What's Difference Between Direct Debit And Standing Order

Right then, let’s talk money! Specifically, those magical little arrangements that make your bills vanish like a ninja in the night, without you lifting a finger (well, almost). We’re diving into the wonderful world of Direct Debit and Standing Order. Now, don’t let those fancy names scare you. Think of them as your personal financial sidekicks, each with their own superpower. Let’s get to know ‘em!

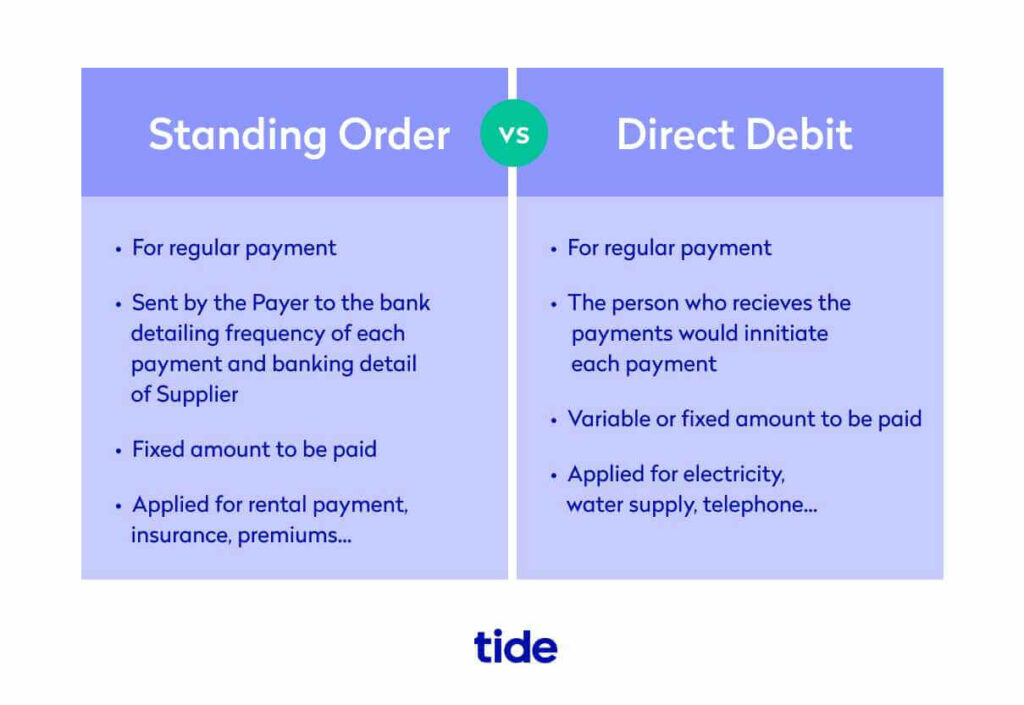

Imagine your Direct Debit as a super-flexible, super-charming personal assistant. This chap is so good at his job, he can adapt to different situations. He's the one you give permission to, to dip into your bank account and grab the right amount of cash at the right time. It’s like saying, “Hey, Netflix, you know how much I love binging that new show? Just take what you need, when you need it, and I’ll trust you to get it right.” Super convenient, right? You’re essentially authorising a company to take payments from your account, and they’re the ones calling the shots on the exact amount and when it's due (within agreed limits, of course!).

This is brilliant for bills that change each month, like your electricity or gas. One month you're practically living in an icebox and the heating’s blasting, the next you're opening windows in January. Your Direct Debit can handle that fluctuation without you having to remember to update anything. It’s like a chameleon, blending in with whatever the bill demands.

Now, let's meet Standing Order. This guy is more like your meticulously organised, ever-reliable butler. He’s all about routine and precision. You tell him, “Right, every single month, on the 15th, take exactly £50 from my account and send it to my Mum for her birthday present fund.” And that’s exactly what he does. Every. Single. Month. No questions asked, no fluctuations. It’s a fixed amount, at a fixed time, to a fixed destination. Predictable as a sunrise, dependable as… well, a butler!

Think about your rent, or maybe a regular transfer to your savings account, or even that cheeky contribution to your mate’s holiday fund. These are perfect jobs for your trusty Standing Order. It’s like setting a reminder on your phone, but instead of a little ping, it’s a smooth, silent transfer of cash. You’re the one setting the rules, and your bank follows them to the letter. You are the boss here, and the Standing Order is your loyal foot soldier.

So, what’s the big difference then? It all boils down to who’s in the driver’s seat. With Direct Debit, you’re giving a company the power to take money, and they can adjust the amount (with notice, thankfully!). It’s great for variable bills where you don’t necessarily know the exact figure beforehand, but you know you need to pay it. It’s your flexible friend.

With Standing Order, you are in charge. You set the exact amount, the exact date, and the exact recipient. It’s your steadfast companion for fixed, regular payments. It’s the one you trust to be precisely on time, every time, with the exact same amount. No surprises, just smooth sailing.

Let’s paint a picture. Imagine you have a gym membership. Sometimes you go every day, sometimes you’re more of a weekend warrior. Your gym might offer Direct Debit. This means they’ll take the agreed monthly fee, and if they have a special offer one month or if their pricing changes slightly, they can adjust the amount (but they have to tell you!). It's convenient because you don't have to think about it, and it adapts. It's like a friendly nudge from your bank, saying, "Psst, gym money due!"

Now, imagine you’re saving up for a fantastic new gaming console. You decide you want to put £50 aside every single payday. You’d set up a Standing Order. On the day you get paid, BAM! £50 magically appears in your savings account. It’s a done deal. No one can change it, no one can stop it (unless you tell them to). It’s your personal piggy bank’s best friend, ensuring your savings grow like a magnificent beanstalk.

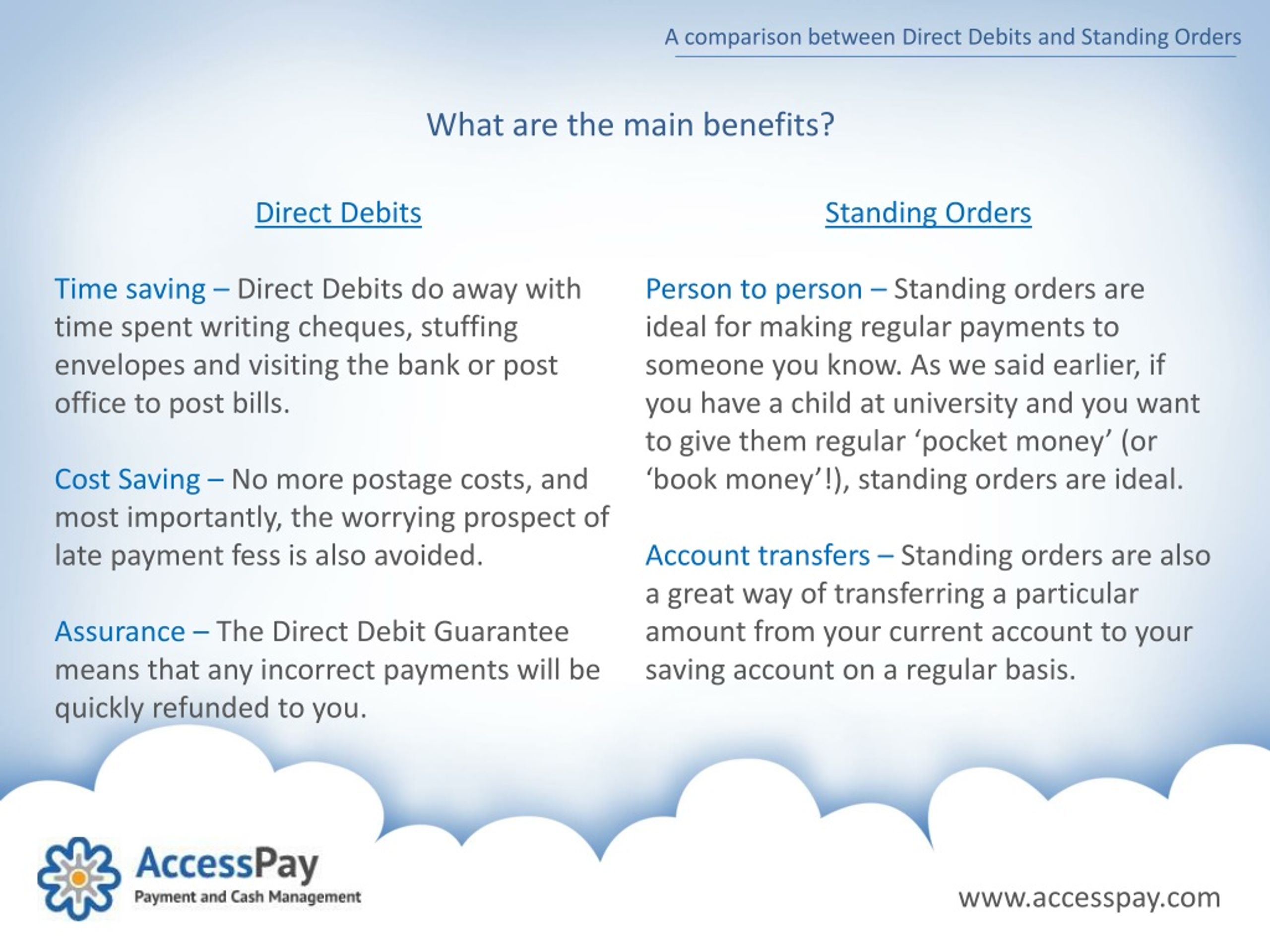

Here’s a little secret: both Direct Debit and Standing Order offer fantastic protection. If something goes wrong with a Direct Debit payment, like if you're billed the wrong amount, you’re usually covered by the Direct Debit Guarantee. It’s like having a financial superhero cape! For Standing Orders, because you’re in control, any errors are usually down to a human slip-up, and your bank will help sort it out. So, no need to fret about either!

Ultimately, the choice between them depends on what you’re paying for. For bills that can change, like utilities, phone contracts, or subscriptions, Direct Debit is often the way to go. It’s the hands-off, fuss-free option that adapts to your spending. For regular, fixed payments, like rent, loan repayments, or those all-important transfers to loved ones or savings, Standing Order is your steadfast and reliable choice.

So there you have it! Two brilliant tools in your financial toolbox. One is your adaptable, accommodating personal assistant (Direct Debit), and the other is your precise, unwavering butler (Standing Order). Whichever you choose, they’re both designed to make your life that little bit easier, and a whole lot more organised. Now go forth and conquer your finances with confidence (and a touch of playful exaggeration, of course)!