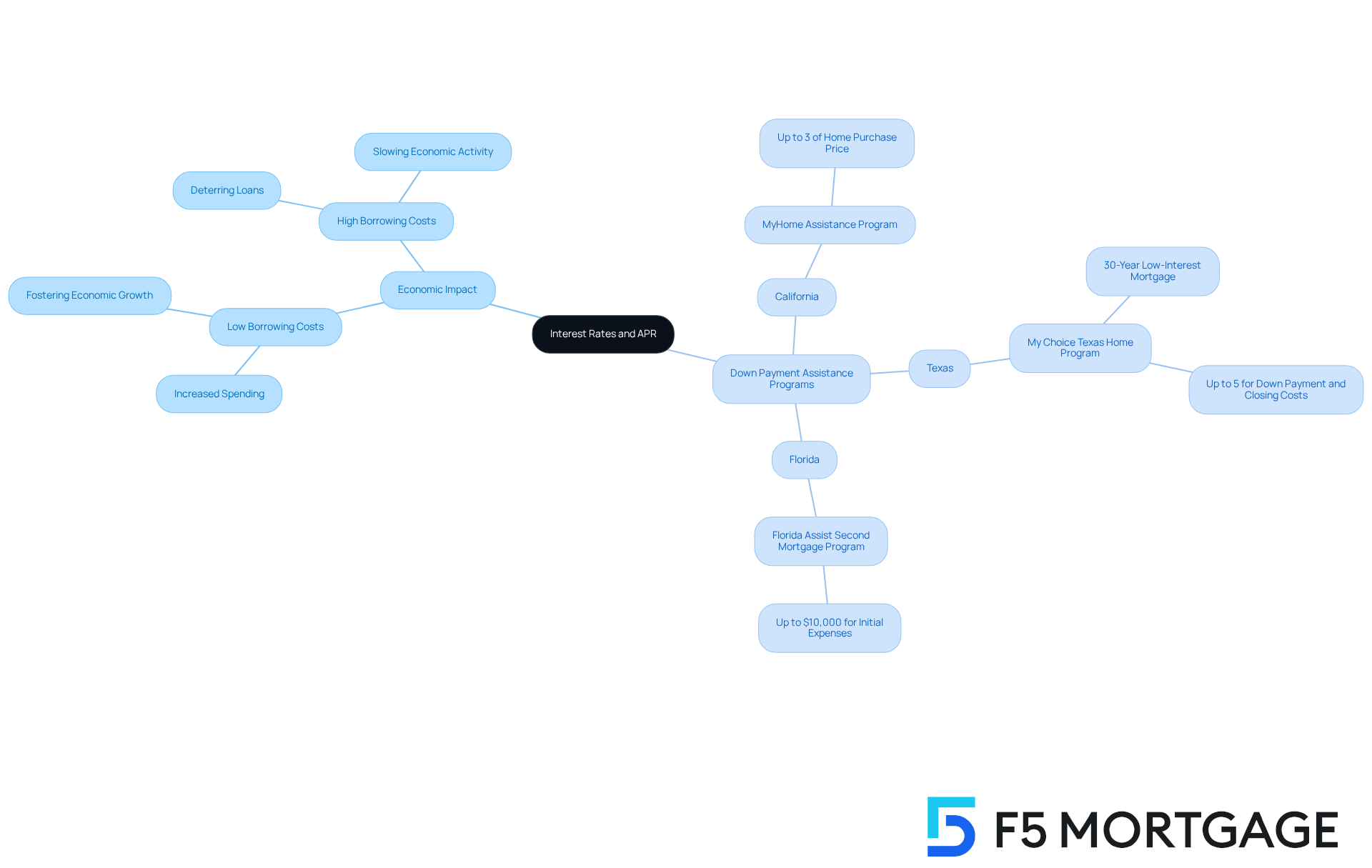

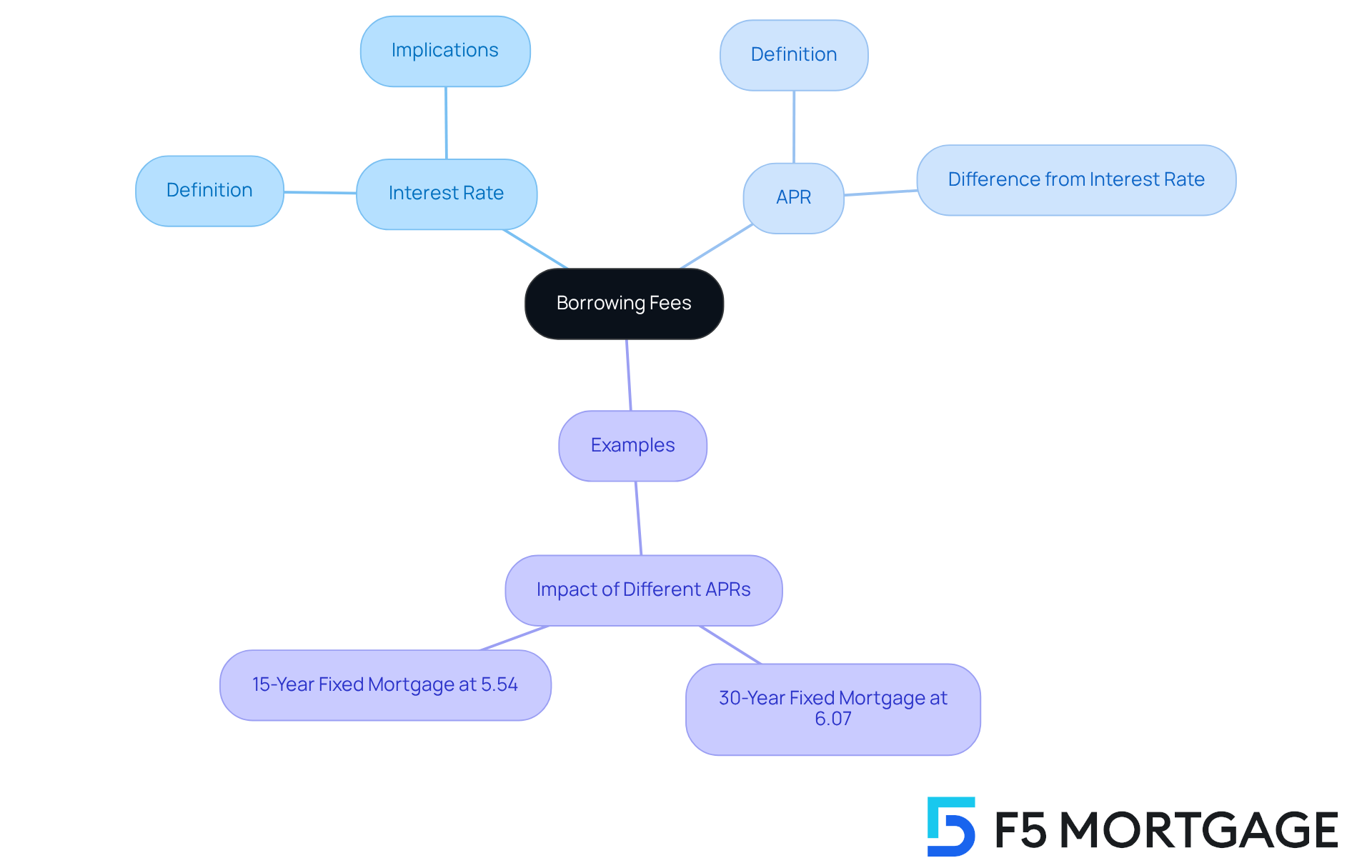

For loans, these "extra goodies" can include things like origination fees (the bank’s way of saying "thanks for letting us lend you money, here’s a fee for that"), appraisal fees (especially for mortgages, where they need to figure out if your house is worth more than a slightly used toaster), and even things like private mortgage insurance (PMI) if your down payment is looking a bit… shy.

Imagine you want to buy a super cool, slightly used spaceship. The interest rate might be advertised as a cool 5% on the loan. Sounds reasonable, right? You’re thinking, "Awesome! I’ll be zipping through the galaxy in no time!" But then the APR kicks in. Suddenly, that 5% is creeping up to 7.2%. Where did that extra 2.2% go? Well, that’s probably the docking fee (they charge you for using their launchpad!), the cosmic fuel inspection fee (gotta make sure your ship isn't leaking stardust!), and perhaps a "galactic exploration surcharge" (because, obviously, exploring the cosmos isn't free!).

It’s like when you order pizza. The menu says $15 for a large pepperoni. Great! But then you add delivery, a tip for the driver who braved rush hour traffic (and maybe a rogue asteroid), and suddenly that $15 pizza is closer to $25. The $15 is your interest rate; the $25 is your APR. See the difference? One is the tempting appetizer; the other is the full, sometimes eye-watering, meal.

Now, why should you care about this distinction? Because the APR gives you the true picture of how much that loan is actually going to cost you over the course of a year. It’s the ultimate reality check. That low interest rate might look like a siren song, luring you in, but the APR is the wise old sailor who warns you about the rocky shores and the sea monsters lurking beneath.

Let’s say you’re comparing two credit cards. Card A offers a 15% interest rate with no annual fee. Card B offers a 14% interest rate but slaps on a $50 annual fee and a $20 processing fee for balance transfers. If you only look at the interest rate, Card B looks like the winner. But when you factor in those fees, Card A might actually be cheaper in the long run, especially if you’re carrying a balance.

This is particularly important for big-ticket items like mortgages and car loans. Those seemingly small percentage differences can add up to thousands, even tens of thousands, of dollars over the life of the loan. It’s the difference between being able to afford that dream vacation and just… affording a slightly nicer toaster. And who wants to just afford a nicer toaster when you could be sipping margaritas on a beach?

A surprising fact? Some lenders might try to be slick. They might advertise a low interest rate to get you in the door, but then load up on fees that inflate the APR. It's like a magician pulling a rabbit out of a hat, except instead of a cute bunny, it’s a hefty fee that makes your wallet do a vanishing act.

So, next time you’re looking at a loan, a credit card, or anything that involves borrowing money, do yourself a favor: don't just look at the interest rate. Look at the APR. It’s the whole story. It’s the director’s cut, complete with all the behind-the-scenes drama and the blooper reel of fees. It’s the number that truly tells you, "This is how much you’re really paying for this money."

Think of it this way: the interest rate is the delicious frosting on the cake. Pretty, enticing, makes you want to dive right in. The APR? That’s the whole cake, including the flour, the eggs, the sugar, the baking time, and the oven electricity it took to make. You need to know about all of it to truly appreciate the cost and decide if it’s worth it.

In summary, my friends, the interest rate is the base price, the initial charm. The APR is the final bill, the gritty reality, the full monty. Always check the APR. Your future self, sipping that much-deserved margarita (or at least enjoying a less expensive toaster), will thank you. Now, who wants another coffee? This financial talk is making me thirsty.